Less than the margin in India. How does it help the company over the long term?

This is mere 7% of capacity . this will be offset by a) 5% countervailing duty which Indian imports face b) lower cost of $ debt c) local state incentives in the US d) lower income tax rate of 21% in the US.

Even considering everything post Tax RoCE would be 7-9% for the US entity vs 16-18% for the Indian unit of similar size. We need to consider this shortfall as Marketing Spend - creating better traction with clients and bringing in more future business.

Company has made it clear all future expansions would be in India. So this one-off US investment is more to build a strategic presence and visibility to OEMs.

5 Likes

To long term Balkrishna investors if can provide answers to following questions

-

Any idea why operating margins dropped from 20% to 13% in 2009 and 2011.

-

How much does crude difference ie Brent Crude vs Nymex Crude has impact on Balkrishna Industries . Since the current difference is $10 ie US crude is cheaper than Brent and it is expected post Iran ban in Nov this difference will increase to $15 … would like experts to revert on this area …

Thanks :

Discl : Planning to invest

This is self-service forum, kindly help yourself ![]()

It is great to have questions you don’t have ready answer to, but one should attempt to find a solution.

A sincere attempt would always find enough guidance on VP. But don’t expect spoon feeding please.

4 Likes

In current market suddenly there are multiple opportunities … one need to take lot of screening calls so that one can focus on important ones . In stocks which I know , if some one ask any questions I will answer on valupickr . By the way I thought that is why this platform is there … to enable screen ideas , clear doubts .

As I understand you are tracking this stock from 2012 , if you can answer above questions great , otherwise no issues … But if you need any answer on any stocks which i own , I would love to help you out

Regards

-

Operating margins fell YoY in FY09 and FY11 due to gross margin compression in both of those years. In FY09, the primary causes were extreme exchange rate volatility and surges in the price of both natural rubber (NR) and crude oil derivatives. In FY11, the main driver was an unprecedented spike in the price of NR (due to a brief under-supply in the NR market, which set the stage for a prolonged planting boom that has kept NR prices in check ever since). While Balkrishna enjoys some pricing power (particularly relative to makers of mass-market CV/PV tires), price increases always take effect with a time lag.

-

India does not import Brent crude; Brent is merely cited as a global benchmark. India has its own benchmark, derived mainly from spot prices in the Middle East (the source of the vast majority of India’s crude imports). As for the Brent-West Texas/Nymex spread, Iran certainly has an effect, but the bigger factor is inadequate pipeline capacity between U.S. shale basins and Gulf Coast export terminals (which is leading to rising inventories at Cushing, Oklahoma - the price settlement point for West Texas crude).

2 Likes

Thanks for clarification . It was useful .

-

As I understand Balakrishna Industries might occasionally have these hiccups of 13% kind of OPMs becos of exchange volatility and RM cost movement ( which is depended on crude oil ) but in long term it can sustain it above 25% .

-

Balakrishna opening tire Factory in US in interesting … It reminds us how Chinese producers reacted to Obama tariffs in 2008

In 2009, American tire makers persuaded the Obama administration to impose tariffs on Chinese tires, and imports of tires from China fell sharply. But Chinese companies did not stop making tires in response to the tariffs — they simply moved production to other places, including to the United States.

Giti, one of the largest tire makers in China, built the South Carolina factory to make low-cost tires for Walmart. Two other Chinese tire companies are building plants in the neighboring states of Georgia and North Carolina, and a fourth Chinese company acquired a tire factory in Georgia this year.

Thanks Again … I am studying the sector will revert with any pointers

4 Likes

I was going balkrishna industries balance sheet.interest paid is very less when compare with their debt levels.

Am I missing anything?

Off-highway tyre manufacturer, BKT reported weak set of numbers in Q2FY19. Standalone revenue was up 19% yoy (down 3% qoq) at Rs1,325cr, lower than expectation of Rs1,402cr. The company was able to keep input costs in check; however, higher operating expenses led to EBITDA underperformance. At Rs333cr, EBITDA was up 9% yoy (down 7% qoq), missing estimate of Rs402cr. EBITDA margin contracted 226bps yoy (115bps qoq) to 25.1%. Standalone PAT was marginally lower than expectation at Rs222cr,

up 10% yoy (down 3% qoq). The company declared second interim dividend of Rs2/equity share.

Other Highlights

-

In its Investor Presentation, the company mentioned the following steps to boost growth:

i) Replacement of Waluj plant with a new plant in the vicinity at a capex of Rs500cr. The plant will have capacity of 30,000 MTpa and will be operational by CY2021. ii) Capex of Rs500cr for manufacturing larger sized tyres at Bhuj. This will broaden BKT’s product portfolio and increase penetration of the BKT brand. iii) A carbon black plant of capacity 1,40,000 MTpa is under construction at Bhuj with capex of Rs425cr. Of the total capacity, 60,000MTpa will be operational by March 2019 and the rest by March 2021. -

Total volume in Q2FY19 was 52,339MT, up 12% yoy (5% qoq). Volume guidance for FY19 is between 2,10,000MT – 2,20,000MT (lowered from 2.25-2.3 lakh MT earlier) ; growth of 5-10% with respect to FY19,

Any views are welcome

3 Likes

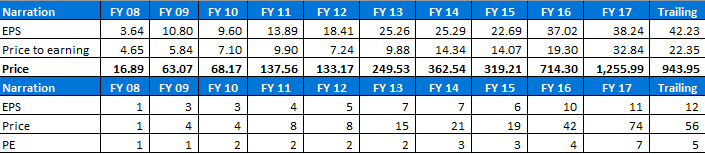

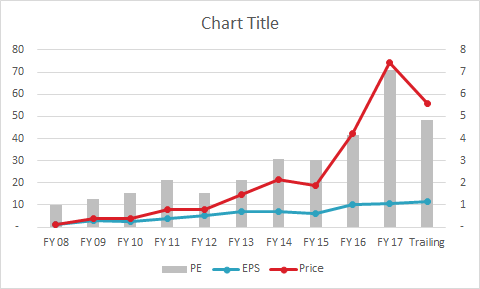

In 10 years, EPS is 12 X, Price is 60 X, thus PE expansion of 5X

Price has run up much ahead of earnings. Currently 35% lower than 52 week high. I expect further correction, may be another 15-20%.

Pls share your views…

2 Likes

Whether it corrects or not, ten years down the line it won’t matter.

2 Likes

I am a novice. Am not able to understand much of the finance jargons. But if you are thinking of 15 to 20% implies a short-duration investment.

By experience i have observed that buying any good company much below its 52w high will give you positive if not excellent returns. The returns are directly proportional to the amount invested in the company.

Moreover, for a good company I do not worry much if it is in an expansion spree, cause they know their company better than me. What I remain worried of is just the quality of management. But since they pay out dividends am not worried of it either.

I don’t know whether my comments would be helpful or not, but am just giving it out.

Would like to have your views on my thought process @hitesh2710, @phreakv6.

Thanks

Growth stocks seldom give this opportunity. And the ones who do are really not all that good.

If Nifty itself does a 52W low, then it is a good opportunity. Many good stocks too will seriously dip.

From where did you find this chart??

Correction may be possible but it is not a long term issue if it retains Competitive adv …

but key to understand here is will Balkrishna retains it’s competitive adv if US makes them to localise production . It has happened in IT and Pharma over last 5 /10 years . It can happen to Balakrishna industries too …

Unlike IT & pharma which are low on assets and hence is not a big problem for them as variable cost across new Indian firms and US firms will be same , but for balkrishna to compete with US firm it will be difficult as it have high cost plants vis a vis depreciated low cost plant of US firms .

Recently we have seen this problem surface for many Indian companies when they tried to have manufacturing capacities in Europe and US … They starting losing money big time …

I beg to differ on this.

They have clarified that this is one off US investment (which is 6-7%) of their total capacity.

Markets are overreacting and this is a good time to SIP this.

2 Likes

Investing capex, opening labs, inaugurating offices, buying out companies & even hiring locals in USA or foreign countries have not been a sweet dream. Often it is painful from financial perspective, let alone regulatory, anti competitive and compliance dynamics.

BKT has grown volumes at 9% CAGR for the last 5 years even as the global OHT industry has declined. However, now that the industry is expected to grow at 8-10% for the next 3 years, volume guidance remains muted @ 5-10%. I think they may be reaching a saturation of the customer base which is solely driven by price. The next set of customers may be harder to acquire only on price differentiation and therefore expenses will rise and margins may decline.

There are other indicators for this as well:

- Launch of USA plant as a necessity to penetrate Americas. Management has said that the customer base they are targeting requires faster delivery schedule

- Addition of larger diameter tyre manufacturing capabilities at Bhuj which require much more capex than small diameter tyres

Conversely, these initiatives could propel BKT towards double digit market share. In either case, the valuations were rich and even now on the higher side given the uncertainties.

Disc. was largest holding in PF. Exited in Sep due to valuation discomfort.

1 Like

The current PE ratio for Balkrishna Industries Ltd is 22. If this is high, iyo, what would be a reasonable PE ratio?

PS: last five year sales growth is 6.88% as per screener. You say vol grew by 9%.

Volume = number of tyres sold

Revenue = No of tyres * price per tyre

If rubber prices are benign, price per tyre may decline and then revenue growth will be lower than volume growth.

You can read about the business model of BKT in this thread.

3 Likes