Breakout above the channel

BEPL had been moving in a rising channel for about 8 months. See the black parallel lines. Now it has broken above that channel. This may indicate a rapid upward movement. Or this may be the final push before the decline.

Bad results from Bhansali’s competition Styrolution .Half year eps down from 19 to 11. Reflects Good on Bhansali that they grow so much while competition is unable to do so…

This even raise suspicion on BEPL performance. Means we need to think whats unique in BEPL that its competitor do not have? Why there is a bipolar situation?

1 Like

I think Styro Solutions gave a very optimistic comments in Q2 concall. Expanding capacities, bringing in variants. Also they mentioned , there is a significant demand Supply gap and they want to bridge that

I think they have a good margin expansion this time.

Hi @nil_71

I am looking forward to your deeper analysis of Styro Q2 results. Apparently Q1 was very bad, Q2 is also not very inspiring as Q2 17 profits are lower than Q216 profits.What do you make out of this? Is BEPL outperfoming the pedigreed MNC?

For FY 17 also BEPL was outperforming Styro. This year the gap is definitely widened. Will you share your views?

See my earlier post:

Styro Solution Q2.docx (697.8 KB)

As I mentioned earlier, there is long run away ahead. BEPL management has some bad past but hopefully they have understood that and correcting the same. That is why I am more interested to know how proposed expansion going ahead. Styro- I am not tracking but understanding the demand,Industry dynamics,RM cost variable, margin expansion that may happen for BEPL

PFA the Q2 result concall details. With strong demand and all Auto majors, making India as their Export base, Walking the talk from BEPL, I am honestly more concerned with

Like to reiterate, one thing, we need more proof from BEPL that they are more serious about their business. Need 2-3 Qtrs more. That is why expansion news etc more important.

Thanks … Insightful reply!

I read the Q2 concall docx. Ineos is also expanding capacities and hoping for margin and volume expansion. They are talking of two kinds of capacities: compounding capacity and ABS capacity. I could not understand what is compounding capacity?

If in India imports are only 75000 tons PA. We may soon be having a situation of over-capacity in ABS. This is what seems to be the case as per this document.

Dear Sir

As one of the BEPL shareholders, congratulations on an excellent set of Q2 nos

In the meantime, it will be great , if we get to know how the proposed

expansion from 80KTPA to 137 KTPA going on.

Also, it will be great if you share the presentation, you have given

to all the marquee investors on 27th & 28th October in Mumbai, for the

benefit of thousands of retail investors

Looking forward to hearing from you

Regards

investor

4:09 PM (4 hours ago)

to me

Dear Nilabja Dey,

Thank you for your query.

We would like to bring to your notice that the details pertaining proposed expansion from 80 KTPA to 137 KTPA is briefly mentioned in our Annual report, which have been duly uploaded on BSE, NSE and on our Company Website.

No presentation was made to the investors for their meeting held on 27th & 28th October in Mumbai.

Thanking you for all your support and co-operation.

Regards,

Bhansali Engineering Polymers Limited

==================================================================================

I am very happy that BEPL Investor cell is responding to my Q. Things are changing.

3 Likes

Thanks Nil for sharing this correspondence with BEPL. Obviously the company is tight lipped. But I had a relook at the AR17 that gives me a lot of confidence and I will be retaining my holding for the time being. Few takeaways from AR17 are.

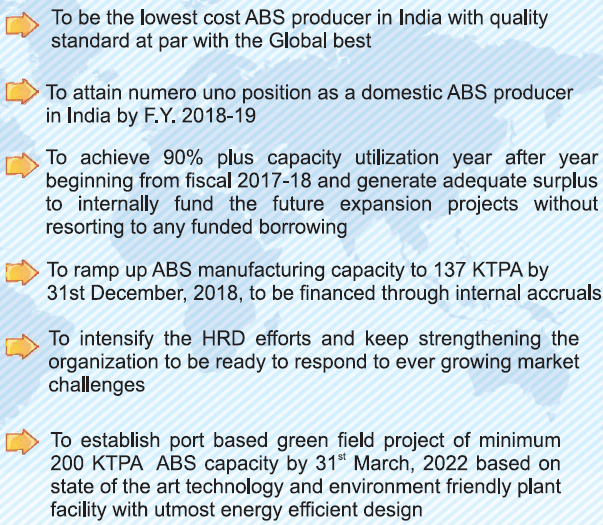

Mission Statement:

Director’s Report: (pp 17-18)

C. OPERATIONS AND FUTURE PLAN:

(I) OPERATIONS

A quick glance at the operational results highlighted hereinabove, when compared with the previous year, will convince the stakeholders that F.Y. 2016-17 reflects a magnificent performance and depicts manifestation of the true potential of your esteemed company. Thanks to the strategic approach adopted by your company to re-orient its marketing strategy by re-positioning its products in highly profitable consuming segments. It is noteworthy that despite stiff competition from imports with relatively weak custom tariff protection, the company could increase its gross margin by 27.80% and the turnover by 18.48%. The increase in sales quantity has also been impressive, showing growth of 15.24% and correspondingly the production by 16.10%.

It may further be appreciated that upon completion of the expansion cum revamping project in the year 2015-16, the total ABS capacity stands at 80 KTPA whereas the exploitation thereof in the year 2016-17 has been to the extent of 64.31% only. Ipso facto, improving upon the results achieved in 2016-17, is likely to be far more impressive in the F.Y. 2017-18 and definitely thereafter in the subsequent years owing to the following facts:

- Buoyancy of growth in GDP in the Indian economy especially post implementation of the GST will push the consumption of lifestyle goods especially in the two wheeler automotive segment, domestic appliances segment and other consumer durables. These first two market segments are the major consumption area of your company’s products.

- The overall demand of ABS has substantially outstripped the present supply from the domestic manufacturers which are only two, your company and an MNC competitor whose respective capacity are identical and aggregates to around 160 KTPA against the current consumption level hovering around 275 KTPA in F.Y. 2016-17, this is likely to continue to grow at the rate of 15% CAGR for at least a decade ahead.

- It is internationally estimated that overall ABS Global capacity utilization is around 70% and which makes the big capacity players to supply in the deficit zone mainly India and China.

- Despite availability of market in India, the global players find it difficult to meet demand of the Indian market as quantity wise it is not attractive to cater to each market segment on account of variety of colours and performance specification. Manufacturing of the variety and the colours largely depend on the compounding extrusion process where it is difficult to strike a balance between the investment and the sectional capacity utilization. Consequent whereupon, there is a huge import of general purpose ABS natural. This is the reason, which attracts several giant global manufacturers of ABS to sell their products in India to improve their respective capacity utilization. In view of the fact that China globally exports the products manufactured out of ABS resins, hence their consuming segments are big enough for any global player to establish and expand their capacity in China itself, however China also imports huge quantity of general purpose ABS from Taiwan. The story of India is somewhat different as we are a domestic market demand driven economy whereas China’s economy is driven by exports. This is principally the reason that has not attracted any third player in the Indian ABS market so far. In the light of the above there is not only the need for existing two ABS manufacturers to improve upon their respective capacity utilization but need to expand their individual production capacity as quickly as possible to reduce import dependence.

- It may be appreciated from the foregoing that your company’s endeavor to attain optimum capacity utilization of 80 KTPA is deemed most expedient and the company is confident that by end of the current fiscal 2018, it will produce and sell 72 KTPA-optimal capacity utilization. Thereafter, in subsequent years, it will ramp up its production and sales by exploiting the additional capacity being created at Abu Road for compounding to achieve an aggregate ABS manufacturing capacity of 137 KTPA by 31st December, 2018. In this connection, all requisites steps have been initiated. The entire expansion programme will be financed through internal accruals. The consistent pattern of growth in ABS domestic demand year on year basis unfolds an exciting opportunity to set up a global size port based ABS manufacturing unit for your company. Presently due to unique market situation company is able to not only sustain but earn handsome profit despite split location of manufacturing facilities as you are well aware of the fact that HRG is being manufactured in Satnoor, MP whereas bulk SAN and compounding production units are located at ABU Road, Rajasthan.

(II) Future Expansion:

Considering the scope and limitation, opportunity and threat and also after in-depth evaluation, your company has decided to set up a port based green-field plant with a minimum capacity of 200 KTPA in the state of Gujarat. The new plant will be based on state of the art technology from Japan and in this connection, the substantive initial steps have already been taken involving several round of meetings with the Japanese company followed by visit of their experts. This Japanese company is none-else than Nippon A&L, Japan with whom the company has a long standing relationship and also established marketing Joint Venture in the year 2013 who are providing sales support as well as technical support with respect to the existing operations of JV products.

Furthermore, infrastructure development work is progressing rapidly in terms of steps being taken by your company for acquisition of land and planning of captive power plant as an integral part of the expansion programme. Based on the encouragement being received from the concerned authorities of the State government and company’s technology partner, the implementation programme has been firmed up to commence manufacturing of ABS from the proposed port based green-field plant by 31st March, 2022.

Perception backed up by conviction of the company is that by the time, the new 200 KTPA port based plant is established; the company will be able to exploit its capacity of the plant optimally. This is because your company is likely to have captured the largest market share of ABS in India. Moreover, based on the competitive cost structure and quality wise at par with the best in the world, if required, your company will be in a position to export specialty grades of the ABS, ASA and AES resins as well.

The aforesaid strategy will ensure birth of a healthy baby, thwarting all threats and limitations which is often faced by any green-field project since it is otherwise difficult to maintain the economic viability in the initial years of production due to relatively lower capacity utilization resulting in not being able to achieve breakeven level of the output which certainly will not be the situation to be faced by your company.

Moreover, implementation of the project takes into account, in terms of the technology selection and logistic planning that it remains globally competitive in the event the Indian economy opens up further and custom tariff barriers is done away with.

In this context, energy conservation and minimizing environmental affects are given due impetus. Furthermore automation and safety measures are no less area of attention for implementing the project based on ultra modern process technology. Due care is being taken to ensure that the material handling system is carried out with least human involvement to improve upon the safety and avoid human errors. The project planning is on the firm footing and it is reiterated that by 31st March 2022, the new port based plant is likely to become fully operational.

This AR says that globally we have overcapacity in ABS production. BEPL is talking about surviving in a competitive environment and telling the cogent reasons. But the worries are currency fluctuations and raw material availability and prices.

Does this make BEPL a moat?

3 Likes

Commodity play cannot be a long term sustaining bet. But you can dance till the music is on. That means as long as Company provides good ROE and that is >15%.

Hi Nil

What will you call a company whose ROE is 30 to 40%?

Styrene Price in China.docx (40.2 KB)

Source http://www.sunsirs.com/uk/prodetail-168.html

Also please have a good tracking of Styrene price. Remember 85% of RM are imported

1 Like

You are absolutely right I have also mentioned in my post that the worries are currency fluctuations and raw material availability and prices. But there is more in BEPL story than what casually meets the eye. For example, What is the ROE of the nearest Indian competitor or global ABS producers? I have a feeling that something more than commodity play is involved. Because BEPL is able to stand out in this environment marked by overcapacity. Also these ROE figures are not sustainable in the long run. So you are right that we should make hay while the sun shines.

1 Like

I had some tracking position in this stock and i picked it up mainly as a trading bet.

Now looking at the potential i’m thinking of moving it into my investment bucket.

From the AR, i’m reading that they are the only domestic ABS manufacturer and the other is an MNC.

is that competitor Styrolution by any chance ?

You’re right. It is Styrolution indeed.

Excellent write up and analysis from your side on the Company. I had initially gone into it as a ST trading bet but then got interested and gone in again as a medium term investment. Couple of doubts/ questions:

- My timing is worrying-gettting into this @peak bull market

- It is a commodity type business with huge dependency on raw material costs/forex

- Not much known about management credibility

But whatever I have read , it seems there is a business opportunity as of now. Please feel free to comment

thnks

2 Likes

I do not make any recommendations. I bought my position at 25. But I am holding. You will have to make your own decisions. My advice will be that keep a strict stop loss if you decide to enter at these levels. The stock may decline from here to 136-138 levels. If it declines below 130 on closing basis I will exit my position. I can only tell about myself.

Your questions have been answered multiple times on this thread by members who are much more experienced than me. Please go through this thread carefully.

Dear @kartiks

It seems that you are new to VP. Posting similar or same message at multiple threads is not advisable. It would be better if you deleted one of your posts.

At the same time you are welcome to Value Picker. it is a great place for taking investment decisions.

2 Likes

Series of LCs and UCs in the last 4 trading sessions. What does one make of it?

Hi Mahesh

This is really intriguing. I am posting a chart below. If there is another rally tomorrow and the stock tries to cross 150 with really heavy volume (1 crore plus), there could be a strong upmove that will take the stock to new highs. We can call this a handle and flag formation. But there is another possibility, and we may be in for a trouble. Presently it seems like a double top formation, as seen in the chart. To make a sense out of it we have to wait for tomorrow or next few days.

Disclosure: I am holding my position and waiting for a big volume tomorrow.

2 Likes