Given the swap ratio, if I buy 1000 shares of Gruh now @ 229.10, I will get Bandhan Bank @ 229100 / 568 = Rs. 403 per share. But Bandhan Bank’s share price as of now is 429. Normally such anomalies in the prices gets adjusted within a day or two of announcement but in this case the price arbitrage remains few days after announcement. What am I missing? Is my understanding wrong ?

Request senior members to suggest if I should buy Gruh or Bandhan. I am interested in buying Bandhan with a view of 5 years time horizon.

This discount remains till the time deal closes. There is always a threat to a deal, so these discount are always there… they range between 4-6% in the start and then narrow down with completion of every regulatory step.

Since you want to buy Bandhan bank, why not buy gruh and get 5% discount on the price of bandhan? Also, if the deal falls apart, IMO gruh shares will recover more or fall less since, gruh on announcement fell much much more than bandhan.

In continuation to my earlier post on experience with account opening,let me add some more.

Staffs are not so active in account opening formalities regarding documents verification. I had to call them multiple times on status and re submitted my rejected identity proofs.

Had to escalate the delay to nodal office then concerned branch manager took it up seriously and processed. 11 days to open account from application, still internet banking facility not activated.

They will ask ten thousands rupees for five thousands rupee min balance account. There is no specific guidelines or bank rules like this, on escalation they admitted it they request customer like this. Simple way of fund raising, a big negative to me.

Will closely monitor banking activity. A good thing that I joined their network to track them better.

Small finance banks have an important role in promoting financial inclusion & priority sector lending. Will hold meeting with MD & CEOs of small finance banks tomorrow(15th March 2019): Tweets @RBI Governor, @DasShaktikanta

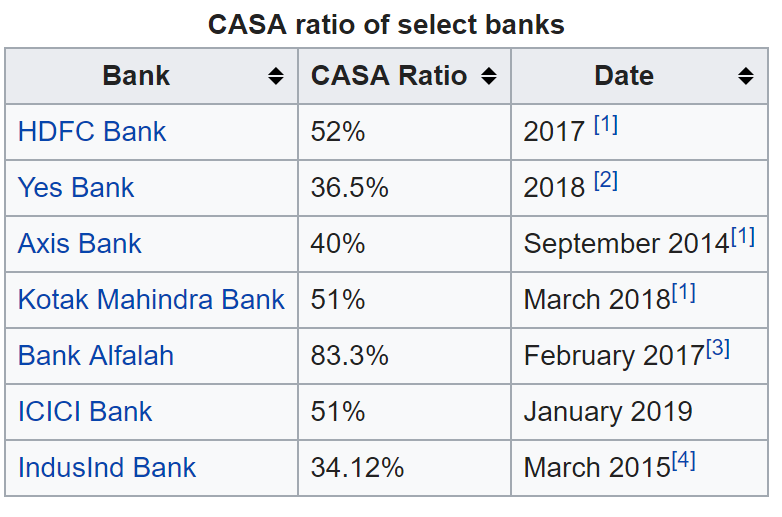

What is somewhat underappreciated in case of Bandhan is its casa ratio. A high casa ratio is the bedrock of any commercial bank and with a 41% casa ratio built within 3 years of operations is phenomenal. Incidentally, HDFC Bank also has the same casa ratio after 25 years of operations.

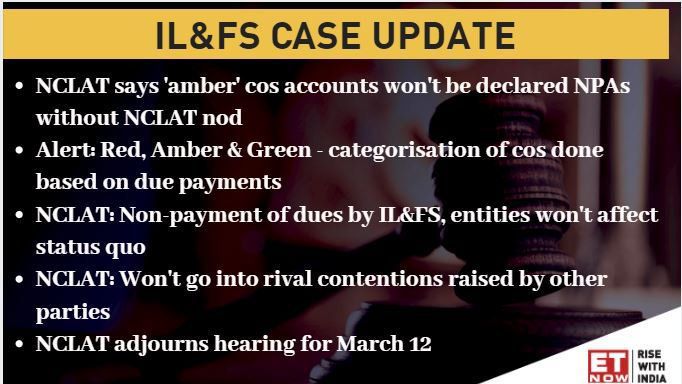

There are enough positives to flow for Bandhan in the short/medium term. Falling interest rates, some relief from RBI post merger of Gruh (& consequent reduction in promoter holding) as well as hopefully strong earnings growth in Q4 2019. With NCLT disallowing banks from declaring ILFS exposure as NPA without its permission, I wonder the fate of the conservative full Rs 385 cr provisioning already taken by Bandhan on its ILFS exposure.

Dividends payout is likely to be lower by combined Bandhan + Gruh. Bandhan standalone had a dividend payout of around 10% compared to around 40% for Gruh standalone

The only way to reconcile with a lower payout is that Bandhan + Gruh should grow much faster than Gruh standalone and therefore needs to conserve capital. It will be interesting to see the growth during the 4th quarter and therefore full year FY2019 for Bandhan. My personal feeling is that the growth is going to be good.

Since its launch three and half years ago, Bandhan Bank reported zero NPAs under the Pradhan Mantri MUDRA Yojana (PMMY)/Mudra Loan. Another remarkable achievement by Bandhan Bank.

Last week, the bank got approval to open 25 more branches.

Will grow affordable housing portfolio aggressively post merger. Was expected, as Gruh gets an additional geography (East India) to offer housing loans.

As per Ghosh, there is a ‘good plan’ to bring down the promoter holding to less than 40% (something which has been keeping the stock depressed).

In a more detail interview here Mr. Ghosh mentioned on reducing stake. I quote " For reducing the balance amount, we are planning an offer for sale (OFS) or any other way. We are very closely working on that process and whenever it comes, we would like to inform you accordingly.

But we are very clear. We will complete the process in compliance with RBI regulations".

If the OFS goes through, then we are done with the dilution overhang/RBI sword hanging over Bandhan’s head. Yes, HDFC would still need to bring its holding down to 9.9% in the merged entity from 15%. Once that is also done, the game will then move on to profit growth. To begin with, I am expecting good growth from Bandhan this Q4 (fingers crossed).

The ‘playing by the book’ will get further reinforced for Bandhan unlike another large private bank led by UK which has taken the RBI to court to postpone promoter dilution as far out as possible. The full earnest with which CS Ghosh is going about in order to meet RBI’s conditions has made my respect for him go up one notch.

In my view, and i am willing to be proven wrong, it is dishonest if not downright hilarious by this other private sector bank led by UK to argue that issuance of non convertible preference share should meet RBI’s requirement of equity dilution by the promoter (when any finance student will tell you that the RBI’s intent was for dilution of promoter’s control over the bank and not just any capital dilution). The irony is that UK recently headed the Kotak Committee which gave its recommendations on improving corporate governance standards by listed Indian companies. Easy to lecture others but difficult to implement when it falls on you. My respect for UK clearly fell one notch by his move.