Essentially how it will work is if you have 100 shares of Gujarat Borosil you will get 50 shares of Borosil Ltd (current BGW) and 50 shares of Borosil Renewables (currently GBL), so essentially given current price of 122 & 305 there is a good arbitrage opportunity unless I am missing something.

Hi

This is right imo. This is detailed in the latest investor presentation also.

Resultant Structure:

– BGWL will be renamed Borosil Renewables Ltd. and house the Solar Business

– HTL will be renamed Borosil Limited and house the Consumer ware and Scientific ware

businessesConsequently:

•Shareholder with 100 shares in BGWL today (Pre bonus) will own 400 shares in Borosil Limited and 400 shares in Borosil Renewables Ltd.•Shareholder with 100 shares in GBL today will own 50 shares of Borosil Limited and 50 shares of Borosil Renewables Ltd.

Now if we look at the prospective arbitrage opportunity. I think there is one. Had scribbled something to a few friends (attached). It makes sense to buy Gujarat Borosil (we can’t short BGWL).

Regards

Deepak

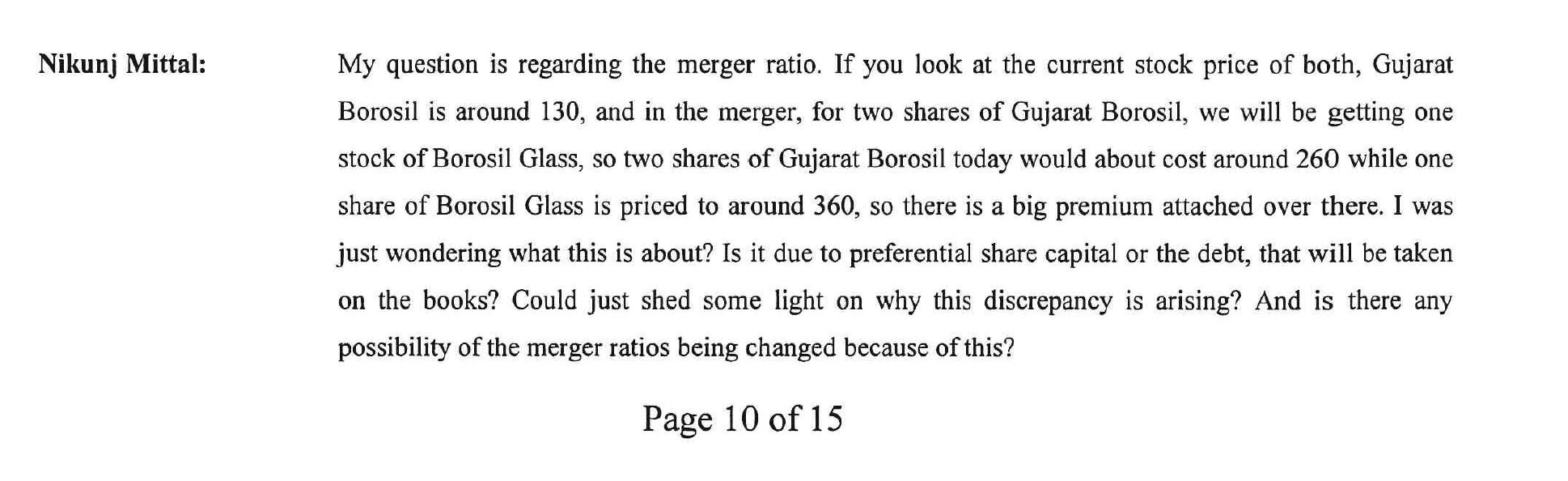

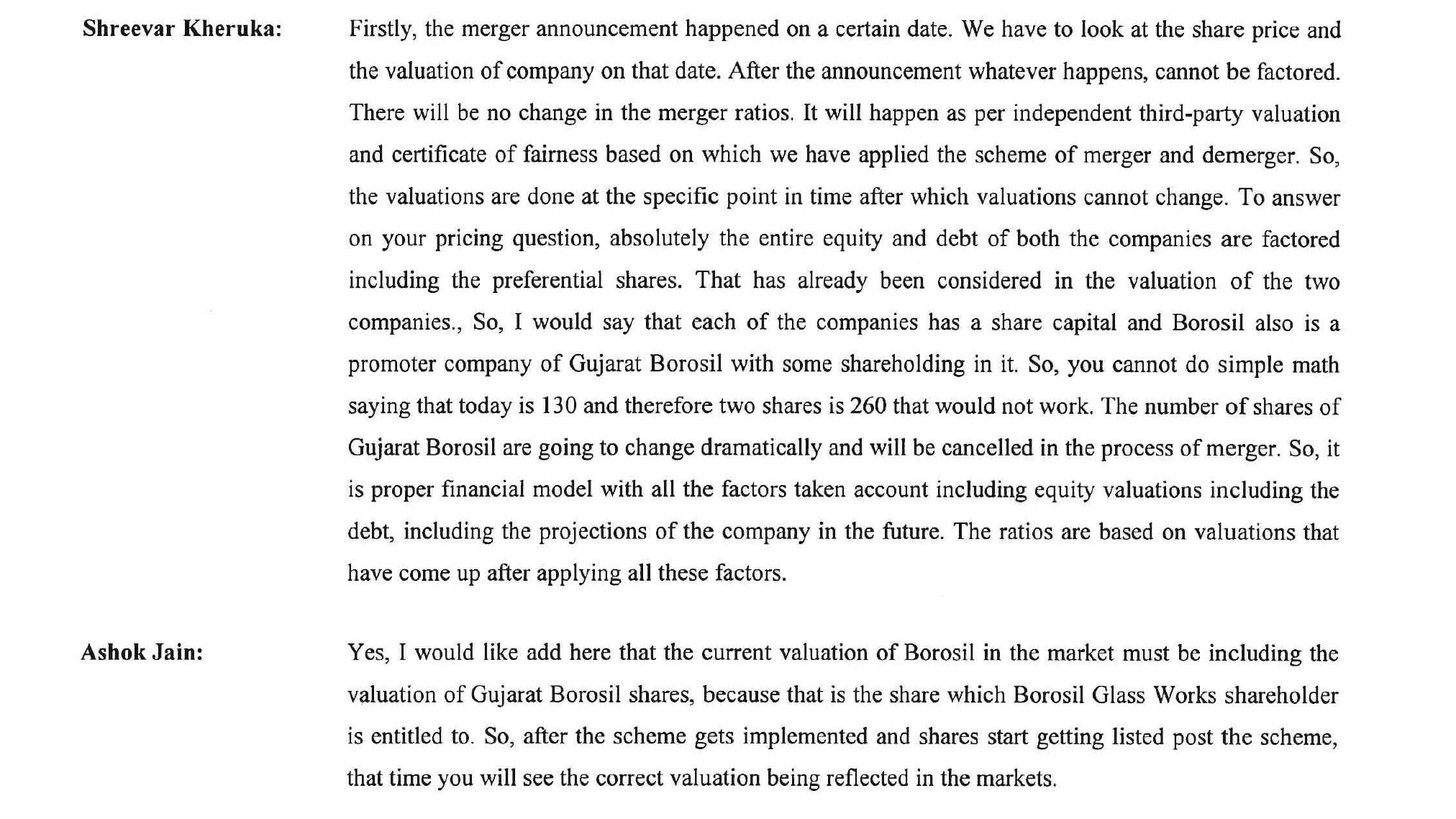

Was doing some digging into the arbitrage opportunity the exact same question has been asked in the Gujarat Borosil concall, here are screenshots of Q&A, 2nd answer is relevant here.

Essentially he is making the point that BGL currently owns 25% of equity and a lot of preference shares. In Gujarat Borosil, BGL ka price includes that value.

This works out as under - 25% OF Gujarat Borosil equity will be Rs. 30 (120*0.25), preference shares will be another 6-7 bucks (Rs 54 cr worth of preference shares/ approx 9 cr shares post bonus equity of BGL - pre bonus equity was 2.3 cr shares), so ~ Rs. 37. Now one cannot say how exactly the market is valuing sub variables but logically the point is sound. So the quantum of arbitrage is reduced significantly, pretty much close to negligible. Mr. Market may have got his numbers right!!

1 Like

Thanks.

On second thoughts I think its a little more complicated and the exact arbitrage if any will be a tad difficult to figure out.

BGWL owns 25.25% in GB with 100% preference shares. BGWL also owns 48.85% in Fennel which in turn owns 33.13% in GB. 16.57% is owned by promoters directly and the remaining quarter by public. There is a little more cross holding because the promoters hold 100% in Vyline which in turn has an investment of 8.2% in Fennel and again Fennel has in GB.

Agree market would have already figured out the optimum levels.

Rgds

1 Like

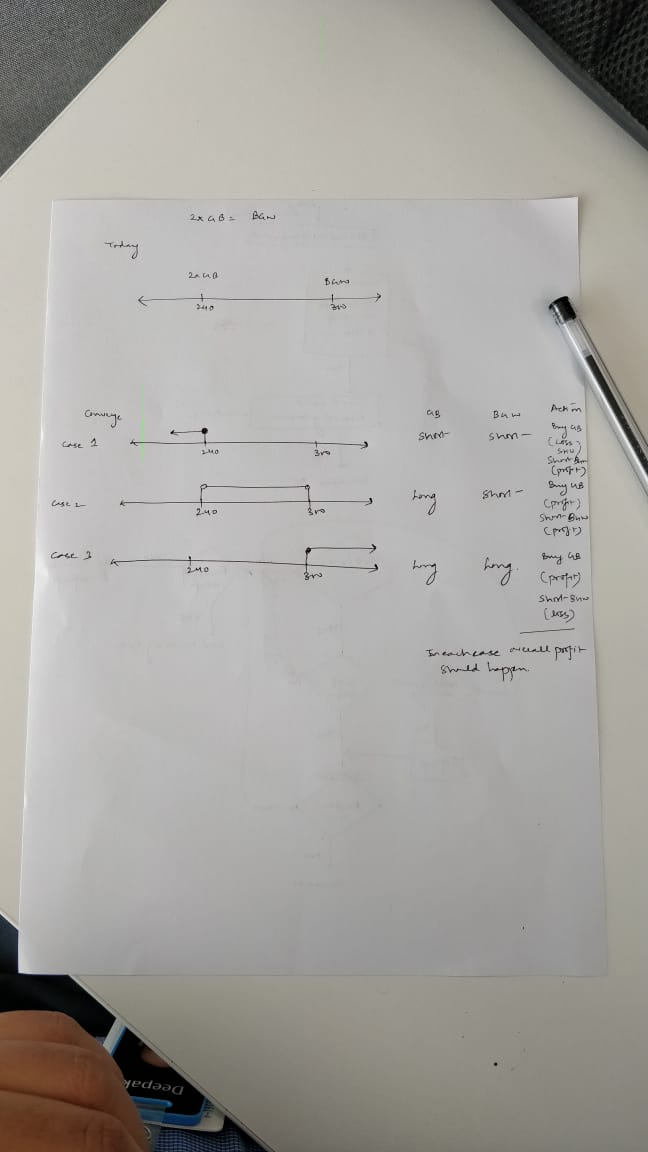

I am unable to understand cross holding puzzle. I have X no of shares in BGWL and Y No of shares in GBL. Post Merger, I am entitled for BGWL shares = x+Y/2. Assuming today’s share price of GBL Rs 121 and BGWL @Rs 303, share price will find post merger somewhere in between 303 and 242. In this case those who are holding GBL will stand to benefit and BGWL holders will stand to lose. Even assuming BGWL share will not correct downward, the quantum of appreciation for GBL will be much more than GBWL Demerger is going to happen only after merger of GBL and BGWL . Hence there is a good arbitrage opportunity available for GBL holders. Is it not prudent to sell BGWL and buy twice the qty of GBL. Am I correct in my assumption?

1 Like

Two shares of Gujarat Borosil would be entitled for one share of Borosil Glass works. After the demerger of Borosil, the holding will be one share in consumer business through Hopewell (will be renamed) and one share in renewable energy though Borosil Glass (will be renamed). To make it simple two GBL equals to one BGWL. There is arbitrage opportunity. But I fail to understand why the gap is not getting narrowed.

According to me the most important point will be the value of the second entity after Demerger…

BGWL has 25% holding in GBL. Hence BGWL is entitled to get 12.5% of BGWL shares (or gets extingushed) in lieu of 25% stake in GBL. Even then it is not making sense. As a shareholder of GBL I will get 1 share of BGWL for 2 shares of GBL. Demerger in to two different entities after merging GBL with BGWL is not going to give any difference between GBL and BGWL shareholders. In any way u think, there is definitely an arbitrage opportunity.

1 Like

In Short it make sense accumulate GB… instead of BG in current senario

please see my points raised above, it is very unlikely there is any arbitrage opportunity in this…

So you think its better to keep long in BG…

I would do so, I mean unless you are interested in the solar opportunity there is no point in being exposed to Gujarat Borosil, as an arbitrage opportunity as such there does not seem to be much scope, perhaps 10-20 bucks at best.

Borosil has a better business, management is doing the right things, there is scope for continuous improvement in financial metrics in medium-long term as well as rerating and institutional investors coming in. I would think it is a 3-5 year story.

1 Like

Any Technical Chart Experts, can someone suggest the best price at which we can accumulate Borosil ?

Any views on Borosil entry in home appliances business?

Hi

Gujarat Borosil Nos are declared and they seem to be quite good.

Borosil Glassworks to be out later in the day.

–

Update: Borosil Glassworks results attached

Rgds

1 Like

90,00,000 - 9% Non-Cumulative Non-Convertible Redeemable Preference Shares of Rs. 100 each were due for redemption on 16th March, 2019. As consented by the holder of the preference shares and as approved by the Members of the Company at its Annual General Meeting held on 8th August, 2018, the tenure of these preference shares have been extended by a period of 3 years from 16th March, 2019 to 15th March, 2022. Undeclared cumulative dividend on this Preference shares shall be payable as and when declared by the Company or otherwise, at the time of redemption. All other terms and conditions of these Preference shares remain unchanged.

This is extra expense which is not charged to reserves as of now, but will be charged later. How many years preference dividends are pending?

Why does the company does not want to redeem preference shares. The actual effective cost of a 9% preference shares is about 15.10% (Since the payments are not deductable from profits before tax. Further DTT needs to be paid).

I try not to invest in the companies where preference shares have been issued as I feel these are inefficient and high cost instruments used by companies to optically enhance the earnings of the company (below the line charge instead of interest).

I have not read the annual report yet. Just looking at the results.

Disc: Not invested.

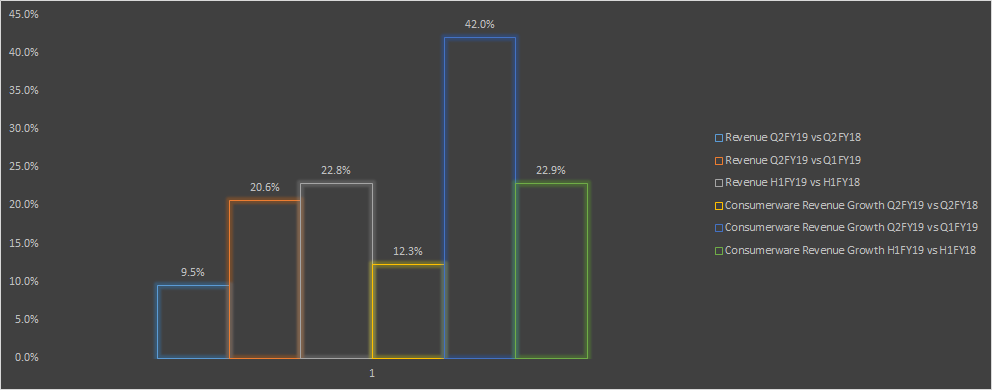

Decent set of numbers by Borosil Glassworks given that

a) last quarter’s base was quite high

b) The festive season is late this year as most of the crockery is bought during Dhanteras and Diwali

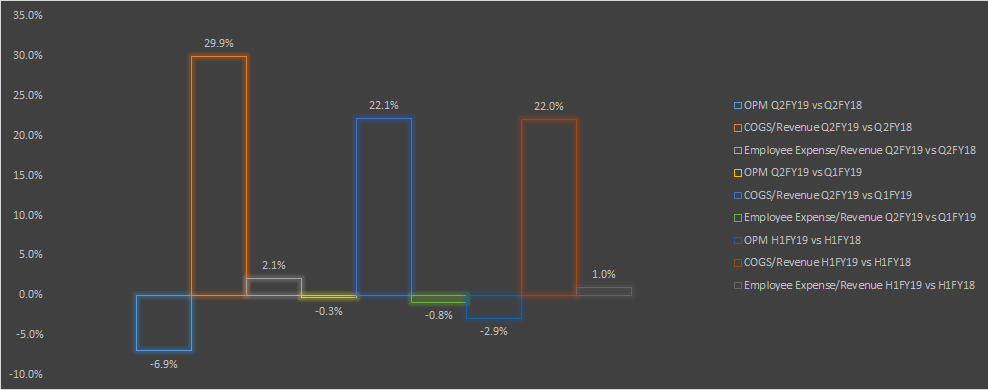

Also, the actual comparison would be H1FY18 vs H1FY19 which shows fantastic growth in consumer ware. They have been spending heavily on brand building and to me it looks like a secular compounding story from here on.

However, the actual picture will only be known when we get to know the hopewell numbers which management has not given.

Disc. Invested

3 Likes

Hi

Was looking at the numbers for Borosil Glassworks. Agree they are decent.

Though the margins have dropped they are incurring more costs as a percentage to revenue, so perhaps they are passing it on.

Personally I am more keen on them increasing their revenues. Will wait for the concall.

Rgds

1 Like

Investor presentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/1fc56f9e-e53a-42ed-96d3-022b6d236954.pdf

1 Like

Short notes from today’s concall :

• 7 cr more advt spend than H1 of last year

• Classpack – new demanding customers, more rejections, hence negative margins, expect to stabilize new customer business in 3-6 months,

• Profitability is not our sole focus, sustainability for channel partners is important

• Higher advertising spend

• 20%+ sales growth expected in H2

• 15-20% EBITDA margins in next few years

• Ordering - 2-3 weeks before Diwali – trade, large format stores – order earlier but expect to deliver around Diwali

• Online sales may become 10% of sales – constant discounting,

• No slower sales this Diwali

• Looking for inorganic growth – investment banking costs have gone up

• Amalgamation expected to be over by Apr – Jun 2019, NCLT may take longer

• No exposure to ILFS, good liquid funds

• Larah capacity – 35/40 tonnes per day, if fully utilized 180 cr per annum, 80% cap utilization,

Expansion – not planning , maybe debottlenecking 10-20% , no plans to add new furnace

Larah – 6-7,000 touch points, 130 exclusive Larah distributors

• Huge difference in margins with competition – major reason – now 20% ebitda in opalware,

Lower electricity cost for la opala due to plant location, La Opala gets slight premium on selling price, Borosil per unit 20% higher electricity cost,

• As capacity util go beyond 92%, margins would improve. Can see margins around 20%+ but would never match La Opala

• As La opala adds capacity, 40% margin is not sustainable for them as they may have to drop prices, which may put pressure on our prices

• Exports realization have improved. We import more than we export. So some impact on margins

• Borrowing on half year BS – short term for working capital of Rs 68 Cr, increase stocks for Diwali. Rather than selling investments, decided to borrow.

• Borosil Technologies – 15-17 engineers hired in Pune. Over next year to 2, positive results

• Exports to US for SIP – started small way

• Larah market share – our sales 100 cr and 250 Cr La Opala (may include crystal), plus Cello, plus imports. If total market is 500 Cr, then our market share is 20%

• Cash and Cash equivalents - 140 Cr (265 Cr minus 125 Cr for GBL)

• Looking for Inorganic acquisition in SIP as well as CPD

• Large fragmented global customer base for SIP. C class item for pharma companies. So they want overnight once they order. We have very good relationship, good supply chain. But same applies to overseas competitors. So difficult to penetrate overseas market easily.

5 Likes