I can think of three sections of retail in India - Unorganised, Organised, Online.

Unorganised retail has market share of 85% , which it is slowly losing to organised sector.

Organised players have almost 15%, which we are considering being under threat from online players. Even if organised offline shops loose some of their market share to online players, they still have tremendous potential of gaining market share from unorganised players.

Ten years back, I used to see a number of grocery shops in any nukkad of a city. Nowadays, only one or two of them are seen operating. If we observe our own grocery shopping patterns in cities, we either buy groceries weekly-fortnightly from BigBazaar or Dmart, or buy them online. Only time we buy them from next door grocery shop is when we need to buy something smaller on urgent basis. (I am referring to general buying pattern, may vary person-to-person) This indicates at value migration in retail space.

Also, demonetisation had forced more people shifting to plastic money or mobile wallets, hence many organised players didn’t face big revenue loss during Dec quarter and same may be expected to continue.

I have also heard that GST will positively impact organised players (I dont know how - If anyone knows how, please shed some light on this)

Yes, post listing!

D’Mart is a great business backed by great operations numbers. However, am not a great fan of shopping in D’Mart. Most of its stores in Mumbai are very small compared to Hypercity/Bigbazaar and many others, due to which it gets super over crowded and looks like a fish market during the latter half of the day.

I doubt the number can improve greatly from hereon, however the players have big scope of improving hereon not to forget new competitors. The current valuations according to me seems to be on a crazy premium side which is more liquidity driven.

I will look to enter only if the stock is available at 400-450. There are many other business which gives more value comfort at current levels.

One of the big advantages of dmart is the capital turns which are best in the industry. Many food brands like chheda and balaji wafers have been built solely because of their association with dmart. Dmart offers them a chance to go national and compete with the bigger players. Also to my mind dmart is the only place which gives a flat 50% off if you are not interested in a buy 1 get 1 offer. I havent seen any retailer do that. These are the small things that set it apart from others which i value.

It’s a very good company available at exorbitant price fueled by over liquidity in this bull market. I like their operational excellence and best in sector numbers, but still, i won;t be a buyer at these valuations. People are buying, but in my opinion they are neglecting the risks involved (likely) or are completely unaware (unlikely).

I have no opinion about the valuations currently. If the company continues to post the growth numbers that it has in the past then one may look at the valuations differently. It all depends upon your views about growth rates. I doubt whether a b2c business like dmart will ever be cheap according to value investing yardsticks bull market or bear market

ndians like the fish mkt cocept ,more crowded the place more people come in.

I think Indians like value for money and don’t mind going to a fish market for that.

Isn’t that the same reason why D’Mart has it’s strong customer base in their outlets as well.

Amazon Pantry and BigBasket are getting popular day by day… When Amazon Pantry is running weekend offers like Rs.500 off on Rs.2000 purchase on already discounted items, you can’t beat it.

I see lots of deliveries by Amazon Pantry and Big Basket in weekends in my apartment.

These will give D-Mart like companies a run for their money.

Disclosure: Got 1 lot in IPO. Sold it on listing day.

Amazon Pantry, BigBasket and others serve a target group that is distinctly different from that served by Dmart both in demographics and psychographics. People who shop at Dmart dont shop at Bigbasket and people who shop at Bigbasket wont enter Dmart. There is a distinct laxman rekha between both these consumer groups with little overlap. Unfortunately for online retailers, the size of the Dmart kind of customer is massive in relation to the Bigbasket customer which is a tiny speck. Online grocery shopping will certainly grow but it will always be a speck compared to the heavy lifters like Dmart.

Agree on Bigbasket point. The products are mostly international and premium. The customers I see in Bangalore are former NRIs or expats and international cooking enthusiasts. The stores are in high profile locations and very well kept. Surely, they are not competing with a big Bazar or Dmart. As @bheeshma correctly mentioned, BB will remain pretty small as compared to other stores discussed here.

Couple of things :–

- Online Food Retailer’s are still at the nascent phase and yet to have a pan Indian presence. So it will take them much more time to become a pan Indian player.

- Consumer Staple products is something for which people do not like any delivery lead time which the online retailer will always have.

- It is also will be a big issue for them that how long will they be able to hold onto their discounted cheap price since logistic cost will be a big item for them on which D Mart is having the advantage of EDLC/EDLP due to their Asset Ownership model.

- It is also debatable that how many of the online customer will buy a grocery items since everyday product deal is not fashion deal type that will interest buyer.

- D-Mart also exploring their online option in their operating Cluster so they are also visionary about the risk they are facing and on the right path to de-risking it.

Having said all the points I still think the share is overvalued and should be bought at 450-500 level.

Discloser Invested at 565 level and holding for long term will add more if the price correct.

It has gone up 11% today even when the market is 1% down. Any idea who is buying ? this move can not be made by the normal retail investors in one day.

Recent Research reports for Avenue Super-mart have target price below 700 only.

Now stock is trading at its own valuations.![]()

This report by JP Morgan says Neutral stance with Target of 635.

Dmart JPMorgan.pdf (1.2 MB)

Research report by PL

http://www.plindia.com/SampleReports/AvenueSupermarts-21-3-18-PL.pdf

Given low float (10%) ( Promoter ~82% n Institutional ~7-8% ) this frenzy may continue for a while.

Disc- Invested on listing day

If that has been the story Rakesh it seems I only have kept myself happy with the holding of mine on listing day @565 . Not sure if I will get any chance to buy it again below that level …

D-Mart Still Fairly Valued From FY19 Perspective: Basant Maheswari

Disc: Not invested but waiting for correction to enter

Basant Maheshwari On The Extraordinary Growth Rally Of Indian Equity Market

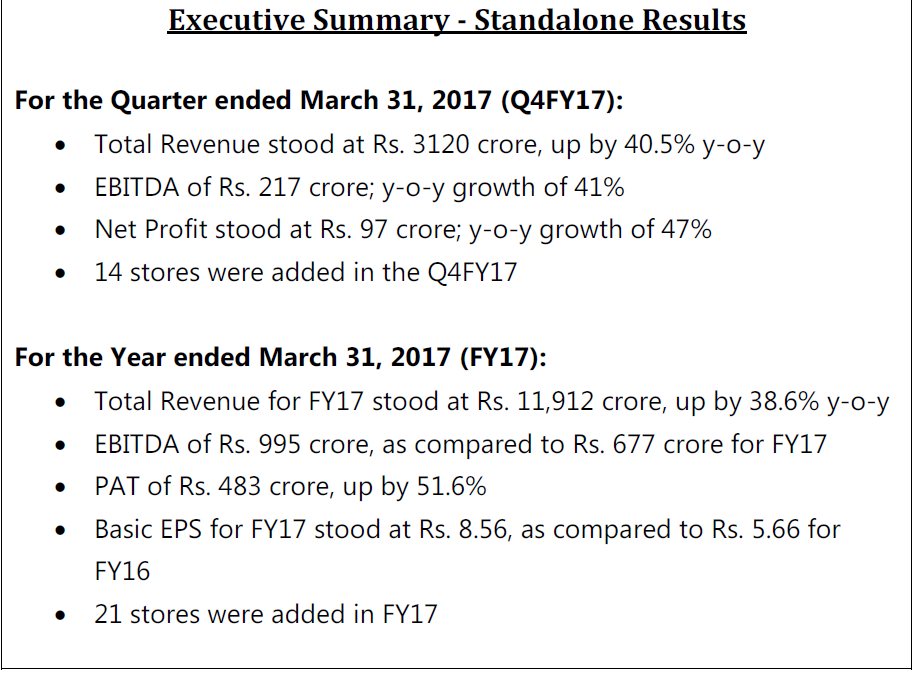

Q4 results and presentation

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/636c913b-2103-47d6-bb4a-880ef949b2a8.pdf