DMART presents a good growth stock and the valuation will not fall until the growth falls. It may give a higher CAGR during the high growth period. Any stock has one or the other risk, and many good stocks with high valuation carry risk of growth slowing down. I have been a growth investor and I have diversified across many overvalued stocks - and the ones where the growth thesis was correct took care of portfolio. So yes DMART is overvalued and diversification may help.

1 Like

Message from my brother after visiting the only Dmart store in Chennai.

"I visited Dmart this saturday. It is inside a not so popular mall which also hosts a multiplex.

When I went inside my first impression was a ‘Wow’ on seeing the prices. It was the lowest price seen for many items. Slowly the excitement faded away due the following reasons

- Not much to choose from, no alternatives. They dont have all the products that every supermarket has. Also the size options for each product is limited. I think they are stocking only items for which they are able to provide huge discounts

- Overall ambience and atmosphere of the shop was dull

- 2nd and 3rd floor comprised of bags, shoes, other items which seems to have only minimum takers. The quality being nothing to talk about.Overall these floors looked like they were ready to be closed/aborted soon."

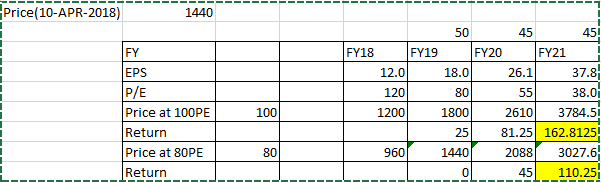

Just to give another way of looking at this quality compounder…

If we dont look 10 year forward and instead look 3 year forward…then can we see good returns…

Assuming this being a quality compounder and next 3 years it will compound its earnings by 45-50%, below is a chart showing the kind of returns at different forward PE’s.

So i have taken two scenarios

Scenario 1 : Markets assign a 100 PE in FY21 to DMART: At this rate we can see in the above chart the stock will give a return well above 25% CAGR next 3 years

Scenario 2: Markets assign a 80 PE in FY21 to DMART: At this rate we can see in the above chart the stock will give a return of 25% CAGR next 3 years

So if we look at a 3 year view , it presents a decent compounder…as long as it can keep growing its earnings at this rate…the share price will follow the same…So despite PE shrinking, the EPS growth will ensure the stock price keeps giving a decent return…

Disc : Invested and holding. Views maybe biased. Please do your own research

3 Likes

In my opinion, it’d be unreasonable to expect decent returns in the next 3 years.

2018:

Sales- 13000 crores

Net profit: 710 crores

2021:

Let’s assume the best case scenario that the company grows sales at 40% CAGR.

Sales- 36000 crores

Net profit: 1960 crores

This is the best case scenario.

And, it’d be imprudent to expect DMart to be able to sustain valuations of 6-7 times sales.

Let’s assume a little moderation and regression.

I’m assuming valuation of 4.5 times sales

Market capitalisation: 162000 crores

CAGR- 21.5%

And frankly, 4.5 times sales is unheard of.

Hardly any retailer trades at these valuations.

This seems to be the cap to me.

If anything, valuation will possibly l be lower than this.

But then, anything is possible.

Markets are known to present surprises.

1 Like

Thanks for sharing. V interesting. I liked the comments of people to this tweet which reflects a lot about the genuineness of this comparison.

1 Like

1 Like

In one way, Basant Maheshwari is right. By the time several folks have been creating models and calculating ratios to nth level, some have made 150% profits in a year. That too, with reasonable confidence and peaceful sleep.

Discl : Invested from first day, high allocation.

3 Likes

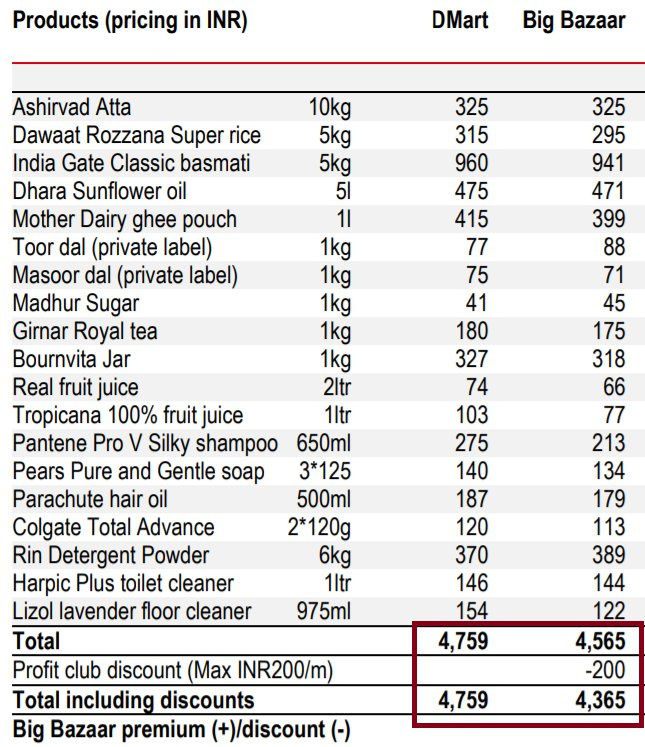

It could also mean that Big Bazaar margins may finally be a little lower.

Dear @Yatharth Sir,

In public fora DMart is often showered with superlatives and bestowed with an exalted ranking. I too firmly believe that Dmart is performing exceedingly well as an enterprise - Expanding rapidly, increasing market share and occupying precious mind share of customers.

But, I sometimes wonder if the high praise for DMart is related to the favourable price action.

Had the same stock been a bad performer would its description be different?

And, I must express my admiration for your posts. Your conviction and patience is what I as an amateur want to imbibe. Thanks again.

2 Likes

Thanks.

Made several mistakes like selling Page and Gruh in the last one year. Learning lessons. Very few companies in India can give 20%+ profit growth consistently, have good management, and allow you to sleep peacefully.

My confidence has nothing to do with the price action. Even if price has remained @10-15% cagr with good sales/opm expansion, I would have been content. As long as there is 20% growth, I may remain invested. All this talk of PE derating is hogwash as long as revenue/eps keeps on going at 20%+ rate.

Now I think that if a good company goes down for a quarter or two, one should remain patient.

4 Likes

Exited DMART today 1485 levels and 130 PE. Will add once there if there is a time correction or will add HDFC Bank if it goes to 1800. I think DMART will give max 15% CAGR for next 10 years if we are ultra optimistic.

Here are simple calculations

FY18E EPS - 13

FY28 EPS - 180 (assuming 30% CAGR)

Exit PE - 40

Price = 7200

CMP = 1480

10yr CGR for 7200 = 17%

I am not a strict a value investor but this is too high a premium for ultra optimistic target. The fun part is that if the CMP changes to 1300 after a year and EPS increases by 30%, the entry would become quite better.

I see HDFC Bank giving that 15-17% returns for next 10 years and that too without much sleepless nights.

13 Likes

In the next week I will check out the prices in both the stores. I have been purchasing from both stores since I got my discount card. Let me see. I will try to expand this list.

1 Like

BM and his PMS put together may not even be .1% of Market cap of DMart. So hyping will not work to manipulate the price. However, he can sing this as a success story to attract clients to his PMS. Notice the difference please.

Like this line of thinking. But if I can

- Get 8-10 such companies, that will grow at 15%+ for 10 years, and

- I keep my bias away and invest in those,

then I need not watch twitter/Valuepickr/Portfolio for more than once a year or quarter. Life will be jingalala.

1 Like

There are a lot of top grade investors on Twitter. No doubt.

But, discussing stock picks on social networking sites where they have a substantial following is, in my opinion, inappropriate. Their entry point was at a much lower price.Those who enter now seeing their tweets have a much lower margin of safety.

They are responsible for their beliefs in stocks when they perpetuate it on social media.

And, anyone reading this thread, my humble request that please don’t invest just on the basis of stock ideas being trumpeted by these famous investors. They’re quick footed and won’t inform the masses when they exit. Invest based on your conviction.

4 Likes

After seeing BM’s tweet in twitter and disclosing he owns it, i wonder if he is planning to sell it soon looks like he is trying to pull his followers also into dmart