As MS report suggests Korea’s Celltrion is a good peer to compare Biocon with.

Thanks @nav_1996. Spent some time on the MS report today morning. On the face of it seems that they have done the sensible thing by focusing mostly on the Biosimilars and deriving the sum total approach basis ‘EACH’ Insuline/mABs instead of lumping all together. Will need some time to digest all of this new info into my study before I resume my analysis work further.

Team - the more I go into it I realize that Biocon is way too complex then what I may have thought of. Please share any other information etc. that you may have (preferred write-up would be one which break down each of those moving parts and evaluate each of those independently ).

Thanks,

Tarun

Hi @T11 Nice post, but I have to disagree when you say Biocon Adalimumab is at almost same stage as Amgen.

Amgen molecule ABP 501 is already approved by FDA advisory panel and Amgen and Abbvie are already locked in court room battle. Read here.

Do you think biocon will be able to launch Adalimumab in US in Jan-17, if court does allow biosimilar launch?

Continuing from where i left this last week…

Funnel #3: Competition Landscape:

For Now, I am limiting myself to LOB#4 BioSimilar/Biological. As indicated earlier, all the notion of ‘LONG RAMP’ is coming mostly from this segment only. Most moonshot work is happening in biosimilars where they have products competing for a market share worth ~US$60 bil.

Futher, withing Biosimilars, lets narrow down the focus on 4 specific products where Biocon is at a certain advance stage (read phase 3 and/or beyond) in the journey.

Glargine/BASALOG/Lantus (Long Acting Basal Insulin):

Innovator is Sanofi. Patent expired in 2014 and pediatic exclusivity on 2015. In EU and JP this patent expired on 2009. Lilly has approval since Dec’15 whereas BIocon is planning for filling in FY’17. However, For US market Sanofi (innovator) and Lilly reached an agreement according to which Lilly would not launch Lantus biosimilar in US till Dec 2016. The settlement is restricted to (inj pen version (62% of toal Lanuts sales) and doesn’t cover the drug packaged in vialsf. In EU market, beeginning in 2015, Lilly introduced this by the name of Abasaglar in some of the key markets such as Czech Republic, Slovakia, and Estonia, followed by the UK in August 2015, at around a 15-20% price discount to the innovator.

Biocon launched Basalog – long-lasting basal insulin glargine in India in 2009. In addition Biocon has registered glargine in 20 emerging markets. Recently, BIOS announced the approval of its glargine in Japan.

Risk: Possibility of 30 months stay injection possible in case of any litigation suit since management has indicated to file via 505(b). Sanofi and Lilly playing the shots. Lilly has launched Toujeo (varient of Glargine) at same price point. Morgan Stanley expects FY’20 sales of $90mil out of the current 8.4 bl $ opportunity (factoring in Biocon/Mylan marketing arrangement where Mylan sharing profit with Biocon, price erosion with generic, competition, substitutes etc.)

Adalimumab/Humira: (Chronic Plaque Psoriasis):

Innovator is AbbVie. US patent expiry in 2016 and an additional Non composition patent is to expire in CY2022 only. Amgen and Sandoz are ahead of Biocon who is expected to file in 2017. Key challenge is that Humira has approx 70 formulations and treatment related patents thus making it really really difficult to penetrate for any new entrant. Further to that, AbbVie continues on improving the existing formulations and medicine administative methods. MS expects to have a market share of US$38 mil by 2020 against total current market size of 14 bil. (factoring in Biocon/Mylan marketing arrangement where Mylan sharing profit with Biocon, price erosion with generic, competition, substitutes etc.)

Trastuzumab/CANMab/ Herceptine (metastatic Breast Cancer):

Innovator is Roche. Patent expiry in US in 2019 and EU was on 2014. Currently 5 companies (includes AmGen,Pfizer,Celltron, Biocon/Mylan) are under phase 3 trial and all of them are expected to file in FY’16. Expected to have all 5 in early wave launch once patent expires in FY19. That may lead to big bang price drop and margin errosion.

Risk: Innovator is focusing on combination therapies and improved formulations. FDA flagging (interchangeability).

M.S is assigning FY’20 sales of US$75 mil from the current market potential of US$ 6.8 bil. (factoring in Biocon/Mylan marketing arrangement where Mylan sharing profit with Biocon, price erosion with generic, competition, substitutes etc.)

Pegfilgrastim/Neulasta (Chemo-induced Neutropenia):

Innovator is Amgen. US patent expired in 2015 and EU will on Aug’17.In term of phase 3 timing, Biocon is behind Sanoz and apotex, ahead of Pfize and most like at par with coherus. lead runner Apotex is locked in legal issue with Amgen. As always, Agmen defending the turf by improvising the doses, administrative method etc.

MS according a market share of US$41 mil against current market size of US 4.7 bl. (factoring in Biocon/Mylan marketing arrangement where Mylan sharing profit with Biocon, price erosion with generic, competition, substitutes etc.)

Some of the aggregate risk are:

- Evolving landscape, regulatory framework still WIP.

- As always, Innovators acting real tough, more so because EACH of the drug is adding billion dollars to top line. Protecting the pitch by legal/patent battle as well as challenging within market via new improvisation/tweaking etc.

- Concentration risk: Biocon has put all eggs in one basket by a blanket development and marketing agreement with Mylan. Read some where that Mylan may be a big power house in its own accord but in those specific segments is lacking marketing prowess.

- Market acceptance/interchangeability etc.

Reward side view:

After withstanding all this uncertainty, the ‘take away’ for Biocon from the entire pie looks to be comparatively low. As per MorganStanley report, they are expecting FY20 top line addition of ~250 million (out of ~ US$ 32 billion opportunity) from the above discussed 4 drugs.

In conclusion, have developed deep respect for the entrepreneur and the organization for venturing into untested waters {despite coming from a developing (for past 60 years) nation}, holding on to the conviction (despite rather long gestation period), proving themselves in a domain technical niche area, forging long and stable relations with some of the leading industry peers ( I can go on and on…).

However, as far as investment perspective goes, after the sharp upmove in the recent rally, the MoS is very narrow. Seems that market is reacting by looking at the entire pie instead of just realizing what is the real ‘take home’ out of the pie for Biocon. (my personal perspective.)

Disclosure:

- Not invested in Biocon/Syngen.

- Still learning.

- source of info is different research reports, company filling/presentation and other info available in public domain. Do own evaluation before forming conclusion.

3 Likes

Thanks @Gaurav_Agarwal for pointing this out. So, ‘technically’, they are NOT at the same stage. Amgen completed US phase 3 and currently has FDA/EMA filling since late’15. Whereas, Biocon phase 3 is still going on for EU. As per management, filling is possible in FY’17.

Talking about launch of Adalimumab in US by 2017, going by the info it seems that innovator AbbVie is trying to block the turf till 2022 via patent litigation. So, my guess is as good as yours.

Thanks again,

Tarun

Hey Friends,

Just came across this:

`WSJ: Report Mylan Biosimilar comparable to Roche

From little reading, what I have understood is that while Biocon has really got some strong going in Biosimilar space, competition also becomes tough from now on. Market for these drugs will not be a Monopoly/ Oligopoly. Sonner or later it will become a form of Monopolistic competition. In that case earning supernormal profits for long period is not feasible. Lot of the future depends on Mylan’s marketing push for these biosimilars. Got a bit worried by recent rally. Honestly I was expecting this a bit late.

Disclosure: Invested 10% of portfolio since April

Thanks @rks00, @T11, @drmithunraj, @sharrmasks and other respected Value PIckrs for excellent contributions

1 Like

Opportunity size is huge, comparability is more or less established, progress of regulatory process is good. Competeton is also on expected line and all are established players unlikely to drop prices to kill each other. Probalistically speaking , Mylan/biocon should corner a reasonable share. Biocon size is a small so a reasonable share will have big impact on their profits. @theinvisiblehand @rks00 @T11

2 Likes

Recent run-up in prices has been a result of market giving 0 valuation this pipeline for long. Biocon stock price did not go anywhere for last 10 years when they continued do right things and deliver. So current price run-up is just a catch up game. I think market is still undervaluing this company considering potential. I think MS is being very conservative assigning <1 % sales in 2020 compared to current sales. Price erosion will not be huge considering few players and volumes may grow globally thus keeping sales in 2020 around same value. Imaging Biocon getting 2-4% of the pie which is not impossible.

2 Likes

Apart from 4 molecules, insulin glargine, pegfilgrastim, adalimumab and traztuzumab which are in various stages of Phase 3/ filing/ pending approval, the next pipeline for Biocon include

- Avastin (Bevacizumab), Roche, 6.9bn$

2 .Humalog (Insulin Lispro), Eli Lilly, 2.8bn$

3 .Novolog (Insulin Aspart), Novartis, 4.7bn$ - Enbrel (Etanercept), Amgen, 8.7bn$

- Neupogen (Filgrastim), Amgen 1bn$

Of these, Phase 3 trial has been initiated for Bevacizumab.

Phase 3 trial comparing Biocon-Mylans biosimilar bevacizumab MYL-10420 vs Avastin (Roche) in lung cancer.https://www.clinicaltrialsregister.eu/ctr-search/trial/2015-005141-32/ES

Start date: July 2016, End date: October 2017.

1 Like

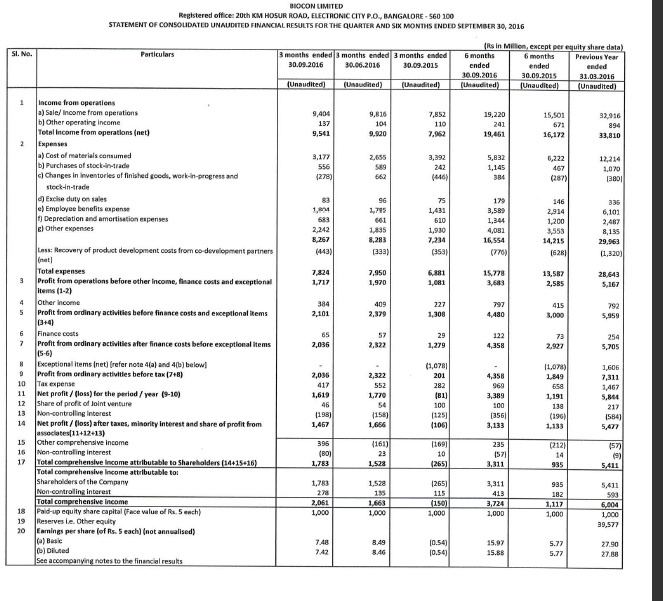

Excellent numbers…

Story is evolving well. Should be a solid wealth creator over next 4-5 years.

Hi All,

I would like to put in some of my views here. I hold Biocon (around 6% of my portfolio) as I believe there is potential here. But I would like to keep looking at the negatives so that my expectations are slightly muted and also gives me the opportunity to exit in case any of these risks suddenly become very real threats to the business. So here goes.

a. The company has invested upwards of 2000 crores in the Malaysia Insulin plant. In the Q1 2017 call, it was indicated that depreciation of this plant will start only after regulatory approvals in developed markets (this being the intended use) whereas the plant will be used for current R&D and sales to emerging markets in FY 17. This essentially means P&L impact on depreciation is going to be deferred to a future uncertain event. I don’t agree with this interpretation of the accounting standards. In my view the company has to start depreciation as soon as the plant is put to use for commercial purposes irrespective of its intended use. This worries me more as Biocon is known to use unconventional accounting practices (I am not saying dubious as there is merit in Biocon’s argument too) to smoothen their P&L. One time money received from a partner earlier for termination of agreement was apportioned over a period of time rather than at one shot.

b. The biosimilars are relatively new to the US, subject to litigation, price erosion and there are huge risks inherent in each case. Hence it is highly unlikely that all the biosimilars will be successfully launched, and even if, on time and at the right price. Also the profit sharing between Mylan and Biocon is not known. My suspicion is this will favor Mylan more than Biocon as Mylan has both the FDA connect and the right marketing skills in developed markets. Therefore it is very difficult to value the EU and US biosimilars business of Biocon. The recent price increase therefore seems to be purely based on speculation and not really on any solid valuation principles. Perhaps we are paying too much for the risk involved in biosimilars.

c. The EU approvals for 2 biosimilars were filed in Jul and Aug. It is Oct now and still there is no US approval. My experience with a Pharma company earlier (I was involved in working with the R&D team on biosimilars which did not succeed) tells me that such delays usually happen when there is an issue in the product. Biocon states that this is because of “time taken to comply with regulatory requirements”. I am concerned though as this could potentially mean that the filing in US itself is a risk.

d. Both Biocon and Syngene are looking at more capex that could weaken the balance sheet. While syngene capex appears reasonably protected, the Biocon capex is subject to too many risks. This means that the FCF of Biocon will continue to be negative for atleast 2-3 more years. Really IMO 2020 will be the defining moment for this company. That will decide whether the curennt strategy is a success or not.

e. The company indicated 14-16% of non-Syngene revenues as P&L and 18-20% as gross spends. As of H1 2017 end, YTD R&D spends are around 205 crores of which around 100 crores has been capitalised.

1400 crores is the ex-syngene revenue for the year. 7.3% is the net spend and 14.6% is the gross spend. I know the full year is not over, but it worries me that the company has taken to balance sheet more than what it indicated. Again refer to discussion on point a. Intangible assets by way of R&D stands at 325 crores as of 30 Sep 2016. This worries me as this is going to increase over the next 2-3 years and could hit the P&L at a later point in time. I would have liked the company to charge it off to P&L.

Regards

Shivram.

8 Likes

Shivram, Good post. The only feedback I have is that, you are looking at this more like an accountant / analyst than a business person. Let me ask you a hypothetical question, what do you think the CEO or COO’s daily dashboard looks like? What are the key operational / performance parameters you think they track on a daily basis to gauge what the direction of the business is and what needs to be done going forward? Would it be depreciation/accounting policies / financial statements or something else?

Anyways, let’s look at the concerns you mentioned -

-

Malaysia Facility depreciation - Their accounting policy is in compliance with GAAP and IFRS. In accounting there is a matching principle, of matching expenses with revenues. Therefore you can not begin a depreciation schedule when there are no revenues incurred from the intended use. This is a manufacturing facility built to churn out Insulin products in bulk. Until it begins to do that, per the matching principle, you cannot begin depreciating assets. The facility will show up under CWIP (Capital Work in Progress) & not PP&E/FA on their balance sheet.

-

This is a good point, and something I am looking at closely. I am not as concerned with the price erosion issue, If you look at all the biosimilars launched in the US, the price erosion to date (including the recently launched Infectra launch by Pfizer 4 days ago) is consistently between 15-20%. This is unlike generics that see a 90-95% price erosion post genericization.

http://www.reuters.com/article/us-pfizer-biosimilar-idUSKBN12H2FZ

The facet I am more keenly looking at here is the so called “patent dance” and the delaying tactics that branded drug manufacturers are threatening to employ. Given the fact that the pace of biosimilar launches in the US has picked up over the past few months and the fact that a lot of these companies are getting into agreements allowing the other to launch their biosimilars, I still remain optimistic. Example - Pfizer’s branded drugs are under threat from Sandoz & Amgens biosimilars which are in the pipeline and vice versa. Additionally Mylan takes on all legal risks in case of patent infringement. -

I am slightly disappointed with this as well, I was hoping for at least one biosimilar application in the US in the past quarter. I do not agree with your interpretation of this delay though. Management on the most recent con call reiterated their target of filing commitments both in the US & EU for this fiscal. So far they have walked the talk in terms of living up to guidance, I am hoping they continue on this path. Keep in mind, they are breaking new ground here, so a delay of a few months is not unusual. Developed markets have reasonably similar data and validation requirements for new drug applications, so if they have filed successfully in EU & Japan, it is not out of the ordinary to assume that the extra documentation required for the US has pushed them back a few months.

-

I’m not worried about their Fixed asset expansion or their current FCF. They had a massive capacity crunch mainly for Insulin products last year as they could not make enough to service demand. Additional expansion to developed and developing markets would require additional capacity as well, so not worried about their capex.

As for FCF, I don’t think any one buys either a Biocon or a Granules for that matter or so many other Biopharma companies for their current FCF. I would honestly be disappointed if they had positive FCF s till FY19 and were putting excess cash in a FD or in mutual funds instead of investing in the business for the future. Unless you’re a mature business with limited avenues to invest in and deploy cash (like the sun & the moon) I don’t expect them to have massive FCFs until US &EU product launches.

Invested & Biased.

Please keep the criticism coming, the more holes we can poke into this story and subsequently try and explain / defend, the better our understanding will be & may help bring out things we may have overlooked.

9 Likes

http://finance.yahoo.com/news/edited-transcript-biocon-nse-earnings-170322142.html

Edited Transcript of BIOCON.NSE earnings conference call

1 Like

The acceptance of the insulin glargine application for review by the EMA is another important milestone in Biocon’s collaboration with Mylan,” said Arun Chandavarkar, chief executive officer and joint managing director of Biocon.

Disclosure invested

Thanks

http://www.bseindia.com/corporates/anndet_new.aspx?newsid=a7b6deb6-4bc3-438a-afa9-25333890bd4c

a proposed biosimilar trastuzumab, to the U.S. Food and Drug Administration (FDA) through

the 351(K) pathway. This product is a proposed biosimilar to branded trastuzumab, which is

indicated to treat certain HER2-positive breast and gastric cancers.

Thanks

1 Like

1 Like