Axiscades is a company which focuses on the engineering, particularly the aerospace and defence space, which is something similar to Dynamic Technology. Recently they got some orders from Indian Airforce too on some simulation technology

Management- New Management took over from Feb 2014. I worked in INFY and found one veteran former ex infocion is CEO now. But I don’;t know him. In the BOD also, I see Srinath Batni who was an INFY veteran is there. Mr.Batni worked in INFY since 1992 Axiscades.docx (48.9 KB)

and was in INFY Board also

I see for the last 2 years significant improvement in top line and also they opened one ODC for Siemens wind turbine also in HYD.

Threat : Well entrenched competitors but market is really big. Potential is great in the event of Make In India and they have already got the approvals from the defence forces

Already supplier of Airbus

they have already got the approvals from the defence forces. Sharing some key operational parameters relevant to IT , that indicates, numbers are improving and company is focusing on execution

I am not a financial wizard, but so unable to share too many numbers

Also I saw some of the Big Guns have also taken position but unable to make out whether they reduced the position from 2015 to 2016 or not…I saw their names in AR2015

I saw Glassdoor feedback of employees , although it is very small but it is pretty bad.

i would not pay too much heed to glassdoor reviews as they tend to be biased. Only disgruntled employees would need a platform to vent their ire. Very rare for a top-performing employee to take the time out and review his employer. For he wont have time off from work!

Axiscades seems a good bet , looking at glassdoors is certainly incorrect , I missed canfin home which multiplied 6 times , I discussed with canfin home employees which are always dis satisfied .

Result on 10th august. Revenue growth is a key monitorable. At such a low base, 2-3% sequential growth doesnt quite justify a 20 pe. Mgmt had guided for closure of merger with axiscades aerospace by july end. That hasnt happened. Merger when it happens is not expected to be dilutive so thats something to look forward to.

Stock’s getting nervous before the results. Company bills 90% of its revenues in $. So pound £ depreciation shdnt impact much.

Would be glad to hear anyone with interesting insights on this one.

Defence orders are yet to kick in which might take sometime, hence I believe this stock will test patience of the investors. However the growth of the company in the last 3-4 years did make take note of this company. It’s too early to tell if it will continue to show the same growth but I felt it worth allocating a small pie to it in the portfolio. 200-210 seems to be a decent entry level.

However since the company is too small, its a high risk high reward stock. Have invested 2.5% of my portfolio in it and do not plan to increase it further. Seems to be consolidating between 200-265 levels.

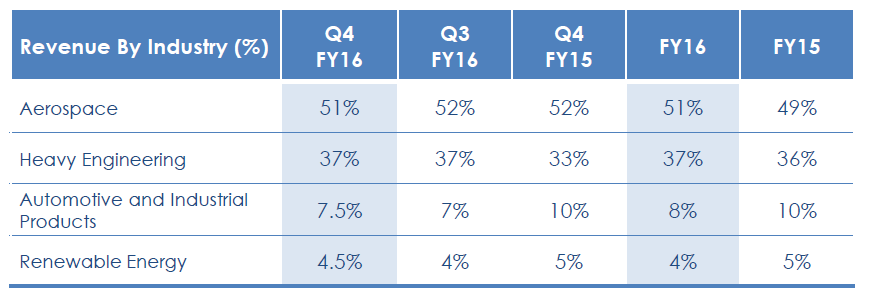

For Q4FY16, AXISCADES’s revenue growth remained flat at $14.7 million on sequential basis. In rupee terms, revenues for the quarter was at Rs99.0 crore, registered a growth of 2.5% QoQ and 19% YoY; EBITDA margins declined by 23bps qoq to 14.5% due to increase in sales and marketing expenses, while adjusted net income was marginally up by 2%QoQ to Rs7.6 crore on the back of higher other income (up 243% QoQ).

On operating front, Aerospace contributes 51% of the total revenue, while the other verticals such as Heavy engineering, Automotive and Renewable Energy contribute 37%, 7.5% and 4.5% of the total revenue respectively.

Fixed price contact increased to 36% in FY16 compared to 28% in FY15. Top 10 client contributes 92% of the total revenue.

Added one large OEM client in Aerospace space from Europe in Q4FY16, while added 19 clients in FY16. Total headcount stood at 1,700 as of March 31, 2016.

The management guided that the aerospace vertical is likely to growth above the industry growth rate in FY17, on the back of healthy order book (60-65% revenues visibility) and robust deal pipeline.

Expect margins will be in the range of 17-18% in coming years. Further, the company anticipates the utilization rate will move up to 75%

Agree with you totally. Another point is employees are too deep drenched in operational aspects of the company that they are not able to see the larger picture which we as equity investor try to do. They generally tend to give views in a very very precise manner and there will always be some issues in every company. Markets have certain tolerance level for every company.

Well, its quoting at a earnings multiple of 32 and barely covering its cost of capital. Essentially, the growth prospects seem to be baked into its price. I would certainly wait till it reaches a level which offers a margin of safety

Indian aviation in turn holds AXISCADES Aerospace & Technologies Private Limited (“ACATL”), which has now become a 100% subsidiary of the listed company.

I had downloaded the MCA documents of India Aviation and Training, and looks like in FY 16 India Aviation infused capital into the above mentioned firm from capital they received. ACATL has a PAT of 10 odd crores.

There seems to be some value (not no value), even then for an investment of Rs 10 crores into ACATL as per FY 16, India Aviation got a valuation of ~ 170 crores when ~1 crore shares were issued to Promoters on Dec 30 2016 and the price was about Rs 170 per share.

I am withdrawing the above post and thanks once again! Attached is the FY 16 consolidated statement of Indian Aviation, that shows a PAT loss of Rs 1.59 crores and PBT of Rs 4.75 crores.

Majority stake in the Company is owned by Jupiter Capital Pvt Ltd - a Venture Capital Company run by BJP MP - Rajeev Chandrashekhar. Jupiter Capital also owns large stakes in Media Companies - AsiaNet and Republic.

In 2019 the Chairman for last 5 years- Dr Vivek Mansingh left the Company, Independent Director - Mr Srinath Batni and CFO - Kaushik Sarkar - left the Company ar around the same time.New Chairman appointed is David Bradley who was formerly working in Assystem (Axiscade has a JV with Assystem)

During FY 2018-19 - Axiscade invested ~ INR 2 Cr in Equity Shares of Astra Microwave and ~ INR 3 Cr in a ‘Real Estate Fund’. Same can be seen in their Balance Sheet.

Debtors are quite high at around 1/4th of Annual Revenue. Ageing also shows significant amounts in past due category.

The Company acquired Mistral - a Defence electronics company for INR 175-200 Crores in 2017. The purchase consideation was linked to Revenues and profitability of Mistral and as on 31.3.19 - There is a huge liability of ~ INR 200 Crores. To put that into perspective - Market cap of Axiscades is around ~ INR 230 crores. Post acquisition - Mistral has to generate enough free cash flows to enable Axiscades to payoff this liability. Mistral’s Cash profit (PAT + Depreciation) for FY19 was ~ INR 19 crores.

Acquisition related liabilities are not accounted as cost in the P&L, and hence without factoring them the profits can appear to show very high growth.

Disc - No investments. Just did a bit of preliminary research, hence shared. Management seems to be a bit aggressive for my liking.

Last 12 days(17th June-20 to 29th June-20) the stock has been rising very rapidly. Hitting upper circuit almost everyday. And a 200x jump in bids. Anyway, this news came in today:

Whats to be liked: Axiscades debt is reducing. Q4 Loss was notional. A significant amount of goodwill impairment has been catered for which came from Mistral acquisition. Cash on book higher than debt. Decades in Engineering business and trades at high discount to peers in terms price / revenue.

Topics of concern: Low engagement with investor community, ongoing litigation with Mistral and high exposure to Aerospace which has fully not recovered