My very first post on ValuePickr. Avanti Feeds growth trajectory has been great no doubts about that for sure.While i am bullish on its feeds division the shrimp processing and export division is seen as the next big wave for this company. While I was initially quite bullish on this company I have opted staying away from any shrimp based company primarily because of the following reason

- The indian industry has boomed due to the vannamei shrimp variety and avanti feeds and others have benefited leaps and bounds due to this variety which has higher yields that a tiger shrimp can . While all looks rosy for the time being but somethings not right. Chinas shrimp production has fallen 20% to 30% and thailand production is also taking a hit . Did anyone do a thorough research why ?

Well technically vannamei shrimps are much more resistant to diseases was one of the reasons why it was preferred over its counterpart tiger shrimps. With poor feed which does not meet the internantional standards, lack of soil and water preservation techniques followed by farmers and other larger producers, to excessive shrimps density in ponds has resulted in declining outputs and increase in different diseases. Check the below links for details

‘Deadliest’ shrimp disease raises fear - SUNSTAR

The issue is that india is not immune to the disease phenomenon. While bigger companies like Avanti might have some action plans to mitigate and minimize their produce to catch the diseases , but one cannot bet that Avanti is immune . To raise the issue under consideration check the research documents available on public domain on how widespread the problem with shrimp and disease is catching to India

http://www.iajpr.com/archive/volume-6/oct-2016/16oct06.html

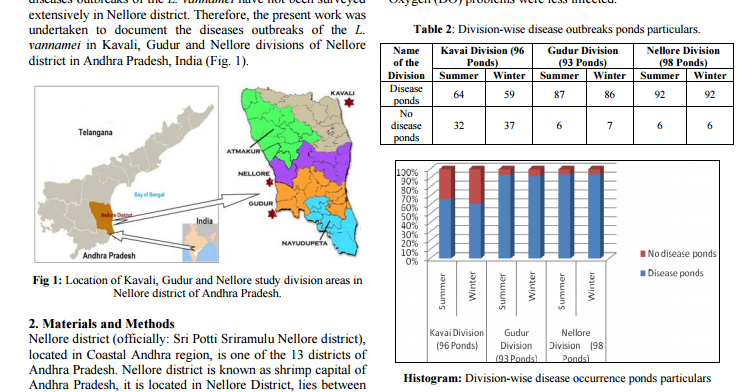

the second document highlights how rms ( running mortality syndrome and other diseases are catching up in India . And more alarming is the number of farms which are currently affected by it . Attaching a screenshot for the reference of fellow members

So out of the 287 ponds studied in the 3 regions more than 80% of the ponds had one of the diseases is an alarming sign for me. While I do believe the growth may continue inspite of increasing disease outbreak but unless you are an hawk eyed investor glancing through the smallest of news affecting the shrimp production in India , the investment in Avanti or any other shrimp producing company can be a highly risky bet .