@armchairinvest_

Thanx for the concall notes, I think every thing is dependent on their execution and getting from nylon to Bcf and other value added segments

Q2 FY18 Results:

http://www.bseindia.com/xml-data/corpfiling/AttachLive/72fca0e9-3d96-475c-9495-582f49abb40a.pdf

1 Like

Any idea why the result is below average as compared to the sept quarter 2016? Is it due to their transformation from nylon to bcf which has affected both top and bottom lines?

No idea. Looks like the pressure on raw material continues. Need to listen to management concall for further details

So Tiexta/PTT/Dupont Sorona/Mohawk SmartStrand is a BCF fiber only and as the link points out, BCF fiber is relatively new in the market (assuming carpet life of 10-15 years) and it’s being pushed by Mohawk and Godfrey Hirst, but there is still some time for it to emerge as champion. Need to dig more into the demand for this.

I pulled out the financials of Mohawk and it seems to be doing pretty well. Performed well in stock market also over 6 year period. Also, it recently announced that it will acquire Godfrey Hirst - https://www.prnewswire.com/news-releases/mohawk-industries-inc-announces-purchase-of-godfrey-hirst-group-300559624.html

Disc: Invested - around 7% of portfolio

3 Likes

Please share Q2 FY18 con call transcript

5 Likes

AYM has a youtube channel and they’re updating regularly now. Can’t say that this helps the company do well per se, but might give some insight into what happens there -

https://www.youtube.com/channel/UCWgKLng90JkrKKrPA5V72fw

1 Like

FY18 Q3 Results: http://www.bseindia.com/xml-data/corpfiling/AttachHis/05e065dc-1df4-4d91-a3f7-5d623fef2b20.pdf

Company raising funds upto 80Cr, through preferential allotment of shares to Promoters.

http://www.bseindia.com/xml-data/corpfiling/AttachHis/05e065dc-1df4-4d91-a3f7-5d623fef2b20.pdf

Concall might give additional details for the purpose of raising funds:

http://www.bseindia.com/xml-data/corpfiling/AttachHis/e2acb309-c6aa-4d0f-90d8-ed34239a4c67.pdf

2 Likes

Please kindly share concall details of Aym syntex

AYM has gone for fresh equity infusion of 80 crores.

https://www.bseindia.com/xml-data/corpfiling/AttachHis/0865bd1f-1076-45d2-947f-fc513167a704.pdf

But 45 crores out of this is due to conversion of corporate loan - any idea what this is? As per last annual report, promoter company gave loan of 20 crores, if I’m reading correctly. So maybe that is being converted along with some other loan given during this FY.

Infusion will bring promoter holding up to 70% and with potential conversion of preferential shares up to 72%. At conversion price of 75, this is better than current market price of 66.

Discl. : Invested with 4% allocation.

1 Like

AYM SYNTEX

Highlights of Q3 and Nine month ended results

- Q3 Performance

o Revenue grew by 22.30 % to 227 Cr from 188 Cr last year same quarter

o EBITDA grew by 7% to 18.5 Cr from 17.24 Cr last year same quarter

o PAT fall to 25% by 3.23 Cr from 4.33 Cr last year same quarter

o PAT fall due to high expense on depreciation due to capex expenditure.

o Net debt of company grew from 6 Cr this quarter to total 239 Cr. - Nine month performance

o Revenue grew by 2 % to 633 Cr from 625 Cr last nine month performance.

o EBITDA fall to 49.9 Cr from 79.9 Cr

o PAT come down to 4.2 Cr from 31.9 Cr. - Total debt stand at 69.6 Cr increasing from March 2017 from around 46.5Cr. Mainly due to higher export receivables out of debtors above 180 days is only 0.6 Cr. Current ratio is 1.7 due to tight liquidity situation and lower EBITDA. Measure would be taken to strengthen the balance sheet till March 2018.

- CAPEX of 15.5 Cr has been done in this quarter and 43.6 Cr till 31st Dec.

- Company is going to raise fund by issue of equity upto 80 Cr to promotor on preferential basis as price determine by promotor in order to strength the balance sheet & plant expense.

- Business update last quarter

o In Nylon and Polyester textile business margin continue to remain under pressure. One significant improvement on Account of OEE the efficiency from 63 % last quarter have gone up to 84 % . It will continue in next quarter last 4-5 quarter it was down because due to lack of demand due to impact of demonetisation and GST. Several Lines are now getting back to work slowly and steadily.

o Difficult part is margin improvement :-

Negative news for nylon is antidumping duty after 11 years has been discontinued. Now there will be some inflow of material from Taiwan ,Korea and China. Company is much better position to tackle it and currently company is at peak level of selling in domestic market almost 60 % from the highest numbers. So it will convert to polyesters in export.

Antidumping duty will more affect to FDY segment the most in which company isn’t present at all.

Due to antidumping the real numbers will be known in next quarter onwards.

o Focus

Focus will be continued on system building to gear up high quality customers and next focus is on business development.

In last quarter company has added a prestige amount in denim space one of the largest denim maker in India with whom company has started bulk business in new project and company has also commercialised with one line running on domestic and export market as well.

On the Palgadh side work is going to make capacity utilisation better. At present it operates about 70% which is still not high enough but higher than last year. Company hopes that as going business development numbers, this numbers slowly and steadily increase. Multiple fronts have started working in this area.

In term of BCF focus on a move to bring three new products that company has developed in last 12 months. Company will also looking to expand capacity before of good customer response.

Q&A - In BCF front almost 6-7 lines are deployed to long term contract out of 9 lines . How can company manage the volatility of raw material prices in case of BCF ?

o It is based on quarterly basis, whatever change in price of raw material happen is automatically transferred. - In Palgadh plan does company have long term contract as company have in BCF ?

o It runs on a different business model, lot of effort are going to add better quality to have long term strategic customers. But the customers are on smaller in nature it is an different business model compare to BCF . Company enjoy strong brand name in Conventional dye space . Company have some old strong and loyal customers with consistency of quality. - Does Palgadh business effect due to change in price in raw material ?

o No raw material price is on immediate pass through on monthly basis. - Kindly give volume growth from prestigious customers in nylon and polyester division ?

o In this quarter there is small contribution of this customers which has been started in last year. Because it is a long process and they want to be comfortable before they ramp up with volume on overall they are consistent small in amount. Effort are there to go up slightly more than 5 % of revenue. Sampling has started but at certain sensitive product the entry barrier are high. - Other expense go up by 54 Crore , What led it to increase ?

o 1.8-2 Cr is from job work charges

o 1.8 Cr is from excise duty reversed into this quarter

o Manufacturing expense increase as top line increases. - What proportion of export is there to total revenue ?

o In this quarter it is 38 % of total revenue. This was due to one time trading activity in this quarter which will not be there in next quarter. So it will be around 17 %. - As crude prices goes up does corresponding realisation also goes up ?

o Yes due to crude price raw material price increase . Nylon price also go up due to increase in crude price . Some time there is a lag that lead to margin pressure. Mostly prices are passed to customers.

o But sales also goes up as raw material price goes up. - Why there is an increase in total borrowing ?

o Total borrowing is 300 Cr last quarter and this quarter it is just up by 6 Cr. In past it was more because of EBITDA doesn’t come out as expected and CAPEX plan of 15-20 Cr was there.

o It includes internal debt in which we take LC , all item that come under current liability considered as debt so it does not increase substantially.

o Working capital also gone up drastically due to GST impact but all will come to normal in coming few months. - Does volume will increase and CAPEX?

o CAPEX will be on side where there are long term strategic customers where company expect to get returns in long term.

o In textile there is margin pressure so product mix will be change and improve margin.

o Utilisation will increase but at what margin that has to look on it. In BCF fairly good utilisation. In Palgadh slowly and steadily utilisation also going up. It is about 70 % which is good from last year if company achieve more than 5 % then that will be good. - In polyester does company is getting expected returns?

o Efforts are going on but results are still not as expected. - Fund raise of 80 Cr is very high as compare to company Market share and promoter holding is already 65 % . Can you elaborate on this?

o It is both for capex and extend balance sheet. Board is yet to decide an amount as well as quality of balance sheet. - 28 % of revenue growth is there in last last quarter but EBITDA margin doesn’t improve any reason for that ?

o There is low margin in trading activity that goes up last year so overall margin are much lesser then normal margins. Growth was skewed because of trading business. This will not be there for next quarter. Next quarter will be more realistic. - What was the trading sales number as of total sales?

o It was around 10-12 % of total sales. - Company can raise fund by right issue then preferential issue?

o It is a very lengthy process and there are lot of norms to follow so we find prefential is best. - What company is expecting from fund raising ?

o After fund raising debt to equity will come down & company will have better return in long run. - Fixed asset of company has gone up substantially in last three years, any specific reason ?

o In last One and half year a lot of CAPEX has gone toward non-production. After this CAPEX there has been increase in Fixed assets. In future more CAPEX will be done in increasing productivity. - Explain more on Comfil brand ?

o Launch two new brand in textile

Comfil :- Launch in all segment in BCF segment and conventional segment.

Wonderfill :- It is a type of yarn use in carpet space.

o These are new product and company is working on it from a year and half. Now attraction is getting on it. - Kindly update on UK customers and some commodity?

o UK customers are there and they have increased exposure with AYM and slowly it Is increasing the volumes.

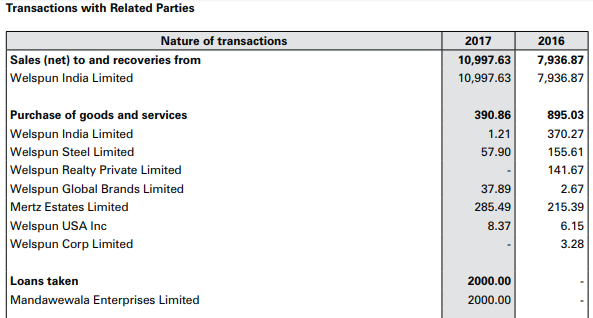

o On semi commodity that was running one line of production is now running on two lines. Sampling has started of high range products. First order will execute in January. Both brands are for export and domestic as well. - Does we only sell BCF to Welspun or other things also?

o We sell BCF and other products as well. - If Welspun as a customer moves away they can we manage the same number of CAPEX and utilisation?

o Yes we can because none of customer is more than 10 % of total revenue of company and Welspun is lower than 10 % . So it will not affect us if Welspun goes away. - What is company annual maintenance capex ?

o Around 6-7 Cr a year. - Can you classify between productive and non-productive CAPEX ?

o Lot of capex is toward land & lab building. Some of them has gone in machine upgrading . In 2014-15 some capex has gone toward capacity expansion where we don’t get the expected return. Some CAPEX is used in nylon space. - Give Outlook on nylon business ?

o Due to anti dumping duty it is not good . But volumes pick up and margin is still an issue. So to get out of it company has to focus on semi commodity and speciality segment. - Due to volatility in raw material prices does company have any long term tie up for raw material?

o No - If the nylon business is not running then why company don’t sell of it and shut down or transfer to polyester?

o It is not easy to sell off it will be stop contributing if it sell off but the fixed cost remain same and margin will be worse.

o In conversion to nylon market there is no barrier to entry and nylon was selling at very high margins like hot cakes but due to demand supply mismatch and anti dumping duty the margin compressed.

o From last two year the focus is on how company will be able to add good quality customers and more sustainable business to portfolio when there are certain barrier to entry. - How company decide to build new product and share some information on R&D department ? What is your hiring policy ?

o New product is decided by a mix of internal and external . In last 3-4 month it is more on external basis on customer feedback.

o In term of hiring policy company have full team of R&D where M.tech and B.tech are hired who work on new product. - Which companies are role model to follow ?

o Companies like Aquafine and trevire base in Europe are company’s role model. - Does company belong to low cost player among other peers?

o No , Companies like Reliance , Alok Industries are 10 times more than us in size and focus is on reliable quality , order and supply for having success. - Management Comment

o One Should not expect any miracle in short run It will take time and keep patience .

4 Likes

DuPont shutting down product line at Chambers Works

What could be the possible impact on AYM?

I think its nothing to related with Dupont Sorona brand…

As per AYM concerned, it is exclusive manufacturing partner of Sorona brand of Dupont in India and as per managment it will take atleast 2 years to material revenue to come from this partnership…

FY18 Q4 Results:

Q1 fy 19 results https://www.bseindia.com/xml-data/corpfiling/AttachLive/953efe83-f9f6-48db-93f1-a5b3e53b6e32.pdf

These guys don’t reveal the revenue share division wise (bcf etc.), ebitda margins for each division due to ‘business reasons’. How else is the minority shareholder supposed to understand the prospects of the company?

Present networth is arnd 300 cr. And After further warrant conversion @75/- (if that happens), networth will become ~335cr. Trading at 0.6times BV with promoter holding at 70%, scope to go 72.5%after warrant conversion… ~3.56% additional shares held by related co.?? (MGN).

Disclosure : invested from higher levels

1 Like

Has anyone come across any Red flags about the promoters.

AYM Syntex Ltd

Highlights of Q1 FY19 results

- Financials

o Revenue grew by 13 % to Rs 231 Cr YOY due to increase in volume and rise in exports. Last year was impacted due to strikes and uncertainties over impending GST. Volumes were lower by 1,000 tons compare to march quarter same year

o In terms of tonnage company did about 12,080 tons which is about 7 % increase over Q1 FY18. There is a drop of 7 % compare to last year same quarter which is mainly on domestic volume reductions.

o EBITDA stood at Rs 16.4 Cr , 7% of Revenue from operations as compared to Rs. 15 crores in Q1 FY18 and Rs. 19.0 crores in Q4 FY18. EBITDA is lower Quarter-on-Quarter on account of lower productions and sales as well as rise in the raw material cost and other input cost like dies and power and fuel cost.

o EBITDA per ton was on the lower side this quarter at Rs. 13,538 per ton as compared

to Rs. 14,900 in the previous quarter however it was higher as compared to the last

year same quarter which was at around Rs. 13,200. Absenteeism of the workers and

employees is faced normally during this part of the year which impacts utilization as

well as efficiencies at the plant level resulting in lower production and also increase

in employee cost on account of overtime being granted to the employees and

workers and some contract labours hiring to manage the production although with

the lower productivity.

o PAT stood at 32 lakh compare to 69 lakh in the previous year same quarter on account of higher depreciations and interest expenses due to increase in CAPEX.

o Debt stood at Rs 236 Cr as on June 2018. This has increased by almost Rs. 15 crores in the current quarter on account of withdrawals of loans largely for the project six to fund the continued CAPEX.

o Net debt to EBITDA ratio is at around 4.48%

o Current ratio is at around 1.1%. Total

o Debtors in the books increased compared to March level from Rs. 87 crores to Rs. 91 crores on account of increase in exports. Although debtors above 180 days is almost Rs. 1 crore only.

o On CAPEX company had total spend almost Rs. 53 crores as on 30 June and around Rs. 48 crores out of Rs. 119 crores in project six. In current quarter company had spend almost Rs 31 Cr on account of CAPEX. - Key Highlights

o Textile

Margin pressure continued while the business continues to suffer there has been some good news after a long time on the demand side. Government has decided to allow input tax credit on fabrics which should increase liquidity in the market.

Further, duty has been increased on certain end products which should hopefully curb imports to a certain extent.

Depreciating rupee has lead to increase in RM cost and it is becoming difficult to pass this on in the textile space

Company has also face internal issues of higher downgrades and wastages and leftovers due to the quality requirement being higher of new strategic customers

Company is also working on developing new source of raw material as well as bring down utility costs which have gone up in the last few quarters.

Palghar Business

• During the quarter company had lost lot of productivity not only on account of the holiday season and manpower shortages but also because of some raw material shortages. This is because one of company major supplier has financial problems and had to abruptly suspend supply for more than a month. This created a major disruption and also there was an inordinate amount of power drippings in the month of June and also in July.

• Company is still in process in developing new supplies and while partial supplies have started from new supplies company expect normalcy to be restored only in September. Business development here is encouraging and some of company new customers have started contributing 5-10 % in total business. These customers are added in Palghar and this number will go up slowly.

o BCF Business

Company is preparing for upcoming expansions which should hopefully start paying fruit from Q4 FY 19 or Q1 of FY 20, although, it will start may be in Q3 but before company stabilize and start running the lines the full impact should be seen may be in part of Q4 FY 19 or early Q1 of FY 20. Company product Sorenyl as well as Comfeel seems to have generated good interest in the market and particularly after the consolidation that has happened in the global BCF supply and sales in these products has started to increase. Company have received the first bulk order for BCF in Comfeel which is a proprietary product for company.

Company order position has also increased which is a great thing now that company new capacity is coming up. And on this side the Rupee-Dollar increase will help to partially offset the cost increase. Company is now near the end of CAPEX cycle and company will be done at the end of the Q3 after which company will try to consolidate its operations , focus on cost and getting the utilization numbers up and also of course improving the quality of the balance sheet.

Q&A - In terms of EBITDA margin in last 12 years only 3 years company have posted EBITDA margins over 10 %. and for minority shareholder’s it does not help like if the share price drops to 75%, say from Rs. 150 to Rs. 40 now . So whether one should considered it a commodity company or a specialized yarn company ?

o In terms of product mix company margins are much higher than competitors Company is a specialty yarn manufacturing company operating in a very niche segment or several niche segments. Company also have commodity side of business also as the Nylon business which is a significant part of overall turnover is certainly a commodity segment but at the same time one can say it is a mix of both. - What will be the depreciation cost going forward as company will be finishing CAPEX in Q3 ?

o Currently it is 8.7 Cr and after CAPEX it will be 9.5 Cr per quarter. - Did company have warrants to convert ?

o Yes company have it around 30-35 Cr and company will convert it very soon. - Did MGN Agro the shareholder of the company is related to promoter group ?

o They were partner of previous share holder of Welspun Group and now they fall under public shareholders. - When will the margin improvement can be seen ?

o Company have 3-4 levers that will push the margin like

Increase in the volumes of the business in Palghar in textiles as well as the upcoming BCF expansion

Cost reduction initiatives that will occur in next few months

Up-gradation of production mix that will be more focused to move from commodity business to specialized business.

o Company is in middle of all these steps that was started 2 years back - What is company outlook on raw material and how percentage of sales it will consolidate ?

o 60 % of sales are raw material. In short term there can be a supply shortages of PTA as a result of which company is expecting polyester raw material prices to go up. Nylon however has been stable for the last month or month-and-a-half but very difficult to say what is going to happen in the future. Certainly Caprolactam which is an input for Nylon is right now not available very freely. - Does the lower margin are driven by the textile segment as opposed to BCF and Palghar ?

o To a certain extent yes. Company textile segment which is the Polyester and

o Nylon segment has actually led to majority of the compression in margins that can be seen in last 2 years. More or less the Palghar margins and BCF margins have

o remained intact or in certain months even gone up but it is the textile segment where the performance has dropped in margins. - Why company is not able to pass the raw material prices to customers ?

o In Textile segment in Palghar as well as BCF company have slightly better pricing power and to a certain extent and company have been pass on. On average company may be able to pass on but company have certain customers on which it is unable to pass on. In textiles in case of Nylon in 2016 where raw material price was $1,600 and today the raw material price is around $2,475. In Polyester the raw material price at the base was around Rs. 55 and it has now increased to around Rs. 85 approximately. In Nylon the company was unable to pass on the entire cost because of mismatch of demand and supply scenario in last two years. Not only have the margin of raw material because of the demand supply gap reduced even at constant raw material prices but the increase of raw material prices has further shrunken the margins. Majority of compression come from Nylon. - Is there is some news about reduction in the XT power cost for XT spinners in the state of Maharashtra, is that something that company is picking up on as well and that should materially help company ?

o Yes , talks are going on and if that comes then it is a big bonus for the company but let it first come. - Kindly give some update on strategic customer front ?

o There is no significant addition of commercial business in new customers which are already announced in some of my previous quarters but certainly with the existing customers particularly in Palghar the volumes have ramped up. In BCF also the SORENYL and COMFEEL products, COMFEEL is proprietary and SORENYL is the solution dyed Nylon product which company developed sometimes back and the volumes over there also have significantly ramped up. On the textile side, the

strategic customers that company added they continue as per normal. - In textiles how volume growth will take play ?

o The efficiency and utilizations at which company is running the plant there is a lot of scope to actually improve upon those numbers and that extra additional tonnage gives company disproportionate profitability because the entire contribution comes to the bottom line. So in textiles company is not adding any new lines but through the process of better utilization of existing lines and better efficiencies company is hoping that over a period of time company can add some volumes.

o In Palghar it is the debottlenecking process. Company have various routes in which company do the dying , there are 4 or 5 different routes in which the input raw material is being fed into the dying process. Company must find the right balance, sometimes three routes might have excess orders and two routes might have low orders. So that causes bottleneck in the plant and the dying department is not fully fed with the material.

o In Palghar if company become unable to balance out the routes, there are plenty of scope for actually increasing the volumes. And again with Palghar company can get additional profitability if company able to increase the profitability. So again that is a better utilization and efficiency and balancing that company can do. in Palghar and in BCF of course the extra capacity which is coming. - What about turkey situation after the political issue in BCF business now in any way positively or negatively because the currency there has depreciated a lot ? Does it make company less competitive and its impact ?

o Certainly some of the local Turkish players are going to be more competitive than

o before. The impact will be seen in the quarters coming forward. Right now company have not heard anything from customers but company have to be very watchful on this and see how to proceed. But it is not like company have unlimited barrier to entry but still it is not a one-minute exercise like maybe in the domestic Nylon that maybe for Rs. 3 or Rs. 4 the sources get changed.

o In terms of BCF it is a slightly more strategic relationship with the customers Company is working very intimately with these customers and particularly with the new products that company is offering and the share of the new products SORENYL as well as COMFEEL is increasing, and these are products that for company at least company gave a chance particularly in solution dyed Nylon after 4-5 years. - What was the consolidation happen in BCF market ? What is the market share of company in BCF segment ?

o Market share is very tiny . The consolidation is basically one of the leading players of BCF called AquaFil, they purchased a plant in China of a company called INVISTA and these are the two. So they did not purchase INVISTA, but they purchased a plant of INVISTA, but they were one of the leading suppliers of solution dyed Nylon and that has opened up some doors for company. AquaFil and INVISTA were suppliers - Will the utilisation will be at peak after adding new capacity ?

o No , existing capacity will be utilised fully but the new capacity will not be fully utilized immediately. But over a period of time it will get utilized. To a certain

extent the new business has been lined up but also the new expansion in which out of 100 tons capacity 50 tons are lined up with the customer.

o Company have to start with zero for new development it cannot start in existing line and after that long process will happen that which has happened for all other products. But rest of the 50% capacity that will also get utilised in a quarter or two. - What is the cost of debt ?

o 9 %- 9.5 %. - What is the plan for Debt repayment ?

o By Q3 end all CAPEX will be completed and after that company have no CAPEX plan so whatever Cash profit company will generate will directly go for improving the Balance sheet. Company target is to keep EBITDA ratio between 2-2.5 % which is 4 % currently. - What are the current reserves ?

o 230-240 Cr - How company will deploy Reserves ?

o It is combination of the retained earnings and the capital reserves and securities premium reserve which company have. The cash flow that company have is already get deployed in the investment and expansion. - What is company planning for commodity business ?

o Company will not invest any capital in this business. It will become smaller and smaller part of overall business. Over some period of time the commodity business will keep moving down. The product mix and new capacity which will be added will only be in strategic area only. - In what direction the company is running ?

o It is running in a direction like

Company is a specialty manufacturing company and looking to add volumes of specialty products.

The operating leverage of the business is higher as compared to some of other competitor businesses and that’s why when new product gets added to the portfolio of the company, the profit of the company should hopefully disproportionately improve.

o So that is the strategy and that is the plan. - What is the company current utilisation as a whole ?

o At a company level the overall OEE this is a function of both utilization as well as the

efficiency is around 71%. - Will be there any cycle shift in coming future in Nylon ?

o No because anti-dumping duty on Nylon was removed. So as soon as the capacity in India starts to get limited then some imports from China and Taiwan can be seen. - What was the split between import and export revenue ?

o Export was 36 % of total revenue compare to 32 % in March 2018. It will gradually increase. - But still company have 65 % market as domestic ?

o Yes - Does company is looking toward new countries to market the products ?

o Yes it will evolve in certain type but company is a customer specific player.

5 Likes

India imposes anti-dumping duty for 5 years on nylon filament yarn import from Vietnam, EU

Very Positive for AYM Syntex

2 Likes