Good find, the link below gives the revenue figures which were missing in your link

2 million tonnes in volumes & 2.1 Billion Eur revenues with 134 mil net in 2014

The world feed market is an oyster for Avanti to find !!

Good find, the link below gives the revenue figures which were missing in your link

2 million tonnes in volumes & 2.1 Billion Eur revenues with 134 mil net in 2014

The world feed market is an oyster for Avanti to find !!

Nutreco 2015 AR mentioned this

’ Most of the world’s shrimp feed is produced in China, Thailand,

Ecuador, India, Indonesia and Vietnam. The global market

has a long-term growth rate of approximately 5% per year

and was around 3.3 million tonnes in 2014, an increase of just

over 5% from 2013. This is a cautious recovery from the low of

2012 due to the impact of acute hepatopancreatic necrosis

syndrome (also known as early mortality syndrome, EMS),

a bacteria that causes shrimp mortality. The top five shrimp

feed producers apart from Skretting are Charoen Pokphand

Foods (CPF), Guangdong Evergreen Group, Guangdong Haid

Group and Guangdong Yuehai Feed Group, and together

account for approximately 40% of the global shrimp feed

market. CPF is by far the largest shrimp feed producer with the

next four companies fairly close together in market shares.

It has remained challenging for Thai, Chinese, Malaysian and

Vietnamese shrimp feed producers due to the continued

presence of EMS in those countries. Production has decreased

by 25% in the last four years and has resulted in high global

shrimp prices. It is expected that those countries will recover

to pre-EMS production levels in the coming years, meaning

countries such as Ecuador that did not suffer from EMS may

still have an advantage in the world markets for some time"

Total Shrimp Feed market conservatively will be around then 3.7 Million Tonnes now.

Avanti’s current capacity is rough cut .415 MTPA and that is cut rough cut .11% of world market share

Hello

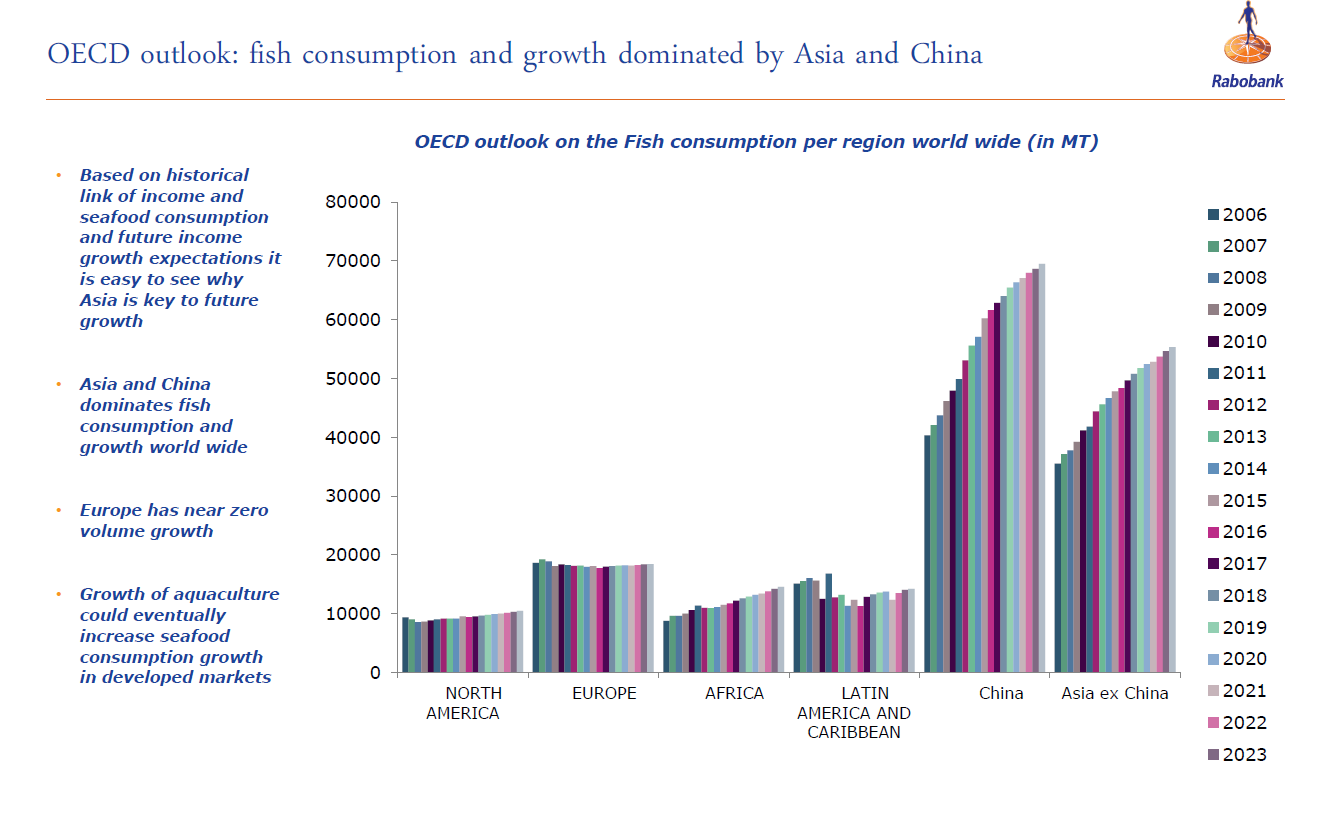

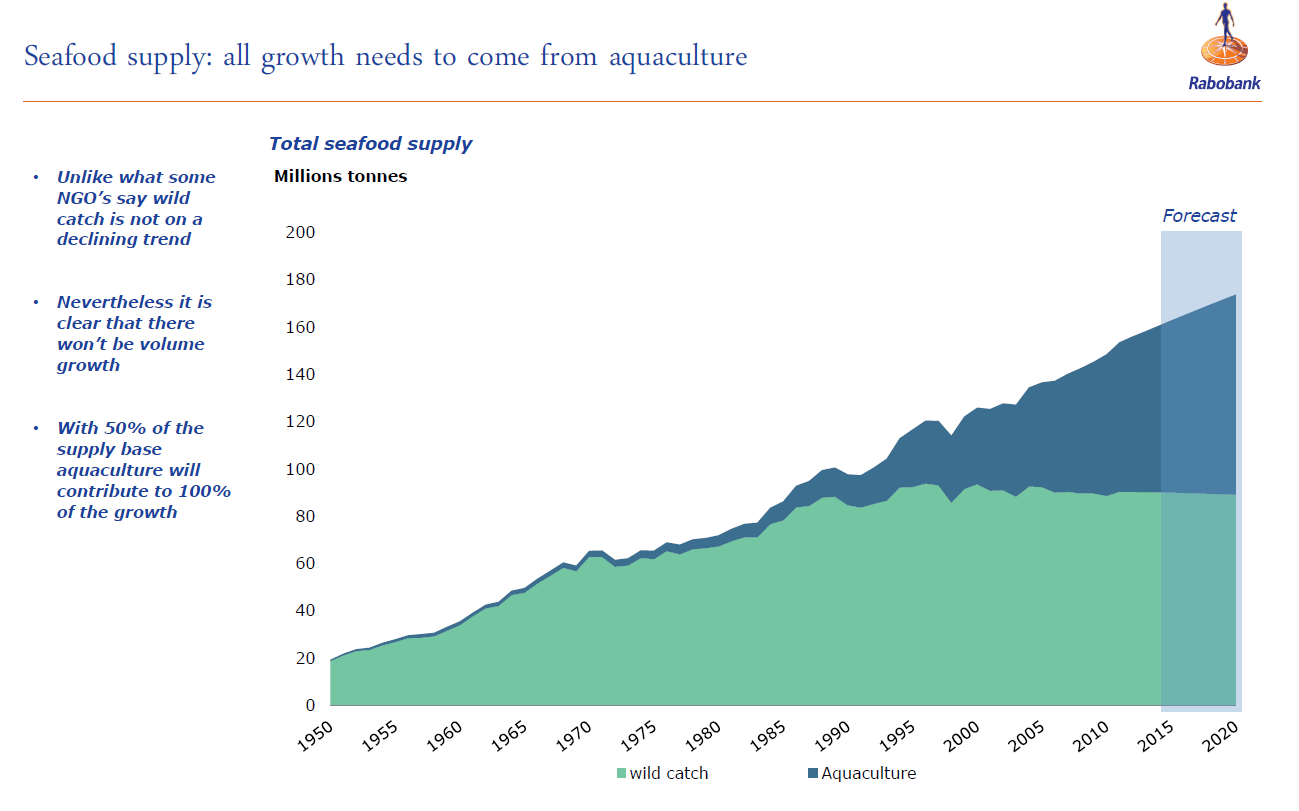

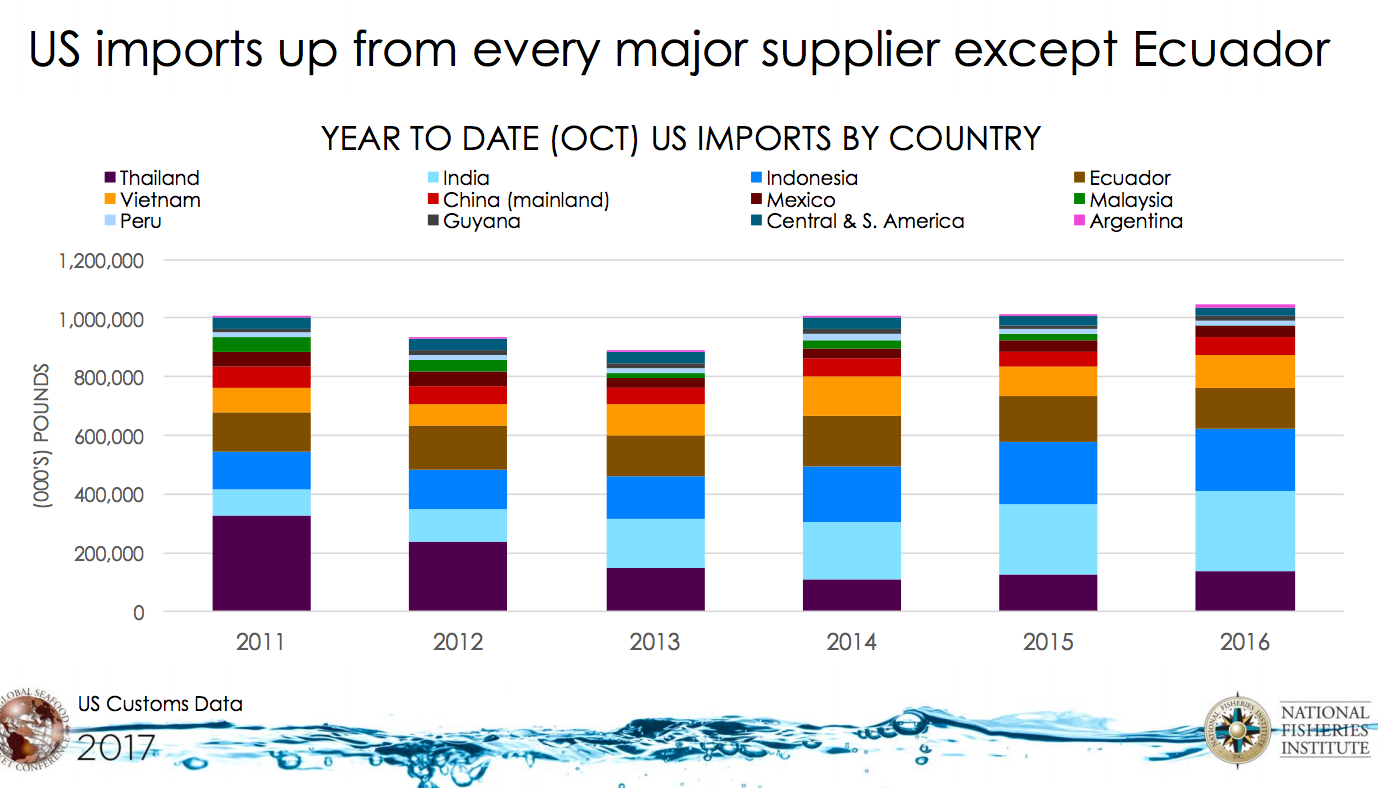

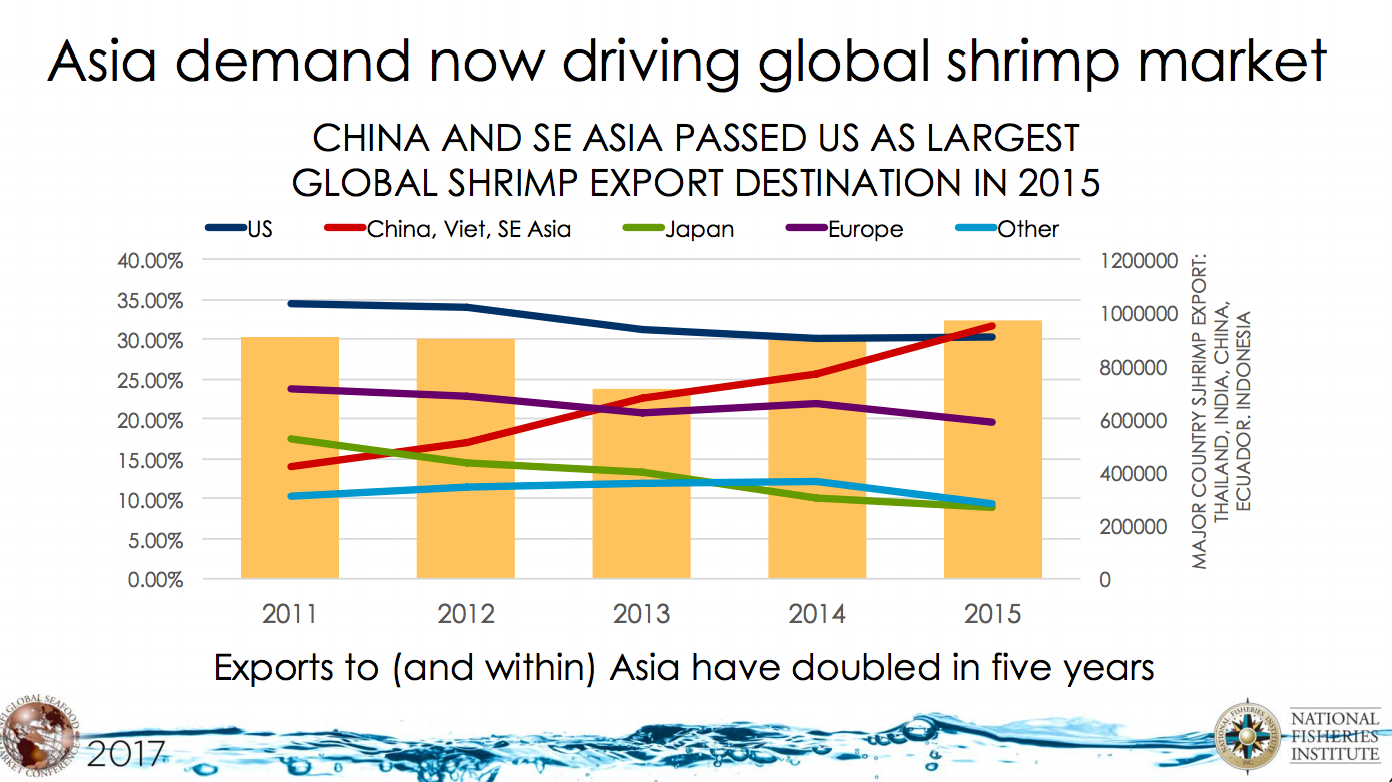

Some notes I had made while reading on the global shrimp market. Thought will share as it would be relevant here. Rabobank does great research on this area. We can follow a guy called Gorjan Nikolik from the bank. He is a seafood analyst with the bank.

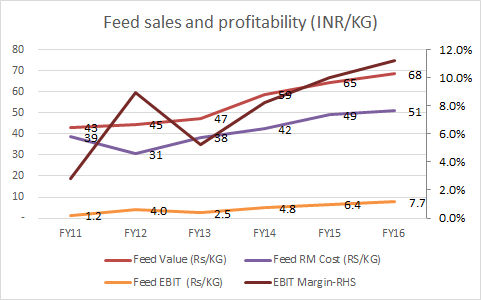

Some of the open questions gets answered by the graphs below.

Rgds

DV

Disc: Invested

p.s. all information presented above is in public domain

http://www.feednavigator.com/Markets/Skretting-to-scale-up-its-shrimp-feed-production-in-Ecuador?

some interesting articles for Avanti investors

Hi,

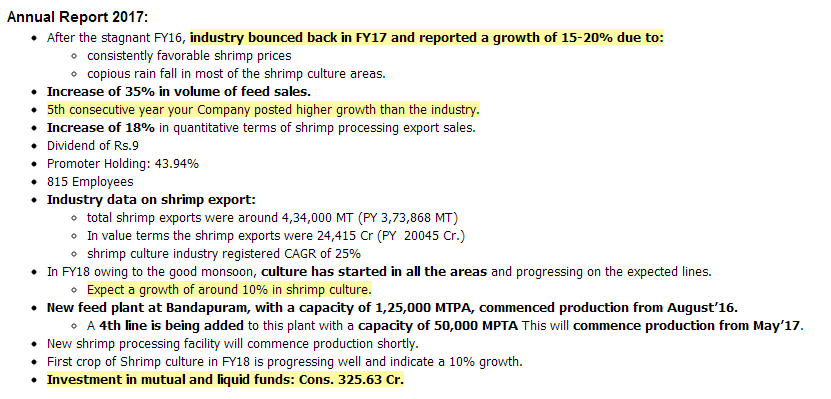

Sharing my notes from Avanti’s 2017 Annual Report.

Regards,

Yogansh Jeswani

Disclosure: Invested

The case in which Avanti and other shrimp exporters had against the Commerce Dept USA on Anti dumping duty seems to have gone against the companies. Any legal mind here can go through this report and decipher this for us http://caselaw.findlaw.com/us-federal-circuit/1867657.html

Hello Saji and others

Though I am not a lawyer but I had tried to understand this and had correlated it to some other information.

I will try and answer this via a series of questions.

Who was involved in this legal case?

On the 12th of July United States Court of Appeal passed a final verdict on the anti-dumping duties on frozen warmwater shrimp from India. The plaintiffs appellants (guys who are fighting) included approximate 24 Indian Shrimp companies and the appellees (these are the guys whom they are fighting against) were essentially shrimp trade associations of US.

What was the point of contention?

The point of contention was the anti dumping duty (ADD) for the period 2011-2012 @3.49%.

What was the claim of the Indian Shrimp exporters?

Without going into the details the Indians claimed that a wrong method of calculation was applied in arriving at the ADD.

If we go through the entire judgement we get to know the 3 ways of calculating the ADD

What was the final verdict?

All the claims of the Indians were rejected and it was upheld that the ADD for 2011-2012 would remain 3.49%.

What does it mean now?

Basically there will be no duty refund for the Indian companies.

How will it impact the share price?

No clue. But personally I don’t think this will impact anything. If it were favourable to the Indians then they would get an additional cash flow via refunds. But if they lost it would not make any impact to outflow of cash. Perhaps an opportunity loss though along with legal fee.

Also I would like to point that Indian companies are charged the highest ADD (I haven’t exhaustively studied this yet)

ADD for Indian Companies

2016-2017: 1.07%

2015-2016: 1.07%

2014-2015: 2.20%

2013-2014: 2.96%

2012-2013: 2.49%

2011-2012: 3.49%

Thailand on the other hand is charged 0.81% now. Since China doesn’t export anymore the ADD has been rescinded.

These data points can be found at the Office of the Federal Register.

I hope I was able to make some sense.

Regards

DV

Disc: invested

Marine exports continue to grow at a healthy pace. June 2017 figures show a growth of ~ 24%. Good prospects for Avanti.

Disc: invested in Avanti feeds

Hello all

I have been going through the annual reports (AR17 & 16) for the last couple of days and have some queries. The focus is on revenue and cost of raw materials.

Some pointers

On page 12 of the annual report under ‘Summary of Operations & State of Company’s affairs’ it states that ‘After remaining stagnant during 2015-16, the industry bounced back in the year 2016-17 and reported a growth of 15-20% due to consistently favorable shrimp prices coupled with copious rainfall in most of the shrimp culture areas.’ Now this ‘favorable’ shrimp prices means what? Shrimp prices of end product were higher than before? This page also gives the amount of shrimp feed sales in MT.

Then if we go to page 164 schedule 19 under ‘Revenue from operations’ we get the sales figures product wise in value terms. From the MT above we arrive at per unit MT price of Shrimp feed in 2017 and 2016. In 2017 1 MT of shrimp feed generated a revenue of Rs 68,657 and 1 MT of shrimp feed in 2016 generated Rs 68,468 of revenue. This increase in pricing of ~Rs 188 per MT actually produces an additional Rs 6.43 Crs of revenue. But on the other hand if we look at the MTs of processed shrimp for export and the revenue generated from processed shrimp there is a drop in revenue per MT. In 2017 1MT of processed shrimp for export generated Rs 4.17 lakh of revenue whereas this corresponding number for 2016 was Rs 6.02 lakh! If shrimp prices were favorable ie rising then this would not have been the case. If the company was able to sell at the same rate then that would add a good Rs 95 crs to the top line! I am not able to understand this drop in export revenue of processed shrimp per MT. We have already pointed that the duties (anti dumping & countervailing duties were constant). Also I was trying to see the global trend in shrimp prices as a commodity, and that has risen too. The INR has strengthened against the greenback. Does this have an effect, I am assuming greatly yes? But the export price drop seems large. (If we see the unhedged Fx exposure on 31st March 2017 its about 23 Crs so I doubt such a large change could only be due to Fx. I am assuming here. Please correct if required.)

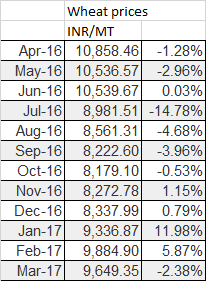

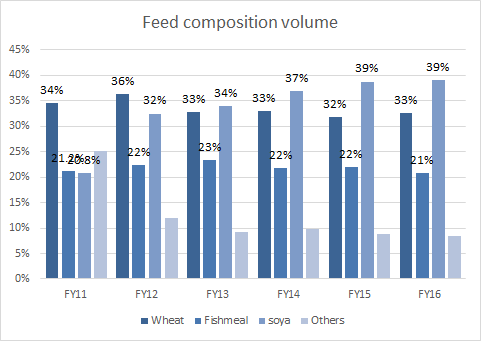

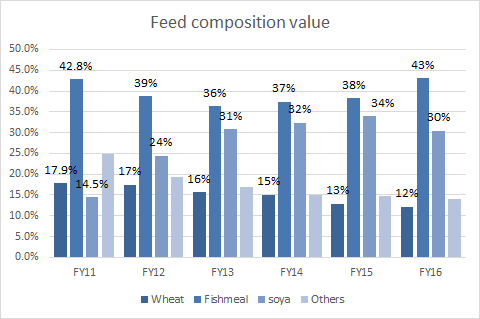

Now if we goto page 165 ‘Cost of materials consumed’ we look at unit price (lakh per MT) of each raw material constituent. The largest ingredient Soya DOC had a tail wind for Avanti and prices dropped by 4.5% (in one of the posts we have discussed this). But the second most important ingredient wheat & wheat flour actually became costlier by 13%. Also from page 164 we find that wheat production fell drastically for Avanti (from generating 27 lakh revenue in 2016 to only 2 lakh in 2017). I wonder why? Also the price of wheat as a commodity kept falling in the year. This too should have been a tailwind but it wasn’t why?

So my two questions in short are (if my reasoning above is ok)

a) Why did Avanti generate lesser revenue from processed shrimp export in 2017 than in 2016 despite a favorable environment?

b) Why did the cost of wheat & wheat flour as raw materials rise so much despite a fall in the commodity price of wheat?

Unfortunately I can’t get Waterbase’s 2017 AR otherwise I would like to confirm the trends there too.

From an industry point of view it seems being the leader in India is like being in the Goldilocks zone

Regards

DV

Disc: invested

You need to add Trading goods sold → Export Sales → Processed Shrimp revenue of 13,978 lac. Revenue from processed shrimp export will be 35,470 lac, which turns out to be 6.88 lakh/MT.

Wheat and wheat floor prices have got up to 21.6/kg in FY17 from 19.1/kg in FY16. One of the reasons could be as you mentioned company instead of producing its own wheat bran started procuring from the market.

Thanks Gaurav. Now the effect of rising shrimp prices makes sense after doing the correction.

For the wheat price please could you let me know where did you get the data from as I have data which says the opposite. My source is indexmundi.

Also I reconsidered the own wheat production point, they needed 1.06 lakh MT valued at 23,018 lakhs of wheat in 2017 whereas the wheat bran produced in 2016 was only 28 lakhs worth. So I dont think own wheat production would do much impact.

Rgds

DV

You have to look at wheat prices in India.

This Nov-16 article mentions MSP by GoI for wheat at 1625/ton.

Also, Agriwatch gives very good check on spot market price in India at various locations.

mate,

wheat is marginal for them by value, key ones are soya and fishmeal. sorry, too lazy to add fy7 details!!

Hi Narender

Thanks, yes wheat is marginal for them in terms of value (approximate 11% in FY17 and 10% in FY16). The point is that the cost of raw materials increased to Rs 59,224 per MT in FY17 from FY16 ie an increase of Rs 89/MT in FY17. This Rs 89 increase has added an additional cost of Rs 3.2 Crs despite the fact that there was a drop in costs of the two most important ingredients which contribute almost 60% of feed (soya with 10.5% drop + fish meal with 4.5% drop). So certainly the other ingredients which contribute 40% to the composition have not let the raw material cost drop drastically. The intent is to analyze what could have been better that’s all.

Aside, in the ET article shared by @sk_123 one of the questions is:

For domestic market only I was trying to understand, so then what clarity are you seeking right now?

A Indra Kumar: We need to import some some input ingredients. There is import duty an IGST. How do claim it back, there needs to be some clarity.

What is the ingredient which is imported?

Thanks & regards

DV

I am assuming the imports must be for processed shrimp. You can call-up (no malis) the company.

Just thought to share a snippet of a conversation had with the ED of one of the largest Shrimp Exporters (not listed) from India.

Q: Sir, how’s been the going this year?

Oh!, as you are aware it has been a fantastic year, and its looking good for India. There has been a marked preference for Shrimp from India in our biggest market US. It’s a remarkable strengthening of “perception” about sustainability of Indian shrimp industry and the quality it offers large global importers/consumers

Q: I remember we asked you this question last year 2016 Sep, why is everybody (processors, farmers) so confident that Indian exports will continue to grow 20-25% for a few years - when the demand supply gap (in earlier years) had closed, Global demand was growing only at 4-5% and supply from indonesia, Equador, Mexico, India, Vietnam were at similar levels ~ 3-4Lakh Tons? To grow, India would have to snatch market share from other countries??

And you remember that we had mentioned (among other supporting factors) the growing “feeling” that there was a perceptible shift in the way Indian shrimp industry was looked at post the EMS breakout in some countries; there was appreciation for the robust regulatory framework/quarantine and traceabilty policies; large buyers who look for developing long-term sourcing were looking at India with increasing interest.

Q: So how do you assess this playing out in the medium term for Indian Shrimp Exports?

Its all looking very promising. Buyers are now specifically ASKING for INDIAN SHRIMP - like they once used to ask about Vietnamese shrimp. This is India’s time, there is large opportunity to harness, and we in the Industry must make sure that we don’t mess up.

Q: This is huge. You had told us in 2015 when we first met - if the farmer gets his price and his happy - the whole industry viability, rests on that. So If Global demand for Indian Shrimp Exports keeps increasing, and global Shrimp supply remains stable as it has, then the Indian Farmer has good things to look forward to ??

Yes. Absolutely

We know most of us (still) invested in Avanti are wondering if at 35x trailing - everything is not factored into the price, and wondering about how to think through the way forward, and are a little uncomfortable holding through rich-valuation stages. As our friend Ayush says, it’s a good problem to have ![]()

Well - from our active experience over last 6 years (in rich valuation cases) there is one clear lesson. We need to focus and work hard at establishing only 2 things:

a) that the Industry is stable and growing

b) that the competitive position of this business is getting stronger or weaker

The AGM is at Vizag on 12 Aug. Most of my friends are dropping out this year. To my mind this is a very important year to attend and take the opportunity to hear/question firsthand the Management, Thai Union folks and other leading players in the Sea Food Industry - based on hard facts - why this is likely to sustain, and/or demolish that premise.

For those not familiar, here’s a back-peek into our 2015 Field Insights - that systematically collated data-points for a System2/Level2 (a la Daniel Kahneman/Howard Marks) analysis of the Indian Shrimp Industry sustainable viability.

AVANTI_FIELD_INSIGHTS.pdf (2.9 MB)

It’s a solemn responsibility we have to UPDATE this Avanti Field Insights presentation - in 2017, with relevant field work, followed by conversations around the AGM. Who wants to join in??

It would be v useful to update the field insights- i would v much like join and help in this exercise.

Hi Donald

I am planning to attend AGM on 12 August and would also like to join for the field visit. Pls do let me know, if I could be accommodated. Thank you.