Dear @Agarwala,

Although there is a general perception that the promoter pledging of the stocks is negative, I feel that, there can be cases when it would be considered to be as positive also. If the promoter is pledging stock to raise capital to purchase additional stake in his/ her profit making business, it can be considered as hugely positive.

In case of BEPL, I think, there are strong reasons to believe that the stocks pledged many years back have not been released as yet for positive reasons. Let me explain my thought process below. As I am not the most experienced person in the stock market, I could be wrong in the following logic, hence request anyone to correct me, if you find a flaw.

Currently, there are 5,00,00,000 stocks which are pledged by BEPL promoters. These stocks were pledged many years back (I do not know the exact date). BSE Shareholding pattern has started including the Promoter Pledging information starting from the Mar-2009 Quarter, hence let us take that Quarter as a reference point and make our judgement based on that.

As of Mar-2009, promoter and promoter groups owned 44.82% of the stocks of the company and 67.24% of the above stocks (5,00,00,000) were pledged. 2009 was the year when the company had made a loss of Rs. 11.42 crores. BEPL’s share price during the Mar-09 Quarter was around Rs. 9, hence let us assume that the market capitalization was around Rs. 149 crores. Out of the above, the value of pledged stocks would come to be around Rs. 45 crores. Let us make an estimate that, the above pledge helped the promoters to obtain a long-term loan value of around 36 crores (80% of the total pledged stock value).

Subsequent to Mar-2009, company had never made any losses and made a cumulative profit of Rs. 146.54 crores till the Sep-17 Quarter. Hence, it could have easily fully paid back the above loan of around Rs 36 crores, considering that, the only major expense the company had since Mar-09 (as per my best guess) was the Rs. 40 crores used for capacity expansion at Abu Road from 51 KTPA to 80 KTPA.

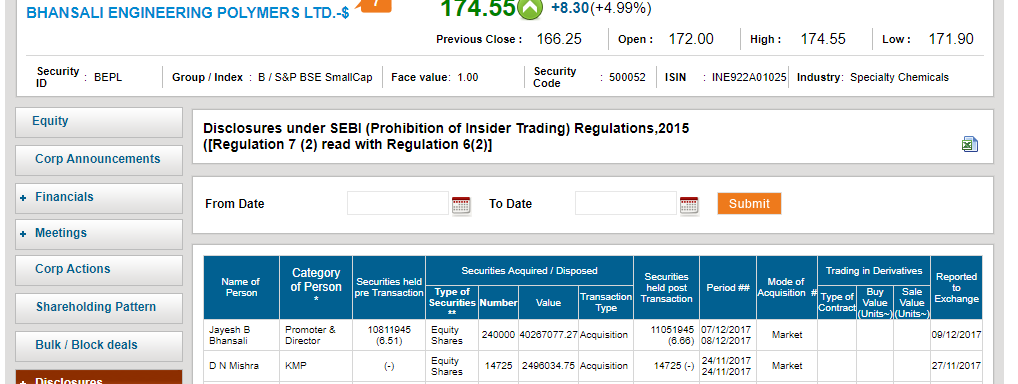

However, the above loan did not get settled till date. Why? Because the promoter wanted to buy additional stocks of the profit-making company and for doing the above, they needed money. Instead of settling the loan, they used the surplus money for purchasing the stock of the company. As a result, the promoter holding now increased to 54.25%, as against the 44.82% in Mar-09. In fact, the current promoter holding could have been even more than 56%, had some of the promoters were not reclassified as public shareholders during the Sep-17 Quarter.

Now, assume that, you were the promoter of the company. Would you have done anything different? Let me tell you, what I am doing. I have a housing loan which I could have settled fully very easily. However, instead of settling the above, I invested the surplus money in stocks like BEPL. Reason is that, I am expecting much higher return from BEPL investment, as compared to the around 9% yearly interest that I am paying on my housing loan currently.

BEPL promoter is not the only one who is doing this. Please read the following article for another example. KPIT stock price appreciated around 40% since the promoter had purchased additional stocks this way since Mar-17: