It’s covered in investor presentation. Cash balance includes the cash.

1 Like

Great news from Borosil. Bonus issue of 3 shares for 1 share held!! Also huge restructuring exercise to simplify the corporate structure

Although the restructuring looks complex on the face of it, it has potential to unlock value for all stake holders.

The earlier structure was a pretty clean one with no major issues. Why has the management changed the entire plan so suddenly and so drastically? Gujarat Borosil was to be a 58% subsidiary of BGL while now that business is a separate entity altogether. While per se I don’t think that is a bad thing and it was being run by a different branch of the family anyway, why has the plan changed? Was there some issue in NCLT approval? Vyline Glass also seemingly assets are being divided, not clear how.

Personally I see it as a concern not a positive. My feel is this has more to do with inter-family issues than any other factor. Need more clarity mainly on how valuation is going to be done before taking a call either way.

The reasons for the change in scheme looks pretty simple

a) They wanted to fund the equity requirement for the solar business.

b) They wanted to increase their shareholding in the solar business without paying any money.

In my opinion, this is neutral to bad for the existing shareholders. Neutral, primarily because it will result in realisation of GBL Stake by the shareholders of the company and Bad, because all the cash will be drained away and many people don’t like GBL businsess (including me).

Disc. It was my second largest holding and I reduced it considerably after this scheme. May add in future if I am able to made up mind about GBL business.

stock up 17% though, someone seems to like the scheme…

I think this 17% rise now discounts the stake in GBL. I am pretty sure management will say that they did this to realise the value in GBL. Let’s wait for the outcome of conference call which is scheduled today.

Concall notes

- Two step amalgamation process Step 1- Vyline, Fennel and Gujarat Borosil would merge into Borosil Glass. Step 2 - Scientific and Consumer product division (alongwith investment in Classpack) would demerge into Hopewell Tableware

- Old Borosil Glass would be renamed as Borosil Renewables and Hopewell Tableware (with demerged consumer/scientific divisions) would renamed Borosil Ltd.(Both would be listed on BSE and NSE)

- Shareholders holding 100 shares of Borosil Glass as of today first would get 300 bonus shares of the company (Borosil Glass) and after completion of amalgamation process/NCLT approval (12-15 months) would 400 shares of Borosil Renewables as well as 400 shares of Borosil Ltd.

- 125 Cr from current BGWL cash would be used towards capex of Borosil Renewables and 140 cr would remain with Borosil Ltd.

- Post amalgamation, both the companies would have identical share /ownership structure ie. 11.4 Cr shares of Rs 1 each as well as 70.5% promoter shareholding.(lower than today!)

- No cross holding between Borosil Ltd and Borosil Renewables Ltd. Complete elimination of related party transactions. (may be my assumption

)

) - Post amalgmation, investors who do not want to invest in consumer or solar can do so by selling their shares (today when you own shares of Borosil glass, you become reluctant part owner of Gujarat Borosil’s solar glass business)

- Name change shows company’s long term intentions - Borosil did not want to restrict themselvs with glass products only and wants to grow into non glass consumer product area like steel containers as well as appliances, lab equipments etc and current GBL wants to keep their option open for any growth area in renewables for e.g. solar modules (forward integration)

- As per Mr Kheruka, Solar glass would be long term (3-5 years) story but he is extremely bullish on this business.

- All in all, steps in the right direction. Mr. Kheruka came across as honest and down to earth person doing the right things for all stakeholders. Post conference call, my conviction has strengthened.

)

)Disclosure - forms 10% of my portfolio. Would be interested to add more in case of price fall

8 Likes

Extract from FY18 Annual report:

http://www.borosil.com/doc_files/Annual%20Report%202017%20-%202018.pdf

Borosil declared hefty Bonus share:

Bonus share Ratio of (3:1) & August 03, 2018 is the Record Date for the same.

AR 2018 highlights  :

:

• During FY18, the Scientific and Industrial Products (SIP) division including Klasspack achieved Net Revenue of Rs 187.1 crore, a growth of 17.0% over the previous year. In FY17, Borosil held Klasspack for 8 months in the year. Adjusting for Klasspack sales on a like to like basis, the SIP division’s revenue grew by ~11.0%.

• The Company has now introduced a range of products branded Labquest by Borosil range of Bench Top equipment. This launch has found ready acceptance and includes products such as Centrifuges, Shakers and Magnetic Stirrers. The Company estimates the market to be about Rs 160 crores serviced predominantly by expensive imports and growing at about 8% to 10% per annum.

• Export revenues for the SIP division have grown from Rs 1.4 crores in FY13 to Rs 9.3 crores in FY18. To tap into the larger North American market, the company entered into a collaboration with Foxx Life Sciences in April 2018 to market premium laboratory glassware.

• Klasspack achieved a revenue of Rs 37.4 crore (net of inter company sale) during FY18.

• Klasspack has adequate manufacturing capacity to handle growth in the near to medium term. It currently operates on a single shift. The manufacturing facility is however likely to require investments of about Rs 10-15 crore each year over the next few years for continuous upgrading of the plant.

• The Company has introduced the “To-Go” Hydra range of food-grade stainless steel products. These include vacuum insulated stainless steel flasks and Hot-n-Fresh lunch boxes. These trendy flasks made of food-grade stainless steel keep food and beverages hot or cold all day.

• In FY18, the company invested about Rs 64 crore in capital expenditure towards adding capacity as well as upgrading the production lines to produce ‘best-in-class’ opalware in a range of shapes and sizes.

• The production shutdown that accompanied the enhancement of furnace capacity and upgrading the production lines, resulted in some supply gaps in the market, particularly during Q4FY18. This led to some loss of sales. During FY18, Larah achieved a turnover of Rs 102.1 crore, a growth of 3.9% over its sales of Rs 98.3 crore (including excise duty) in FY17 (Growth in revenue before excise duty was 14.7%). With the expansion completed and production stabilized, sales are poised to increase at a faster rate during FY19.

• The Company has received requisite permissions to build a brownfield new Fulfilment Centre adjacent to the Hopewell plant at Jaipur. The investment required is estimated to be about Rs 50 crores. This consolidation will enable the company to ship goods to customers in full truck loads as opposed to partial truck loads and help in reducing freight costs. In addition, it will improve fill rates to Customers and also improve the response time to market demand. The project is likely to get implemented in the fourth quarter of FY19.

• As of March 31, 2018 the Company had Net Fixed Assets of Rs 254 crores. During FY19, the company expects to invest about Rs 50 crore in its new Fulfillment Centre at Jaipur. The ongoing capital expenditure of the Company is expected to be to the tune of about Rs 15 to Rs 20 crores each year, including upgrading of its Klasspack plant and repair of the furnace at the Larah factory once in two to two and half years.

• During the year FY18, the Company realized Rs 64 crore, upon disposal of residential property at Samudra Mahal in Worli, Mumbai. This has brought down the value of non-core assets on the books of the Company as of March 31, 2018 to Rs 3.9 crores.

Disclosure: Tracking Position, 1% of my Equity Portfolio

6 Likes

Today’s discussion with Shreevar Kheruka

1 Like

Excellent results from Borosil. Sales up 44% by whereas PAT up by 108%…

1 Like

Stock keeps moving up and now at Rs. 371 on ex bonus basis

2 Likes

Latest conference call transcript

Story is unfolding in predictable manner. Promoters seems to be doing all the right things for the company as well as minority shareholders and markets have started taking notice of it

2 Likes

Wanted you know you view on Borosil Glass work for its market segment and valuation.

Brand Borosil is quit strong in Indian market for its microwavable product and its glass work. Now day this company is going through restructuring of its group companies and subsidiaries.

Thing that attracted me was progress this company has done in its consumer space. Sale and profit are kicking up along with OPM for the company .Also Borosil also entered in home appliance and opal ware.

Went through latest conference call, thing look positive for coming year.

Vivek Vikram Singh

Hi

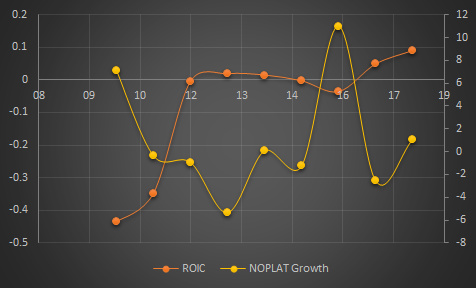

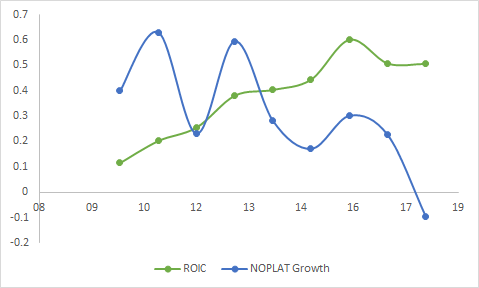

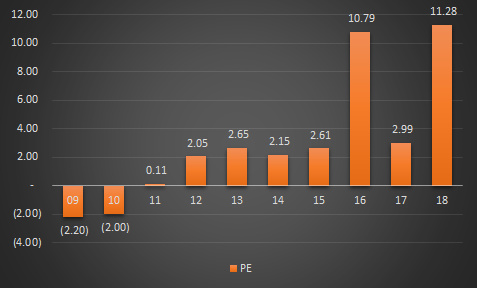

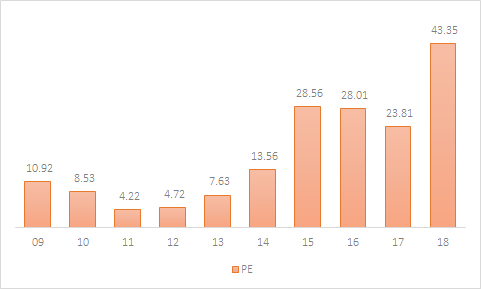

Some pointers in borosil vis a vis laopala

-

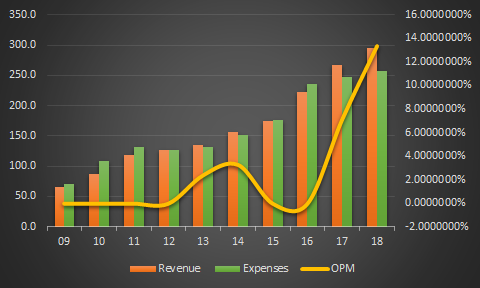

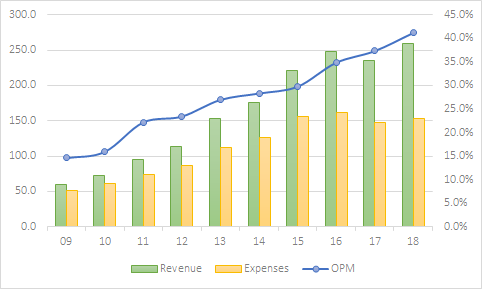

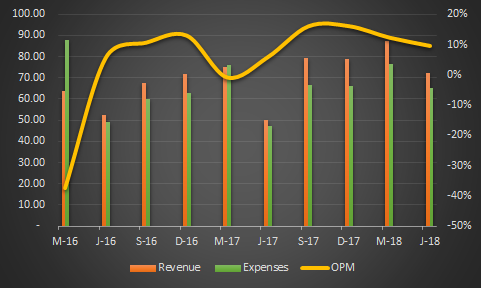

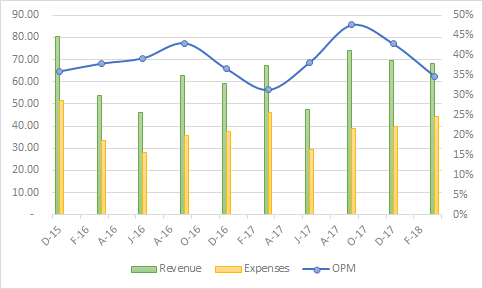

Borosil works at a considerable lower OPM than LaOpala (14% vs 41% in the trailing 4 quarters). Agree that OPM has seen a sharp increase for Borosil on a yearly basis but on a quarterly basis it is dropping (same for LaOpala). Also it is quite low compared to that of LaOpala almost 3x lower. The revenue CAGR for both is ~40% from 2009 to 2018

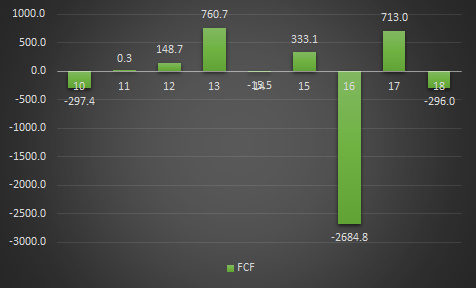

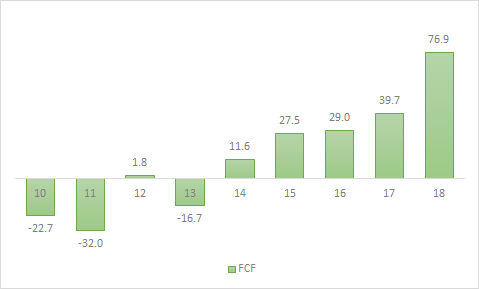

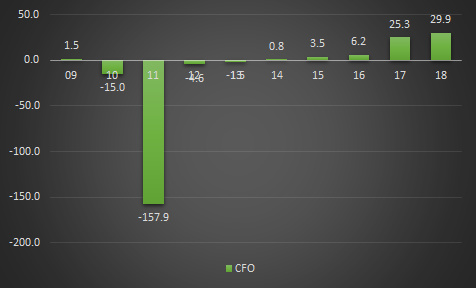

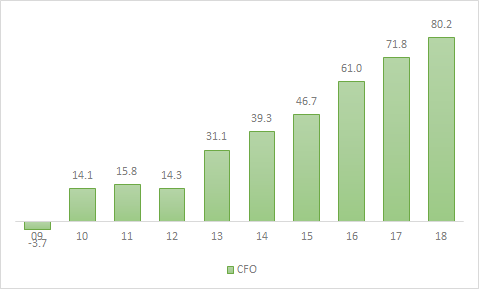

Charts in black are of Borosil and ones in white are that of LaOpala

-

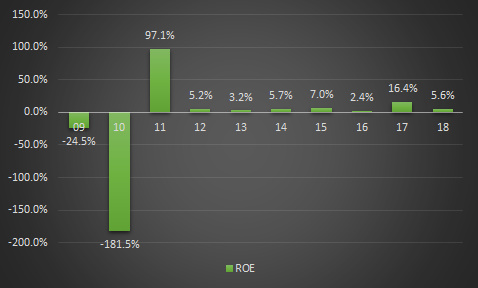

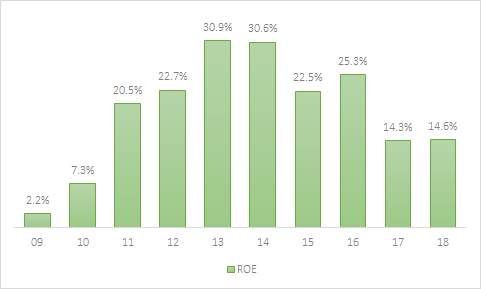

ROIC for Borosil has been very poor

-

ROE for LaOpala has been considerably better

-

FCF is very poor for Borosil

-

CFO too is poor for Borosil

-

Thus Borosil quotes at a lower PE which is understandable and imho should not be construed as being only because of under valuation.

I have also been trying to observe at retail stores. Usually earlier Borosil used to take independent shelves in a store like Hypercity but I have started observing that they are pitching their products besides LaOpala especially in tableware. I tried to inquire this over the weekend but could not get conclusive replies. Some pics from Metro (wholesale) in Bangalore.

Also LaOpala is a preferred product from a little informal survey I have done for tableware. For microwave utensils Borosil is becoming a household name. In my current company and previous ones I have observed a significant number of people switching to Borosil for food safety reasons (earlier tupperware held this position). In addition seeing this market others have started trying to capture this market for instance Tarrington House (Metro in house brand) etc. So definitely the market is expanding but the players too.

Just some of my notes on these two.

Rgds

Deepak

Disclosure: Was invested in Borosil till H1 2017. Hold no more.

14 Likes

Just to add some perspective on your points, Borosil did not till recently have a presence in the opal tableware segment, it was there in glass microwavable’s and scientific instruments, which are less profitable segments. It entered opal 2 years ago thru purchase of a brand called Larah, which was a much smaller player than La Opala. So essentially La Opala had the segment to itself other than imports and other stuff like bone china, melamine etc. Even today Borosil ka opal business is a work in progress and there is good scope for multi year growth. Also as market is under-penetrated both players can grow well without price competition. Also like I have said earlier Borosil is one of the many companies who have now realized there is more money to be made in showing profits and getting a good valuation than in avoiding taxes!

There is no denying La Opala has better ratios today and both should grow well, La Opala may continue to outperform but IMO possibly Borosil has greater scope for improvement in ratios than La Opala does and management does seem to be moving in the right direction.

2 Likes

Hi

Please do not take what I have written in the last post as something which puts Borosil in bad light from an investment point of view. You are right. Some pointers on Larah from the concall script shared earlier:

- Consumer business has had a growth of 51% QoQ compared to Labware which is 19% (Consumer revenues is 63 crs vs 44 crs for lab)

- Within consumerware Borosil brand products has seen a 42% QoQ growth and Larah has seen 54% (38crs revenue for bororsil and 25crs for Larah). Thus Larah is actually the fastest growing portfolio for them

- Larah ebidta margin has grown from 1% to 13% (this I believe is still lower compared to LaOpala)

- New Jaipur plant has stabilized and efficiency has improved (80% capacity utilization)

- Management believes in the opal segment it is the market which is growing and not fight for market share capture. Opal is becoming a mass market product (steel is main competitor, melamine is a small market and bone china has headwinds because of the anti dumping duty)

- Marketing spends is going to be substantial at 14% of revenues

- Expect 15-20% growth in Opal on a longer time frame

In my market visits I checked out Larah including Moon, LaOpala and Corelle. My personal observation was that Larah is the cheapest of the lot from a pricing perspective. Spoke to a small set of consumers and I think the management is right in channelizing funds for marketing as it is needed. LaOpala is always premiumly priced over Larah perhaps.

Management also believes and I agree that in other segments the brand Borosil will help in recall and customer satisfaction.

I believe the opal business has good road for growth and with efficiencies kicking in from operations/logistics and coupled with marketing will certainly lead to better sales numbers.

Rgds

Deepak

Disc: Evaluating to increase position. Not a reco.

3 Likes

I was not taking it in the wrong light, your points are totally valid and the valuation gap is justifying that. I was just trying to put it in perspective that the delta scope for improvement is there here. Sorry if a different impression was given. La Opala is definitely a more premium brand as of today, Larah will take time to get traction but it should emerge as a strong second player is what I am saying. There is a lot of scope for growth, both should do well.

1 Like

a basic question - if somebody wants to enter the stock, can’t one buy Gujrat Borosil as the merger ratio has already been decided 2:1 … so now 127*2=254 is less than 315 ??

1 Like