Another innovative product launched by HDFC Credit Card is ‘Easy Dinner’ in the line of Zomato Gold…Got a message yesterday

Hello all

I visited few large offline stores today. The sales for the season looks decent and robust. Since I am invested in bajaj finance I wanted to check the finance dept also. Finance was available for almost everything costing more than 5k.

Few imp observations .

- There are multiple finance options now avb to the customers like hdb , bajaj , capital first . Few places there were banks also offering credit.

- All the stores I visited the terms and conditions were more or less same.

- Inspite of point no 2 there was lot of business at the bajaj finance counter . Will it be sustainable on the long run. That has to be figured.

- Can some throw some light on hdb which is a subsidiary of hdfc and since when has it started operations , their presence and further future plans .

- We also need some ground level check on tier 2 and tier 3 cities. Are there too multiple options available for consumer durable business.

- If there are multiple players in all the cities , then this business is getting overcrowded. Retail npa and gnpa should be same for all as all do the same background check and documentation.

Regards

Divyansh

4 Likes

Add Tata Capital consumer durable loans especially active in Croma stores.

Interview with the founders of Mobikwik in the Forbes magazine. BFL owns 12.6% stake. Mobikwik is transforming from a wallet/payments business to an online credit business. The founders claim to have financed 300 crore worth of loans so far and aim to have a loan book of 1500 crore by March 2019.They also mentioned that Mobikwil plans to go public in 2-3 years.

We can build a company like Bajaj Finance over the next few years. In fact, we intend to go public in two to three years.

However, in 2016, one of the founders had claimed that Mobikwik would be profitable by April 2018. For FY18 their losses were 132 crore on a revenue of 85 crore. Last year the company was looking at raising Rs 1000 crore at a valuation of Rs 4,500 crore to Rs 5,000 crore. Eventually they ended up raising 225 crore for a 12.6% stake, from Bajaj Finance. So I would take their projections and aspirations with a pinch of salt. It has seen a string of top level exits, and is frequently in the news with rumours of trouble and shutting down.

Mobikwik claims to sanction paperless loans, upto Rs 60,000, in under 90 seconds. I downloaded their mobile app (on iOS) to try out the instant digital loan. However, it seems to be offered only on the Android platform. Has anyone else tried it?

4 Likes

Has to be as same group companies

I was looking at the annual report of HDB financial services . Hdb finance is a nbfc and subsidiary of hdfc bank. They are now present in 831 cities and their loan book is also growing at a scorching pace. For fy 17-18 their loan book is around 44000 crores with a net profit of arnd 1000 crores. But their annual report does not throw any light on their future plans and breakdown of loan disbursed to various segments. Being a hdfc bank subsidiary one can expect the quality of book to be excellent and also sustainable. Another crown jewel in the making for brand hdfc. In my guess since this subsidiary has been delivering from past few years and so has been bajaj the consumer space as of now is offering growth opportunities to both. But for someone who wants best of both the world’s . Part investment in hdfc bank along with bajaj finance might be a decent idea to ride the nbfc theme focusing on consumer market.

Regards

Divyansh

1 Like

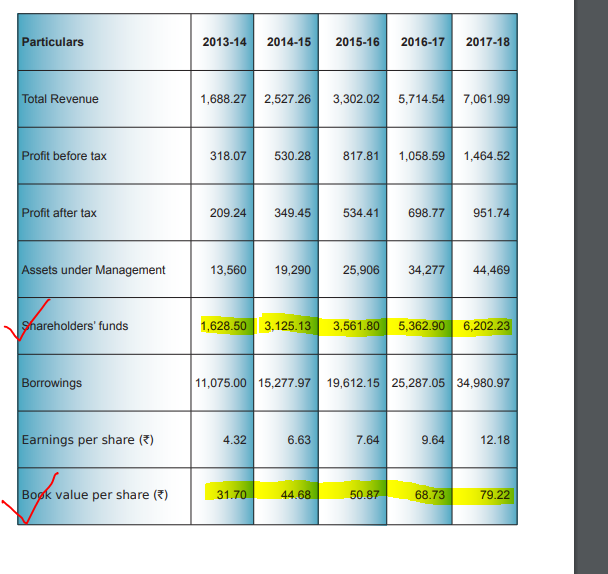

HDB Financial’s ROE is lower than Bajaj Fin. Comparing Share holder fund and Book value is indicating that in 2014-15 and 2016-17 they got equity infusion but for other years Book value growth is indicating that ROE is within 13-16% range. Consumer Loan ROE is generally 20% +.

1 Like

Results Announced. Looks good as usual.

4 Likes

Its a usual dhamaka result and most importantly they don’t see any issue going forward - whether its growth or margins or asset quality or liquidity etc…They say cost of funds will not rise for short to medium term(interview to ET now).

7 Likes

It seems business as usual for BFL if you go through the interview. Rajeev Jain is of the opinion that the liquidity crisis in 2013 was worse than what it is over the last month or so. Everything seems status quo at the moment for BFL.

7 Likes

How do you see the demand in terms of consumer finance business shaping up? Can you sustain AUM growth at over 35 odd per cent?

The demand outlook remains reasonably strong. We are in the middle of a festive season. We are seeing reasonably strong discretionary consumption demand at this point in time. From a medium to long-term outlook standpoint, can we continue to grow upwards of 25% which is our guidance for many years? The answer is yes.

3 Likes

Q2FY19 Results Highlights:

- Assets under management up 38% YoY to 1,00,217 Cr.

- Net Interest Income (NII) up 42% YoY to 2,729 Cr.

- PBT up 55% YoY to 1,435 Cr.

- PAT up 54% YoY to 923 Cr.

Key Conference Call Highlights:

- Ratio of deposits to total liabilities has increased to 15% (was 14% at the end of Q1FY19). These deposits are broken up into 60% retail and 40% corporate)

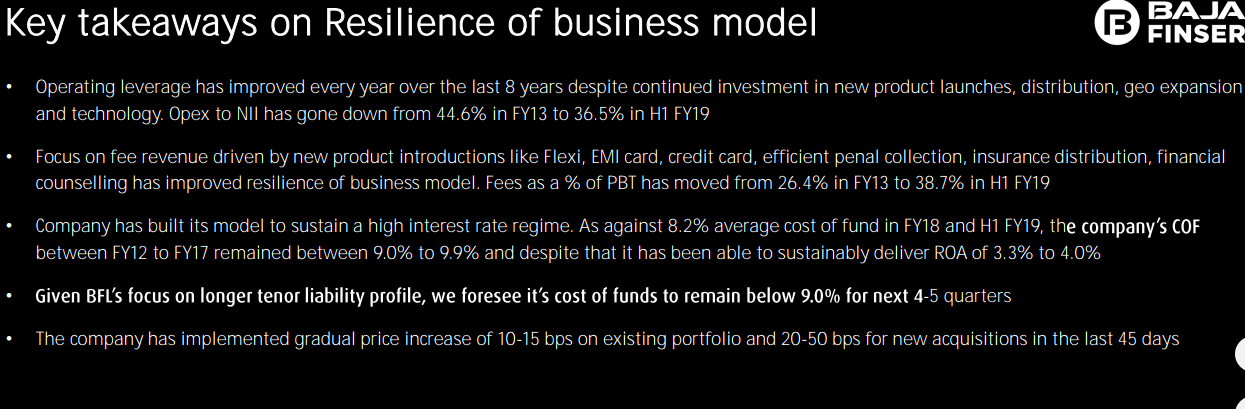

- OPEX to NIM falls strongly to 35.9% in Q2FY19 from 40.6% in Q2FY18. This is mainly due to strong focus on fee based incomes from EMI cars, RBL cobranded credit cards, BajajFinserv Mobikwik wallet, insurance distribution and other fee generating products.

- Cost of funds has gone up from previous year, however empirical evidence from previous years suggests that margins are not majorly affected by increase or decrease in cost of funds. As against 8.2% average cost of fund in FY18 and H1 FY19, the CoF between FY12 to FY17 remained between 9.0% to 9.9% and despite that it has been able to sustainably deliver ROA of 3.3% to 4.0%

- IL&FS exposure: Lease rental discounting for 2 towers in the GIFT city (Ahmedabad). The lease is operational and the tenants are marquee corporates (Domestic & international IT companies). Rentals flow through escrow accounts and BFL has exclusive charge on the underlying assets.Total exposure around Rs 225 crore.

- Developer finance business outlook: This is 1% of overall AUM. Per borrower limit capped at 50 Cr. Average is 11 Cr. So credit risk is fairly diversified.

- Banking license: If ratio of deposits to total liabilities goes to 30% in the next few years (is 15% now) then what is the need to apply for a license? However if that does not happen then BFL may apply. No such plans in the coming year.

- BHFL: AUM of ~10,700 Cr. Profitability lower right now however operational leverage will kick in after AUM crosses 18k-20k Cr.

- NBFC Liquidity crisis: BFL is well positioned in terms of asset liability matching. BFL & BHFL collectively raised over ₹5,395 Cr in money markets and ₹2,900 Cr from banks in the first 3 weeks of October. So this crunch does not affect Bajaj Finance. Empirical evidence (from 2008, 2013 taper tantrum crisis) suggests that such liquidity crises usually get over in about 50-55 days. We are already 30 days into this cycle.

- Growth outlook: Not much has changed on ground. The retail financing boom still continues. Demand is strong. Lumpy businesses like SME, commercial, securities lending (LAS) may see cautious approach given the current market conditions.

10 Likes

My take on the results:

- OPEX/NIM improvement due to increased focus on fee based income, repeat business due to EMI cards & co-branded credit cards, larger cross-sell franchise. As the number of cards (EMI, credit) in circulation increases the OPEX/NIM ratio will go down even further.

- This means that both RoE & RoA will go up. This will lengthen the runway until the next equity infusion is required.

- It would be quite interesting if OPEX/NIM falls towards 30% levels. Management however is cautious and has given a guidance of 39% as being a sustainable level for the next 2-3 quarters. However I am quite optimistic because I feel the investments in data analytics (for cross ell) and EMI/credit card franchises have started paying off. Operational leverage is kicking in, which would mean a lot for the stock’s valuation.

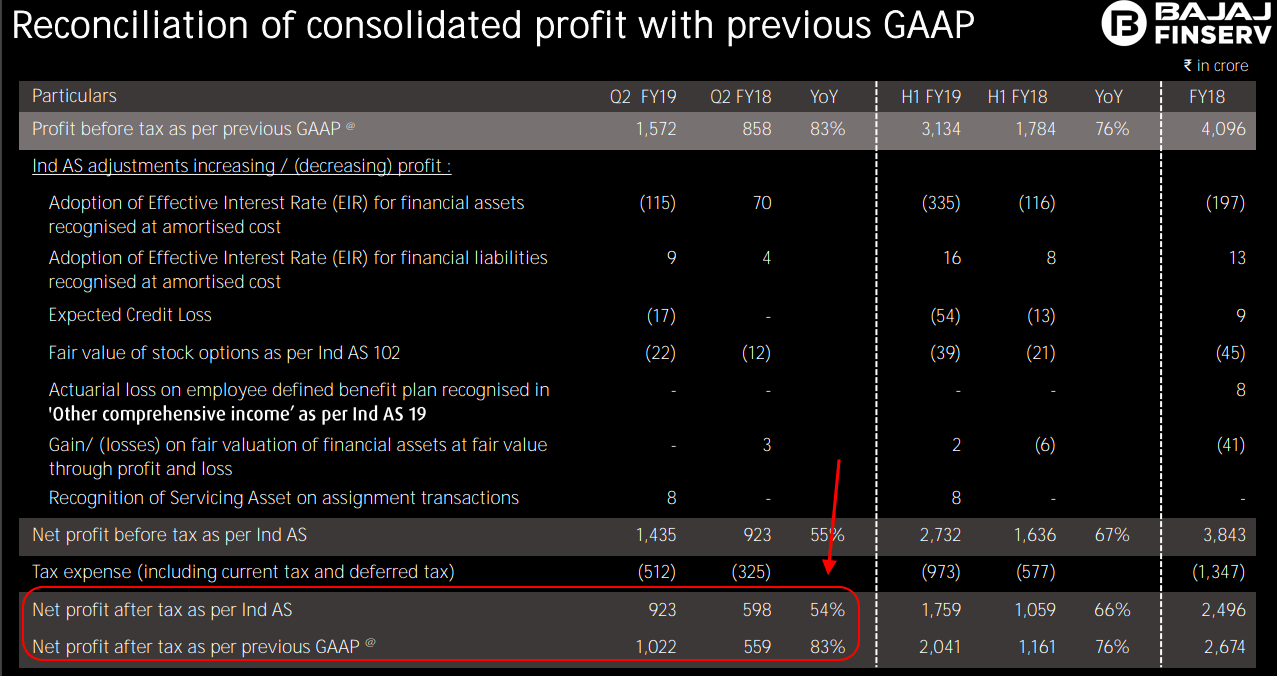

Slide 19 of the investor presentation provides a comparison for the PAT with Ind AS and previous accounting standard (Ind AS kicked in on 1st April 2018):

It shows a 83% increase in PAT as per the previous standard. I am not an expert in accounting and I don’t understand Ind AS and the previous GAAP. But an 83% growth is very very impressive, even by BFL standards. Especially given the current macro and liquidity environment.

8 Likes

Neither am i an expert in accounting and agree with ROEs moving up in future but remember during the last quarter, impact of the accounting rules was the opposite

4 Likes

Bajaj Finance’s latest filing with the exchange says the company issued NCDs at a coupon rate of 9.224% on 15th November 2018.

- NCDs issued on 25th October 2018 had a coupon rate of 9.3027%.

- NCDs issued on 29th August 2018 had a coupon rate of 8.6511%.

The IL&FS default happened in September and one can clearly see that the borrowing cost, even for a company like BFL, has gone up by about 500 bps (CORRECTION: It should be 50 bps or about 0.5%. 500 bps would be 5%) post the news of default. This is without even RBI raising the repo rate (The last hike of 25 bps happened on 31st July 2018). This is certainly going to affect the spreads for Q3. And it looks like it will take some more time for debt market investor confidence to come back.

EDIT: Corrected the quantum of rise in cost of funds as pointed out by @varun037.

2 Likes

its 65 base points not 500 (100 base point = 1%)… Yes the cost has increased… But this cost rise is for all players not just one. So, IMO, this cost can be passed to customer. Increased cost does impact customer buying pattern negatively so consumption may be lower overall. However, I feel that the growth for Bajaj Finance will be sustainable as some players under credit cruch will not be able to serve customers. I mean, the industry overall may not grow very well, but oppurtinites for well managed companies within the industry should grow.

Also as per latest data

The issue rate is 7.85% for Bajaj Finance.

1 Like

Thanks for correcting my mistake.

I agree. Other players would be more adversely affected.

I was in Latur, Maharashtra recently and visited a Sony showroom to buy a TV for our family. It was a small showroom and it had a dedicated person for processing Bajaj Finance applications. The salesman said that about 80% of their customers use the no cost EMI option of Bajaj Finance. I saw a stack of 7-8 BFL loan applications on his table. Documents required - PAN, Aadhaar, bank statement/passbook and address proof. There were a few other offers from HDFC and ICICI bank, but people preferred the no cost EMI option. There was virtually no competition for Bajaj Finance at the showroom. This reminds me of a line frequently used by the MD in conference calls “Competition fizzles out outside the top 15-20 cities. That is where the growth opportunity is”.

14 Likes

Thanks for sharing this… Yes Bajaj has first mover advantage and they know how to exploit that ![]()

1 Like

That means model is being replicated in tier 2&3 cities. A hugely aspiring demographies being catered to.