There has been some promoter buying last week. Please check BSE.

Yes I am also surprised that Promoter is still buying. Excellent for Retail

There has been some promoter buying last week. Please check BSE.

Yes I am also surprised that Promoter is still buying. Excellent for Retail

Hi nil

Promoter buying may explain this series of UCs.

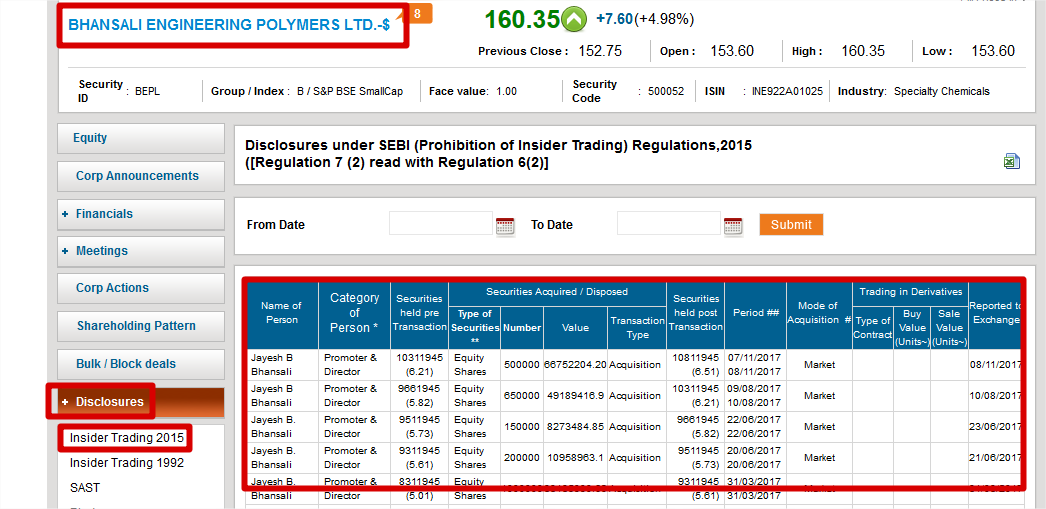

Hi nil_71, Can you please let me know how to check this info in BSE ? I generally check in bulk/block deals tab but I did not find any such info. Really appreciate your response. Thanks in advance.

There used to be prolonged lull periods for the stock after Q4’17 and Q1’18 results. However, after the Q2 results, the stock is exhibiting a different behavior. Stock is on a continuous rise, especially after the analyst/investor meet during the last week of October. I think, people have started believing more and more the story of the company, as it has come up with outstanding results quarter after quarter. Also, the analyst meet might have worked as a catalyst.

Bhansali in UC every alternate day. Wondering who is buying so much ?

In response to your questions, I can raise some more questions. INEOS Styro is showing technical weakness, while BEPL is moving up and up. Why is it so?

One possibility is that BEPL is acting as some sort of disruptor that is leading to weakness of the competitors. I will personally like to subscribe to this theory. Although I will very much like this view to be challenged. The other possibility is that some pump and dump operation is going on in BEPL.

nil_71, can you once again find out the price trends in ABS and its raw materials? You have done that in the past and have made significant contributions to this thread. Promoters have bought at 125-130 levels also. Does that mean a good current quarter? The possibility is that favorable pricing structure persists for BEPL.

I see a clear pattern between Avanti in early year and Bhansali now. Duopolistic Market, Domestic demand that is steady and Avanti has a passionate person to drive it.

That is why for Bhansali - execution and management walking the talk, very important.Because there is a long runaway ahead. Also nowadays Refrigerator is must have item in all Indian Households + huge demand of 2 wheelers + 4 Wheelers selling in decent nos. With reduced GST - just a good execution will increase it market cap

Only headwind can be if LG Chem decided to setup the plant tomorrow but still there is a huge demand-supply gap

Dinesh Rohira of Moneycontrol again bets on BEPL

Unchanged S&P rating, F&O expiry to keep markets volatile — 4 stocks to bet on

In the annual report, apart from promoter shareholders, there is a list of top 10 shareholders and statement of change in their shareholding. For all the non-promoter shareholders who are listed there, instead of buy/sell, it is mentioned under “transfer” category. So what does it mean ? Shares are transferred to other subsidiary or how to read it exactly ? Am talking about page 61 in annual report. Thanks.

Key management person acquires shares of BEPL

According to BSE DN Mishra acquired 14725 shares on 24 November 2017.

Following article (dated 13-Nov-17) mentions that Asian ABS prices have risen ~40% since the beginning of the year primarily due to higher demand in China for automobile interiors:

https://www.pressreader.com/india/money-times/20171113/281633895523107

Also, as per the following article, ABS market is to register a CAGR of 6% over the period of 2016-2024. Mounting need for light-weight automobiles to improve the fuel efficiency of the vehicle is primarily driving the ABS industry trends: https://www.openpr.com/news/813873/U-S-Acrylonitrile-Butadiene-Styrene-Market-to-exceed-3-1-billion-by-2024.html

Hi Madhavikutti

Let us do a quick calculation. Sales of FY17 = 626 crore with 55 KPTA capacity utilization. Let us assume full 80 KPTA capacity utilization of FY 18, so sales of around 910 crore for current year. Now assuming a 40% increase in realization due to increased ABS prices, the sales would be around 1275 crore. This will result in sales of around 320 crore for current quarter. Net profit could be anywhere in the range of 32 to 40 crore. There are lots of assumptions in this calculation. Therefore the final result could be wide off the mark. But this may be a reason that the BEPL is going north almost vertically.

Hi @Agarwala, I think, it will be better to extrapolate the Q3’ 18 numbers from the most recent results, which is Q2’ 18. While I will not make any attempt to predict the Q3 numbers, let me provide a few related points:

Looks like, 40% increase in the ABS price had happened during the period of Jan-17 to Sep-17 itself, as I can conclude from some of the news articles which I went through. However, the following article suggests that, bulk of the above increase would have happened during Q2’18 itself: https://www.icis.com/resources/news/2017/09/01/10138341/asia-abs-soars-on-upstream-gains-demand-outlook-uncertain/. Any way, we can assume that, the Q2 results alreay carries the positive impact of the 40% price increase to a certain extend. I am not sure about any subsequent price increases since 1-Oct-17 (beyond the 40% mentioned above).

While I am not sure about the capacity utilization for Q2’18, following article mentions that, Q1’18 utilization had already increased to 85% (I am a little doubtful about this figure though): http://www.moneycontrol.com/news/business/bhansali-enggs-capacity-expansion-targets-sales-guidance-give-it-earnings-boost-2327369.html . If we trust the above 85% utilization figure, let us approximate that utilization in Q2 was 88% and in Q3, it will be around 90%.

Hi Madhavi

Thanks for the contra view that is what makes VP a great place. In the meantime I have dug out some information about ABS natural prices in Central Europe. It comes to about 2.6 Dollars per kg. Here is the link … Does that mean a rise over September price that is 2000 Dollars per tonne, as per the article that you cited. In the mean time SAN price seems to have declined.

@vipin111 thanks lot for this report. While I am not focusing on price but report is truly gem given the wholistic nature of the same

Guys- all the pricing assumption will get cleared. BEPL does 50% LT contract and 50% spo

Welcome nil_71.

Fanatic promoters can create fanatic wealth. If one can identify these people early even a few or maybe 1 stock is enough to take ones investment journey through!(Eg: Indra Kumar of Avanti)When I was at the AGM all were busy looking at the balance sheet and none listened to what the promoter had to say. Balance sheets can be cooked up so it is very important to see and hear the Guy we are entrusting our money to.Target is machli ki aankh(Fish’s eye) as Arjuna did.

Hi Gaurav

Thanks for sharing. Trinseo ABS project is actually a recommissioning and reconversion of a mothballed polystyrene plant. Its capacity of about 80 KPTA is likely to be locally absorbed in China. My worry is that one of the global ABS majors may enter India.

I think this one will give 100% revenue growth for next two quarter which makes it attractive in spite of huge run.