BM disclosed it long back on TV. One of his First Day First Show that is around 600-650

A couple of days back a tweet was shared by a fellow member in which a fair comparison was made between the product prices at DMart and Future Retail.

Today, I had visited Food Bazaar and I’ve tried to collate information pertaining to the prices of essentials.

Tata Salt(1 kg):

DMart: Rs 16

Food Bazaar: Rs 16

Amul Butter( 500 grams):

DMart: Rs 209

Food Bazaar: 212

Chana Dal:

DMart: Rs 33.5 ( 500 grams)~ Rs 67( 1 kg)

Food Bazaar: Rs 50( 500 grams)~ Rs 100( 1kg)

Kabuli Chana( 1kg)

DMart: Rs 123.5

Food Bazaar: Rs 124

Moong whole(1 kg):

DMart: Rs 100.5

Food Bazaar: Rs 88

Chowli( 500 grams):

DMart: Rs 62.5

Food Bazaar: Rs 82

Matki( 500 grams):

DMart: Rs 31.5

Food Bazaar: Rs 38.5

Pulav Rice:

DMart: Rs 59

Food Bazaar: Rs 76.5

Sagar Ghee:

DMart: Rs 2149( 5 liters)

Food Bazaar: Rs 237( 0.5 liter)

Toor Dal(1 kg):

DMart: Rs 75

Food Bazaar: Rs 85

Rajma(500 grams):

DMart: Rs 45.5

Food Bazaar: Rs 74.5 ( The significant price differential can possibly be attributed to the bigger size of a Rajma bean at Food Bazaar)

I understand that this isn’t a comprehensive list. But, I’ve tried my best to expand the list presented in the tweet.

Also, as expected, shelf space was dominated by products from their own brands.

I did buy some products for trial.

And, to be fair, their products are genuinely good for the price charged.

For example:

Mixed fruit juice by the brand Tasty Treat is being offered at Rs 91 for 2 liters. The price being charged is less than half of competing juice producers.

And, it was of decent quality.

However, emergence of their brands has led to a reduced shelf space to products manufactured by other companies.

Nonetheless, it was a decent shopping experience.

11 Likes

No intention to hurt but overconfidence does not pay in the market.To authoritatively confirm DMART will give 15% CAGR is naivety.Spreadsheet calculations does not give too much insight into underlying value. But again different opinions make the market-so no issues

Which is why one should read the comments properly no offence meant. I have clearly written that these assumptions would be true in an ultra optimistic environment.

Yaar it depends if you can live with the ultra steep falls. In case of a hard correction or any unforeseen biz circumstances, the multiple contraction can be immense. It is just that I am becoming a little defensive and I see uncertainty in biz environment.

Nobody is paying 129 PE for 15% growth. The GDP is growing by 8% and adding 6% inflation, 14% is the minimum earnings growth you should expect from any company. BM is certainly not a 15% growth investor and he expects upwards of 30%. Assuming that Dmart grows by 30% (the competition being so stupid) the returns to investors will be far less assuming PE moderation which must definitely happen in a bear market. What competition is now doing is replicating Dmarts prices, without replicating the business model. When you replicate prices alone, while continuing to maintain a high cost operation the folding up date is not far off.

2 Likes

DMart, trading at a PE multiple of 115, seems expensive. But, just because something seems expensive doesn’t necessarily mean it’ll experience a meltdown in prices. I had, in my interaction with a trader learned that shorting a stock just on the basis of high valuation seldom works.

Various other factors need to be taken into consideration.

And, at the end of the day, value is in the eyes of the viewer.

Compared to peers it’s expensive but then what’s the right valuation?

Whatever the buyer is willing to pay and the seller is willing to sell for.

In a bearish market there’s a likelihood that the stock may experience a drawdown.

Or, it may not experience a drawdown.

Who knows? Noone

Some stocks, in the FMCG sector have always traded at high double digit PEs.

But, have been successful in generating wealth for their investors.

This isn’t to say DMart will necessarily be a wealth generator- I don’t know anything at all.

But, just highlighting some cases where despite perceived over valuation returns were decent.

And, there are several cases where over valuation resulted in wealth destruction.

Markets, resultant of the emotions and cognitions, of millions of participants are often difficult to comprehend.

I haven’t been able to understand it yet.

Hopefully someday I will.

Seems you have not read BMs magnum opus “The thoughtful investor”. He says that all stocks however great sell at reasonable PE in a bear market. In my personal experience

I have not seen anything sell above 60 pe in a recent bear market. BM says 20 pe, in a severe one. Let us see.

Time to buy Dmart- During bear market.

Reasonable price- Bear market price could be between 60 pe to 20 pe.

2 Likes

Exactly my Point. Mr. Biyani is spending crores advertising Har Din low Price during IPL prime slots without worrying about the cost structure they operate in. Whereas D Mart is spending zilch on ads and the money is used to improve the supply chain.

Case in point: A good Mgmt always delivers profits in all situations and hence markets love them and reward them with astronomical valuations.

3 Likes

@Julian Can you elaborate on how you came to these conclusions? As I understand

Free cash flow (FCF) = Operating cash flow - capital expenditure

So if DMart is FCF negative then it implies it is spending more on CAPEX, maybe opening more stores, purchasing land, investing in associate companies etc. Why is that a bad thing for DMart? I am not trying to dispute the fact. I just want to be convinced of why this is a bad thing, before I make an investment decision.

According to screener/DMART, avg RoE for the last 3 years is about 20%, RoCE is 22%. Aren’t these good numbers?

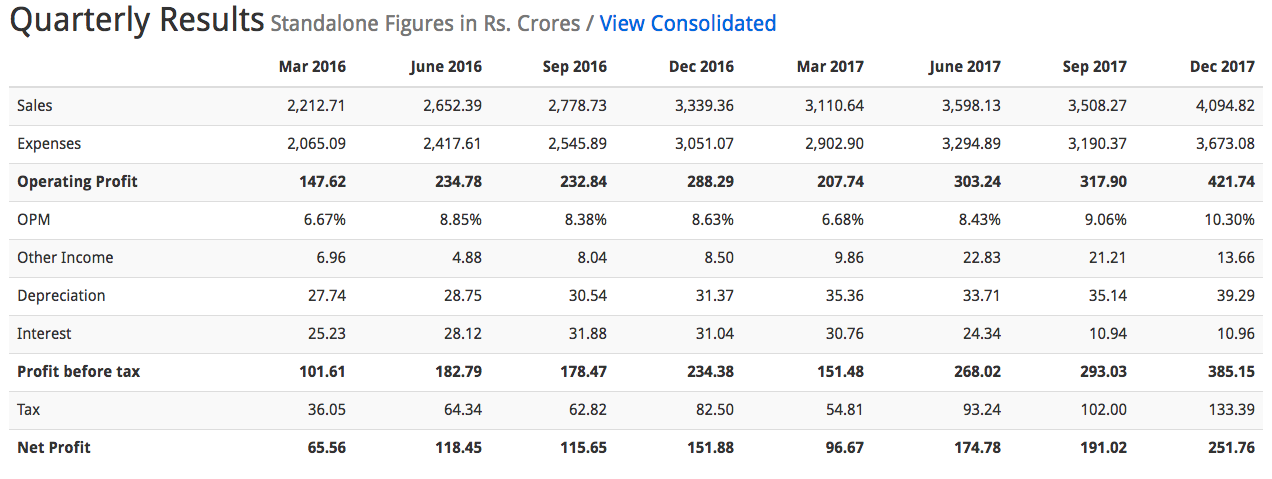

Everyone,

How do you explain the fact that, in terms of profit & revenue, Jun & Dec quarters are better than Mar and Sep quarters? ![]() Or in other words Sep is worse than Jun and Mar is worse than Dec.

Or in other words Sep is worse than Jun and Mar is worse than Dec.

Disc: Just started analyzing this company. No investments yet.

2 Likes

Free cash flow was calculated by deducting cash from investment from the cash from operations in screener. This was found to be negative. If depreciation is assumed as the maintenance CapEx, and if only this figure is deducted from CFO, company could be cash flow positive to the tune of 320 crores for which you are paying 91000 crores in market cap ie., 286 times. However on an overall basis business is sucking up cash as it is in an expansion mode. There is nothing wrong in being cash flow negative as long as the business ends up cash flow positive in future. Many businesses don’t.

Roe for 2017 is around 12.5% . However ROE for the previous years is as per the figures furnished by you and you may go by the same. Business is good. Long term prospects are good. But asking price is unreasonable.

2 Likes

Thanks! That was really helpful

Any guesses about the 2nd question? About the variation in quarterly performance? Since DMart is a retailer selling items of daily needs, IMO the revenues & performance should not be cyclical.

Putting it other way, December is higher than other months because Diwali falls in Oct-Nov every year which will definitely boost Dec Qtr revenues for every retailer.

No idea regd Sep/Jun Qtr, however the chart shows it wasnt the case in 2016, so its just a one-off may be.

KSA Technopak’s views on ASL from 7 min onward.

1 Like

Love you KB. Customers are being asked to give way and side for paid brand ambassadors. Kaam itni khamoshi se karo ke kamyabi shor macha de…

2 Likes

DMart will be punched hard during a down market. Most newbies will learn this lesson the hard way in this bull market. Valuations will always win!

4 Likes

I don’t mean any disrespect to celebrities. But, I truly wonder whether hiring celebrities as brand ambassadors has any influence on sales or not. Buyers’ decision, more often than not, is based on their views of the product/ service and not on the basis of brand endorser. If companies stop spending so much on star campaigners it’d be interesting to see the effect on the popularity among buyers.

3 Likes

It seems cheaper than loss making flipkart , which is valued at $20B - DMart is $14B right now. I plan to sell Dmart at a $140B valuation some day…may be in the next 10-15 years, and I am ok with that kind of return. Seems too far fetched right now, but the big banks like HDFC bank will command a market cap of $200-250B by then. If you are a value investor , you may find it hard to digest growth investing - and its vice versa for growth investors. Not much to debate, and to each his own way of making money.

Invested

4 Likes

hmnnn. Did we not say the same thing about Page and Gruh in 2015?