The ABS contracts are priced at 50% spot price and 50% future price. The sudden rise in crude oil prices + drop in ABS and SAN prices last year left the company with lots of high cost inventory. Management has said that results of the company are not 100% correlated with the auto sector since they’re able to pass some costs to clients even in industry down cycles. This was the first quarter after the high cost inventory was all sold off.

3 Likes

I enjoyed your write up of last year’s AGM, did you attend this year as well? If yes, could you publish a similar post on your blog?

Yes sure will do that.

1 Like

In my opinion, it makes sense to invest in BEPL now, for following reasons.

Earning growth drivers:

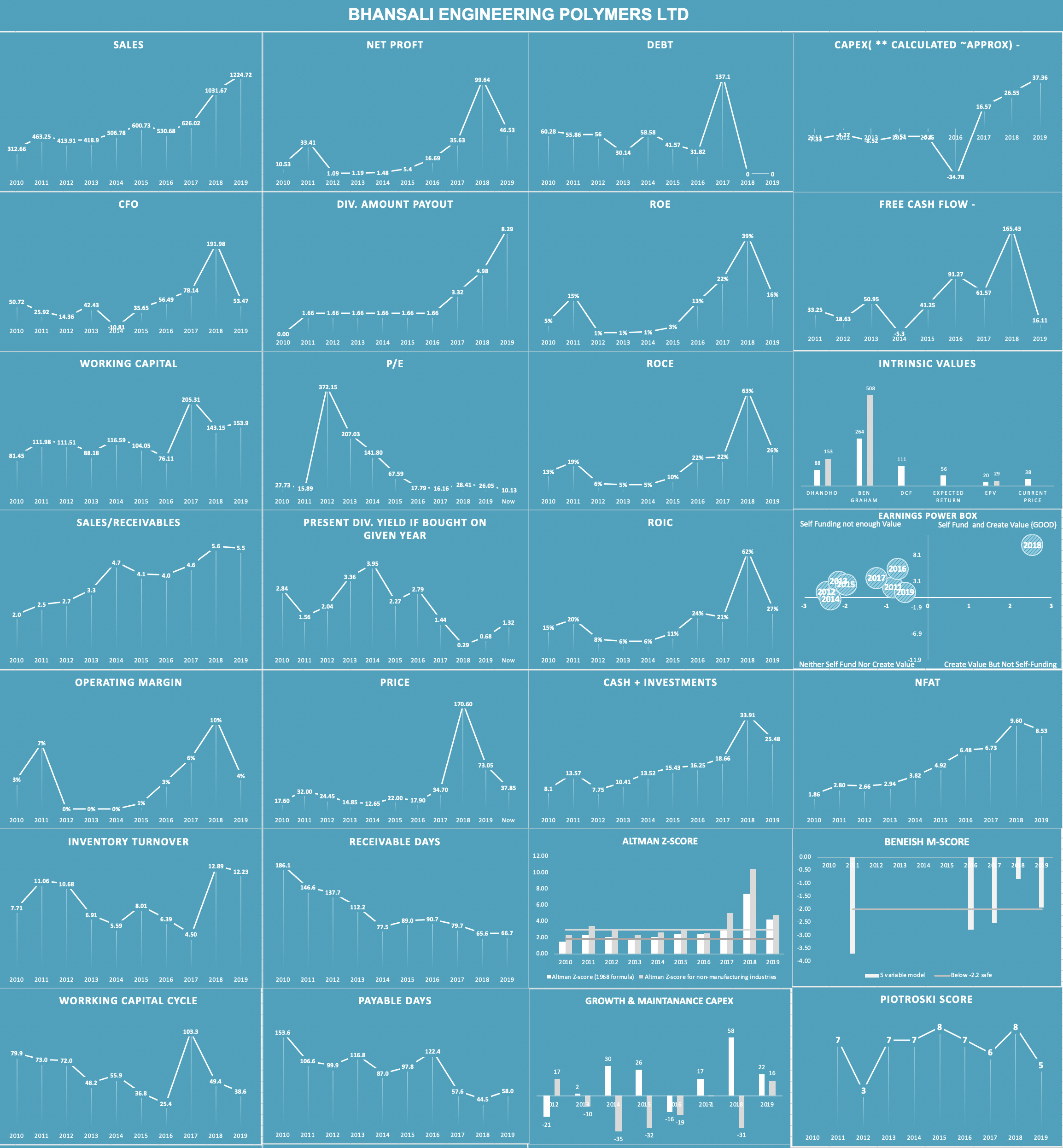

The capacity has been recently enhanced from 100000 to 137000 TPA during last financial year.

The recent lowering of corporate tax will benefit the company.

As per company, the research center at Abu Road is fully functional now. It will help the company in increasing sales of high value products by making custom products for the end users.

Zero debt in the balance sheet.

The share price is near the long term supports.

The key risks to be considered are:

The raw material is mostly imported. The price of raw material is linked to crude.

The company is exposed to foreign exchange fluctuations.

Disclosures:

Invested during this week.

I have been following the company for about four years now. I have completed one cycle of buying in Nov 16 and selling in May 18.

3 Likes

I would like to add that the on going trade war is probably the reason ABS and SAN prices are low, due to cheap ABS and SAN being dumped in India. Even considering this, the company is still undervalued at CMP. It seems like BEPL has gone off most people’s radar so we might need to wait for the broader economy to pick up before market price reaches intrinsic value and it might do better after that. Nonetheless, the company is still strong fundamentally, nothing much has changed on that aspect.

1 Like

BEPL Q3FY20 results.pdf (3.3 MB)

BEPL Q3 results. Again, impressive PAT and PBT considering the macro scenario in the auto sector and currently depressed global ABS prices.

1 Like

Due to lot of moving parts, its very difficult to track this company. Any specific growth drivers you are tracking?

From the raw materials side, ABS and SAN prices and major fluctuation in crude oil and USD/INR rate. The management had previously said that minor fluctuations don’t affect profitability much. From the sales side, performance of the auto and consumer goods industries. These are relatively easy to track. Since the company is only in one segment, as chemical companies go I’d say it’s relatively easy to track the factors that affect the company.

Q3 performance was good considering the decline in auto sales.

As for growth drivers, the BS 6 norms that will come into effect from April 2020 should help in theory but how it will be practically implemented by auto companies is yet to be seen. As discussed in this thread, demand in the ABS market still exceeds supply and BEPL is the market leader. They’ve also increased captive capacity and are in the process of adding new clients, which could be another growth driver.

5 Likes

Very useful info. Thanks Jeet.

1 Like

Hi, can you let me know where you track ABS and SAN prices? Is there a website that provides these prices day-to-day? Thank you!

www.indianpetrochem.com is one website that i know of, unfortunately it is a paid subscription. They track domestic as well as international prices i believe.

1 Like

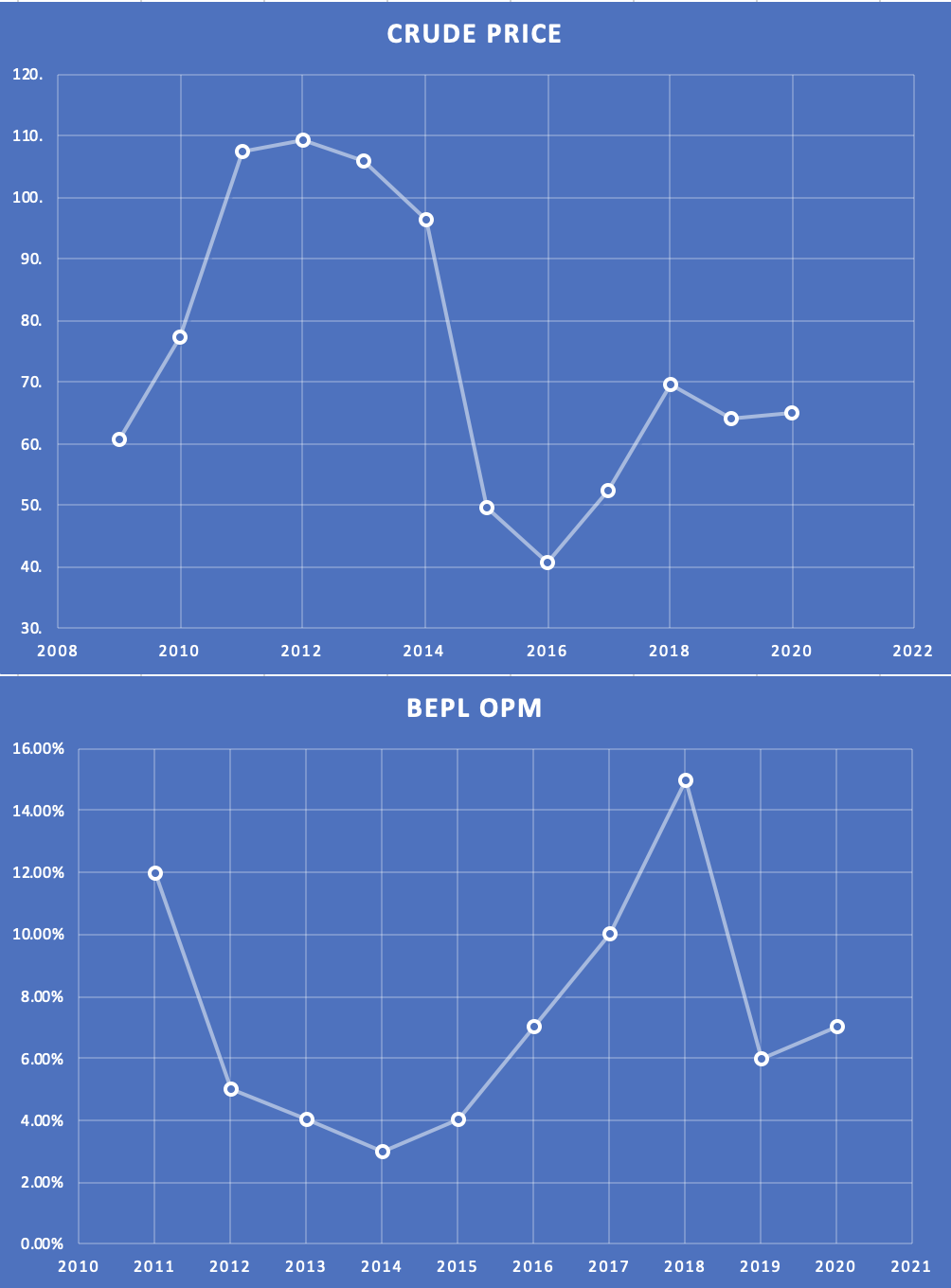

I was looking at BEPL and its margins connected to crude price and also to find out if the value addition to its products can negate any spike in crude.

simple anti correlation between OPM and crude. Now that crude is pretty low I expect BEPL to show good improvement in margins. Recent Capex will give them margin advantage compared to earlier ? Any thoughts on this ? Also did anyone compared the competition from Kingfa science & Tech… They are doing a big Capex and they also produce ABS.

Discl:

I have no holdings… But studying it… may add in the future.

4 Likes

Your observation is correct. May be Promoters can see future earnings due to above same analysis so started buying from open market.

I haven’t done a detailed study of this, but had discussed this with a friend (during the last bull run). The view I’d heard during the bull run pained BEPL as something that was beyond crude-led i.e. it’s not just crude tailwinds, but a structural story. At that time my view was that the company was benefiting from simple crude tailwinds. This view has only been reinforced since. So I very much agree with what you’ve said. BEPL will benefit from low crude prices.

But as far as valuations go, while the last bull run gave it multiples of a “structural story”, this time while results may improve, the multiple is likely to be a “commodity / cyclical” one. That may be useful to bear in mind.

2 Likes

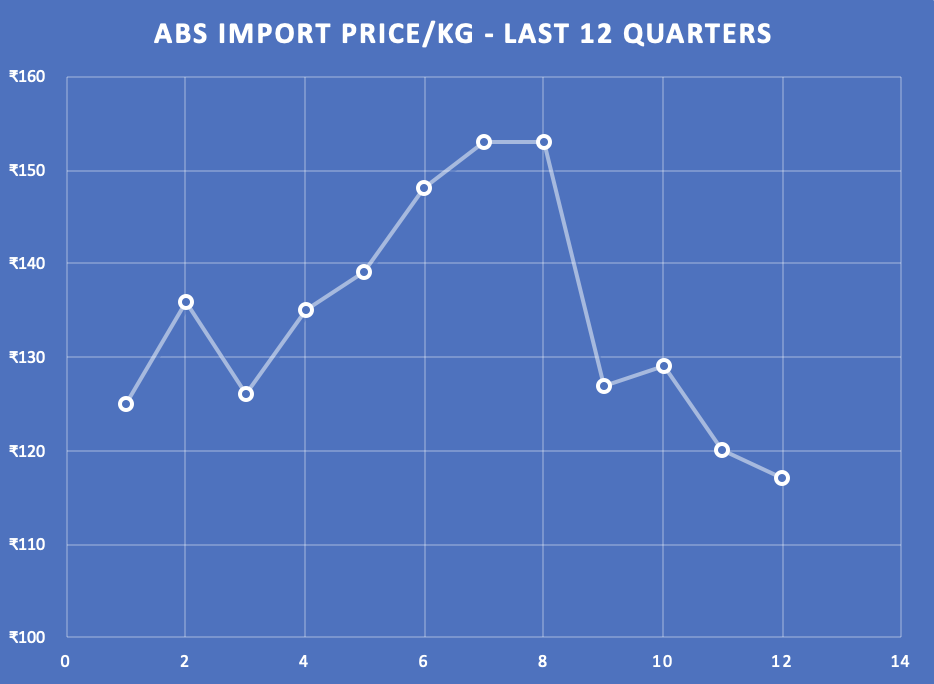

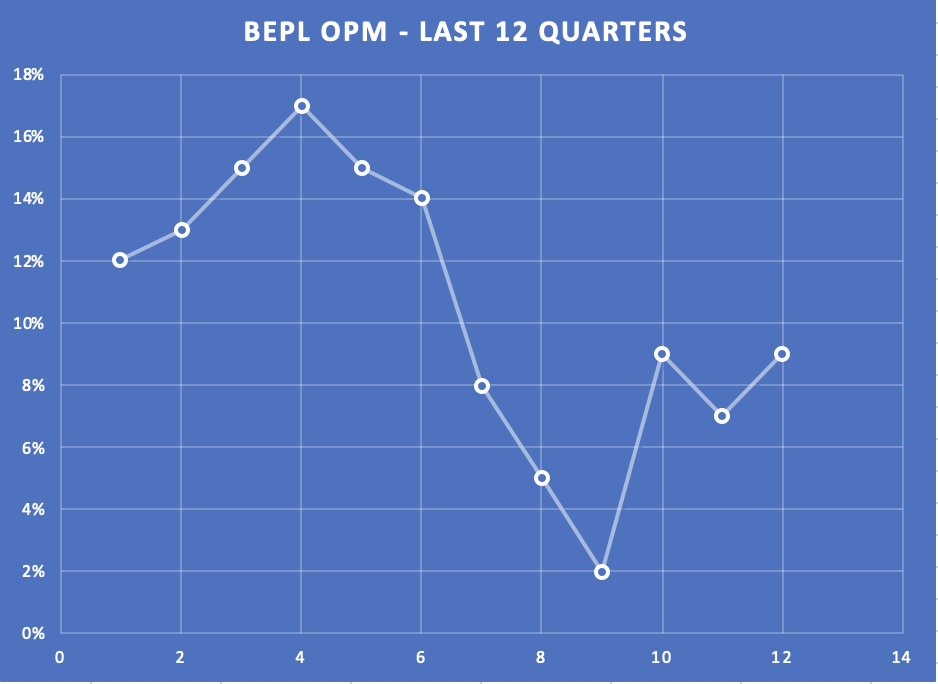

I also did check the recent 12 quarters… Just to see in case if BEPL value addition protects it from the crude fluctuations… Instead of taking crude I took ABS import price as a proxy to HRG.

I see the same trend and I dont see any evidence for any protection… Maybe recent Capex could add few points to margin,

3 Likes

I have analysed Bhansali’s current position. % of Deliverable Quantity to Traded Quantity has been around 55-60% (Source: NSE)

https://www1.nseindia.com/live_market/dynaContent/live_watch/get_quote/GetQuote.jsp?symbol=BEPL#

Company is selling commodity product: ABS whose global prices are increasing. CMP (28) is close to the book value (20). Major capacity expansion is complete

Does it make sense to accumulate the stock at this levels?

Headwinds, I predict: Auto sector slowdown which can last for 3-4 months

Disc: Invested from 140 levels

Capex will give BEPL an advantage in the future for sure. Comparing OPM to crude prices won’t give you much info because in the 2018 AGM Mr. Bhansali himself said that crude doesn’t play much of a factor in company performance, INR fluctuation has a bigger effect.

Regarding your other comment below comparing ABS price to OPM, may I ask where you got the ABS prices from? In all 4 of the quarters in FY18-19 the company had to face systemic problems, beginning with the plant catching fire. Raw materials are imported 3 months in advance to fulfill orders. So when the plant caught fire, the company had to import Raw Materials and Finished Goods. At the time INR value fell from 68/- to 74/-, so the company was stuck with high cost inventory. That’s why you can see a fall in OPM even though ABS prices are rising. Then finally in Q4FY18-19 ABS prices fell too due to auto industry slowdown and the US-China trade war. Despite these issues the company posted a net profit in each of those quarters, while INEOS which is it’s largest competitor in ABS posted a loss. Even Dec 2019 quarter the company posted a very good net profit figure despite the auto industry being in the doldrums while INEOS posted a net loss.

Rather than comparing OPM to crude oil or ABS prices, a better evaluator would be to compare ROCE over the longer term. Even in a bust year for the company FY(2018-2019), it still managed an ROCE of 22% which means that even though external factors were against it in all 4 quarters, management still managed to effectively deploy capital to earn above market returns. In the boom year of FY 2017-2018 ROCE was 58%. 10 year CAGR ROCE is 23% and 10 year CAGR Earnings growth is 30%, which means that over the last 10 years not only has the company been able to grow net profit at a healthy rate, they’ve done it at a rate far above cost of capital. In my opinion this would be a better indicator of a long term compounder.

I have gone through Kingfa’s 2019 annual report and in the MD&A section it only states that the company is looking to expand into engineering thermoplastics without much detail into specific products. Kingfa’s existing capacity according to their annual report is 1,10,000 MTPA and most of it is in Polypropylene. BEPL’s is 1,37,000 MTPA and only in ABS. INEOS is BEPL’s largest competitor in ABS and BEPL is a larger and lower cost producer than INEOS. So if Kingfa is producing ABS, it’s not a very significant amount in my opinion.

disclosure: completed one investment cycle ending in 2018. Bought again at 30-40 range in the last two months

4 Likes

Capex will give BEPL an advantage in the future for sure.

This is what I said in my post as well. Maybe recent Capex could add few points to margin

may I ask where you got the ABS prices from

from screener.in you can check import export prices of all goods.

Comparing OPM to crude prices won’t give you much info because in the 2018 AGM Mr. Bhansali himself said that crude doesn’t play much of a factor in company performance, INR fluctuation has a bigger effect.

Its good to triangulate what management is saying by comparing the available data at hand. I understand that things went downhill from the fire accident and company had to procure HRG as high cost.

Rather than comparing OPM to crude oil or ABS prices, a better evaluator would be to compare ROCE over the longer term.

Idea is to understand the cyclicality and possibility to take the ride but entering at right time, which you seems to have done as well.

10 year CAGR ROCE is 23% and 10 year CAGR Earnings growth is 30%, which means that over the last 10 years not only has the company been able to grow net profit at a healthy rate, they’ve done it at a rate far above cost of capital. In my opinion this would be a better indicator of a long term compounder.

if you look at the historical earnings/ROCE… it started improving from 2015 which also coincided with fall in crude… which made me think and compare the crude prices… that was another rational why compare crude.

So if Kingfa is producing ABS, it’s not a very significant amount in my opinion.

wonderful… good to know…

Discl: I don’t hold any BEPL… but considering and studying.

3 Likes