Dahej Brownfield Expansion:

The company is expanding capacity from 12,300 MT to 29,200 MT. Dahej plant has 3 operational units (Unit - A, B & C) while 4th unit (Unit - D) is under construction (EC approval already received). Unit D is expected to be completed in two phases - June, 2019 and December, 2019. Unit D will be largely manufacturing intermediates for company’s existing technicals. So the new EC application is for further expansion (may be Unit E and F). If one goes through the details of products, it seems that company is adding new products and expanding capacity for existing products. The total cost of the project is estimated at 200 crore. Normally, it takes 6 - 9 months to get EC approval. Since, its a brownfield capex, the time taken for completion of the projects should be less than company’s greenfield Saykha project.

Saykha Greenfield Expansion

This is the new capex that the company is undertaking at its third location after Rohtak and Dahej. The existing land is near company’s existing Dahej location. Saykha is being developed in line with Dahej since the land in the petroleum, chemicals and petrochemical investment region (PCPIR) in Dahej has been largely sold out. Saykha’s will help reducing the single plant risk for Rasayan (since Rohtak is relatively a smaller plant compared to Dahej). If one goes through the details of the report, it seems company will further add new products, expand capacity of existing products and add facility for intermediate manufacturing. The total cost of the capex is 310 crore.

Normally, I have seen that for EC approval, the company takes approval for large number of products and larger capacity as it becomes cumbersome to go to EC again and again for adding new products. They expand in phases over the years. Even for Dahej, the company had approval for 12,300 MT and they expanded gradually over the years. However, two simultaneous applications for EC approvals with capex size of around Rs.510 crore from a conservative management like Rasayan (as per my observations after meeting them for years during AGM) is pretty interesting.

The company recently participated in Chemspec exhibition held in Mumbai. It seems that the overall mood in exhibition is such that there are increasing inquiries for Indian chemical manufacturers post the recent fire incidents in China in March and April, 2019.

(Disclosure: Invested)

On the face of it, this looks like a bargain buy. But reading from the above thread and annual reports I understand it is better to avoid for the following reasons:

Promoters are not shareholder friendly (Missing send SHP, no investor presentations etc)

Low dividend payments,

3.high salary to promoters and increasing by 50% every year

Loans given to promoters

Related parties working in same industry and hence conflict of interest

High related party dealings

Revenue doubled over 4 years despite headcount reducing from 550 to 450! I don’t know how they achieved that.

Presence of shareholders warned by SEBI.

Boarders invested and following the stock please provide your opinion.

Lemme try to answer some of the queries raised by you: 1. Promoters are not shareholder friendly (Missing send SHP, no investor presentations etc) - Promoters meet the investors during AGM and explain about their business in detail there. They believe that their performance will speak much more than talking to public in general.

2. Low Dividend Payments - The company is in growth phase and expanding capacities every year. So they believe in conserving cash for expansion.

3. Loans given to promoters - Please understand one thing - Company has not given any loans to promoters but taken loans from them. As on March 31, 2018, promoters and their group companies had given loan of around Rs.69 crore to the company.

4. Related parties working in same industry and hence conflict of interest - Bharat Rasayan is a technical manufacturing company (B2B) of the group and the IPO of the company was done to undertake greenfield capex of Rohtak plan in 1990s. The other group company - BR Agrotech and Bharat Insecticide are engage in manufacturing and marketing of formulations (B2C). These companies do not manufacture technical on their own.

5. High related party dealings - As per management and balance sheet also indicates (through receivables from group companies), all the transaction between group companies happen on arms length basis. Let’s look at the data of inter-group sales and receivables outstanding from the group companies over the years which is not alarming:

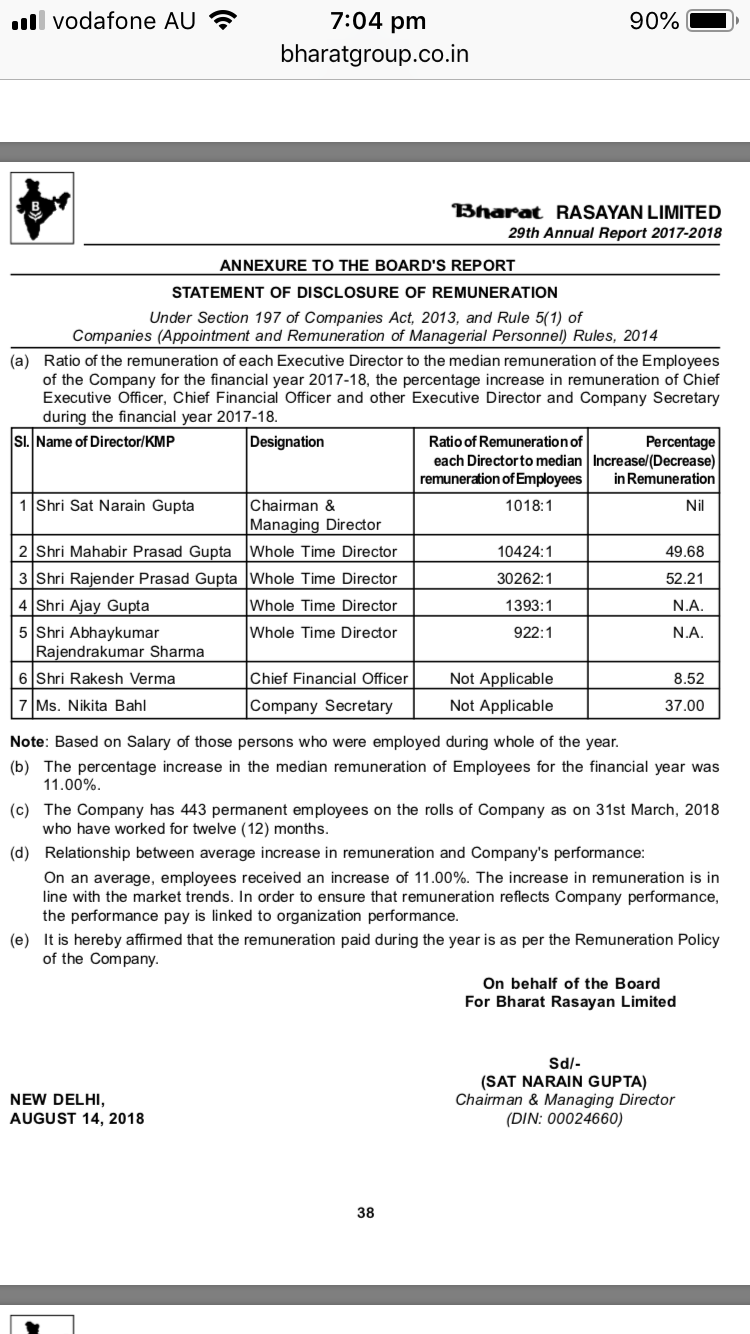

The company is no longer a micro cap. The shareholders buying today would be paying top price at today’s price. There is nothing wrong in expecting a more shareholder friendly management in my humble opinion. Paying themselves filthy high remuneration for their size at the cost of minority shareholders (ie dividends are comparably bread crumbs) which is increasing 50% every year and like 25000 times more than median remuneration is very shareholder unfriendly. So is not proving a regular update through investor presentations.

So this ~ 510 Crores of capex is going to be taken in this FY, any idea? And how is going to be funded?

Also any idea over the last couple of years what has been the volume growth v/s realization growth? Bharat Rasayan has grown at a stupendous rate while the other listed agro chem guys have grown at a tepid rate- any idea what is leading to that?

Overall I am trying to understand what is leading to the growth for BRL, @ankitgupta

Even if we compare the growth of BIL v/s BRL the difference is stark. This is true both for short term and long term duration. I couldn’t get the numbers for BRAL, if anyone has them please share- I think it would be interesting to compare growth within group entities

On the part of remuneration, one must understand that it is liked to commission as % of PBT. As PBT increases, commission will also increase.On a yoy basis, it might look that commission has grown disproportionately but it is just linked to profits. Lot of companies pay remuneration to the directors as commission linked to profits. Nothing wrong in that. Also, remember that in a promoter driven company, promoters have worked very hard to grow the company. Most of us are hop-on and hop-off investors (we can decide to sell our shares anytime) but thats not the case with promoters. They would have done years and years of labour to take the company to where it is today. I have seen Mr. RP Gupta himself attending chemical exhibitions (recently he was there at Chemspec India exhibition at Mumbai which I also attended) and meeting customers. Taking high remuneration is much better way of sharing wealth with promoters as it is more transparent than any other means.

On the part of they being more transparent, I think it all depends on the philosophy of company’s management. Lot of big companies (MRF) and MNCs meet shareholders only once a year during AGM. Doesnt mean that they are not shareholder friendly.

One the capex front, it all depends on when the company gets EC approval and time taken to complete the capex. Dahej capex is expected to be funded largely through internal accruals and might be spread across FY20 end and FY21. For Saykha capex, we will have to get clarity from management as during AGM last year, management had indicated that it is looking at various options for funding it.

In case of growth, we should look at the growth of technical manufacturing companies (B2B) and formulation companies (B2C). Formulation players have been facing tough time due to erratic monsoon, farm stress and increasing prices of technical as many of the companies were not backward integrated into manufacturing of technical. Lets try to look at the growth of Rasayan over the past 8 years which will give us more clarity about where the growth is coming from. I have segmented the growth into three segments - exports sales, sales to group companies (BR Agrotech and Bharat Insecticide) and domestic sales.

Although, post commissioning of the Dahej plant, the company’s sales have grown from all the three segments over the years but last three years sales in the domestic sales has more than doubled. We might think that how is it possible given the weakness in domestic formulation market. However, we need to understand that growth has been higher for Rasayan on account of its products being replacing lot of the products being imported from China. Furthermore, management has been emphasizing on getting into long term contracts with MNCs. MNC sales will include sales to their domestic arm as well as exports. The proportion of such sales has increased consistently for the company over the years. For eg the company started its relationship with one molecule for MNC and over the years it has scaled up the relationship to four - five products. BIL and BR Agrotech cannot be compared to Rasayan as these are formulation companies and their sales have also been impacted by slowdown in the formulation markets.

The growth in revenue has been driven by both volume increase as well as realisation increase. Rasayan currently manufactures 21 active products and its product basket will increase post Dahej and Saykha expansions.

TCS CEO gets Rs16cr after 30% rise this year. And with another 50% rise Bharat rasayan MD will get more than that next year! Just to make a comparison of how bad the compensation is at the cost of minority shareholders and this too after 75% shareholding in the company. Cleanest way for owners to take out money is through dividends. And if they work as well to take a salary. Commission, share options, royalties etc should definitely be frowned upon by the minority shareholders and this weighs down heavily on the corporate governance of the company. The performance, capacity addition etc would mean nothing if we cannot trust the management to work in favour of minority shareholders.

I would like to give a comparison with a shareholder friendly management to make my case. I am not saying this stock is better in any way. This can even become a sham tomorrow. But on corporate governance standards, they score better. Caplin point is the stock. This stock has only one related party with significant dealings. That too a subsidiary with 99.9% shareholding which I believe is because the local law in that country needs a citizen of the country to be a shareholder. The owner takes Re1 salary. This is also a closely held stock with high promoter holding. These promoters also work hard(probably harder) to grow their company.

The top two got Rs10cr and Rs4cr as commission which I think is 10% and 4%. These are not MD, but wholetime directors. If you ask me, a director can get upto 50lakhs for a company of this size. A non-promoter can get a higher salary depending on talent but not at the ratio of 30000:1 of a regular employee. Promoters can take out any amount of money after all it is their company. But they are short charging minority shareholders by taking out through commission rather than dividend.

Are these directors shareholders ?

If not, you think the business or value they added to the company should be valued at 50 lakh. The md thinks it’s valued at 4cr and 10cr

High level glance shows that CAPEX Investment + WC Investment for FY19 comes out to ~124cr (47+77) which is funded by increase in borrowings of ~120cr. However will have to wait for annual CF statement in AR to confirm above numbers and check how internal accruals was utilized, if any.

Inventory has more than doubled from 94cr to 210cr.

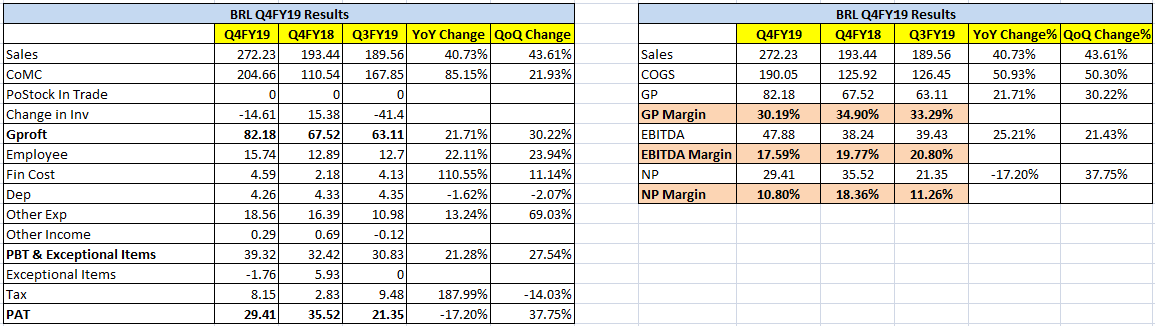

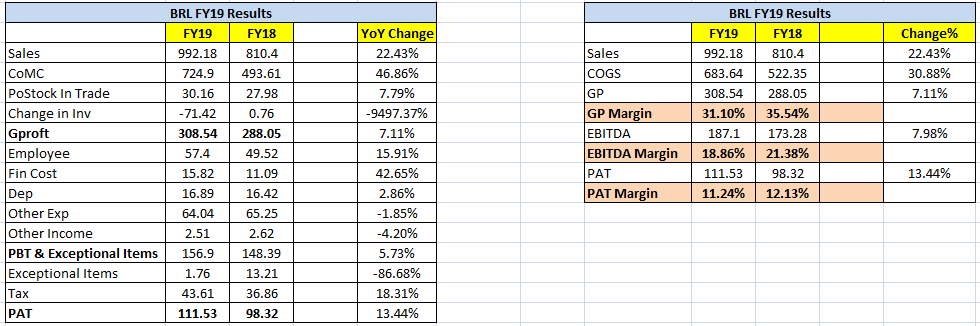

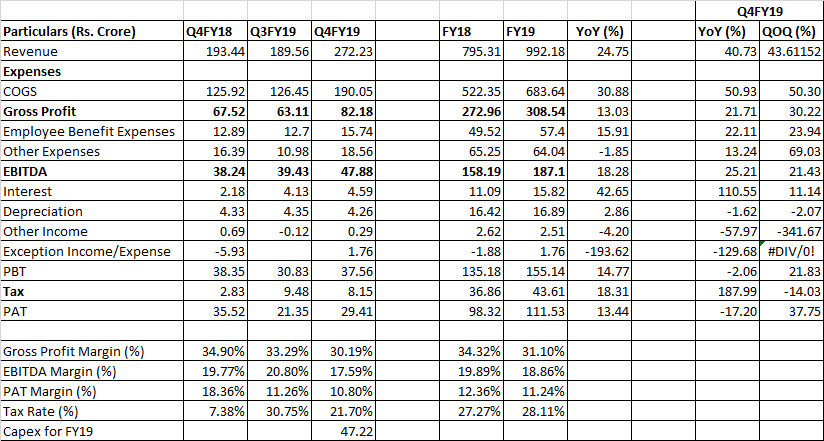

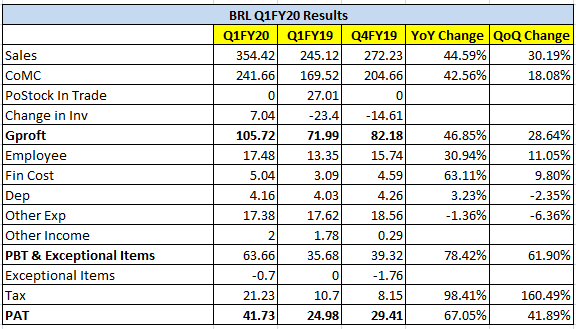

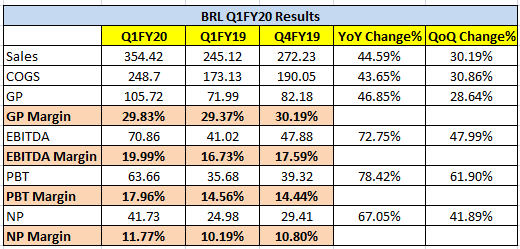

Bharat Rasayan has come out with mixed bag Q4. Revenue growth was healthy but gross margins declined while inventory increased leading to higher borrowings. On one hand revenue growth was healthy at 40%, gross margin declined 472 basis points (bps) which led to EBITDA margins compressing by 218 bps (operating leverage kicked in to reduce some impact of gross margin reduction). Interest cost also increased due to increase in borrowings. On the balance sheet size, receivables have declined from September 30, 2018 levels despite H2 contributing 47% of company’s total sales. Prior to FY18, H2 sales have always been less than 40% of the company’s total sales. It has done capex of 47 crore for the full year. CWIP shown in the balance sheet is most likely for the intermediate plant. The same is expected to be completed in two phases in June and December, 2019 respectively. There has been a sharp jump in the inventory which has increased by more than 100% as on March 31, 2019 compared to March 31, 2018. There can be many reasons for that including shortage of intermediates from China which would have led to company keeping higher inventory. The same along with higher receivables have led to increase in short term borrowings. There are no bank/NCD borrowing on long term basis (40 crore long term borrowing is unsecured loans from promoters). Seems the company funded its capex from internal accruals. Hopefully, gross margins might improve post completion of intermediate plant. Some working on the quarterly nos that I do (Amit has already covered it in previous post) but posting my analysis too:

Indian agrochemical companies are in focus after ADAMA Ltd, a leading crop protection company, said it expects a decline in sales for the first half of the calendar year 2019. The agrochemical major attributed the fall in sales to delays in planting on the back of adverse weather conditions and reduced crop protection applications in many parts of the world.

The Israel-headquartered company said its revenues in constant currency are likely to come in at $2 billion, which is in line with last year’s constant currency growth. However, the company said US dollar revenues may decline due to flooding in North American markets and extremely dry weather in Europe and Asia.

The company expects adjusted EBITDA to be lower by $9-19 million in 1HCY19 compared to 1HCY18. Profits may come in at $123-133 million, as against $157 million last year.

ADAMA said contributions from the Latin American, Indian and Middle Eastern markets are likely to remain strong. The company expects its performance to strengthen in H2CY19 as the southern hemisphere regions, which are performing strongly, move into their peak season, and as output increases from the Jingzhou old site.

Impact on Indian agro chem companies

Most of the Indian agrochemical companies have big exposure to these global markets. UPL earns 18 percent of revenues from North American markets and 14 percent from Europe. The contribution from Europe might go higher due to Arysta acquisition as it has greater exposure in those markets. Latin America accounts for 36 percent of UPL’s total revenues. India and the rest of the world contribute around 17 percent each.

Sharda Cropchem gets around 47 percent of revenues from Europe and 7 percent from Latin America.

The weakness in the global markets will definitely impact companies with high exposure. BASF had already issued profit warning due to trade war and Auto sector slowdown. This also was expected to impact some specialty chemical companies

Its an industry issue and they have indicated that they don’t expect any issues in recoveries. The same has been discussed here also above and I have nothing new to add.