Interested to know how the slump sale value would be reflected in Avanti standalone books?

They sold it at a consideration of Rs. 128 crores… What is the tax implication? Or there would be no tax implication on the sale?

They transferred Capital employed in business of processing shrimp worth 128 crores (assets - liabilities) … Then invested about 84 crores for 60% … Then 40% appx bought by Thai Union for 125 crores…

So as on date what should be the valuation of shrimp processing business… Imagine as if this company is sold to an outsider by both Thai Union and Avanti? What would be total value? I am trying to calculate the per share value of Avanti Feed shareholder after this 40% sell off? Suppose the outside buyer wants to buy entire processing business at a price Thai Union paid… That would be the amount he has to cough up?

@Gaurav_Agarwal Last year (FY15) the company had done shrimp feed production of 2.33 Lac MT and in the 2015 AGM the company had announced that they are expanding feed capacity by about 1.2 Lac MT. Hence the capacity of feed segment should be about 3.5-4 lac MT for the coming season. Like Aman pointed, the capacity in shrimp processing might be higher but as its a seasonal business, the utilization is lower. Last year they had sold about 3400 MT…and capacity was about 7-8000 MT. As per articles, the new expansion for the processing segment should add about 15,000 MT of processing capacity in phase 1.

@Aveek - I’m also not very clear. But we can try arriving at some nos - old plant has been valued at 128 Cr + 85 Cr infusion by Avanti + 125 Cr infusion by Thai…hence net asset value can be considered at about 340 Cr.

Since we all do not have exact information about the capacity of the company I thought it prudent to call the company and try to find out about the capacity, as always the management was courteous and forth coming in supplying the information.

Feed capacity expansion is underway which should add around 1 lac mt/annum.

I wonder why companies disclose expansion information to the magazines which treat the information as their property and charge money instead of doing a proper disclosures on stock exchange which are mandated by SEBI Listing Obligations and Disclosure Requirements

I am posting my understanding of the subsidiary transaction after interacting with the company …Please correct me if i am wrong…

A. Business transfer of shrimp processing to Avanti Frozen foods @ 128 cr

Transaction recorded in standalone books of parent Avanti Feeds Ltd …

a… Non- current investments(being shares of Avanti frozen foods) : 84.60 Cr

60,00,000 shares @ 141 each : 84.60 Cr

b. Loans & Advances : 43.4 Cr

B. Cash infusion by TUF in Avanti Frozen Foods

40,06,667 shares @ 313 each : 125.41 cr

C. Equity outstanding of Avanti Frozen Foods : 1,00,06,667 shares of Rs 10 each

D. Net Asset Value of subsidiary should be 210 Crs Loans outstanding around 44 crs and a proposed credit line for WCap needs of 62,25 Cr

Now, there is no cash infusion by Avanti Feeds as believed and also my sense is economic interest of TUF in subsidiary should be at around 55%

[40% direct and 25% *(60%) through parent company] but majority voting power should vest with promoter.

Overall, transaction looks good for Avanti Feeds shareholder as you will get 60% ownership in a total installed capacity of 23,000MT(new capacity of 15000mt) at no additional cost.

Thai Union, Avanti India value-added shrimp plant to be ready mid-year

My guess is only phase-1 15000MT will be ready by mid year and additional 10000 MT will be added later

The plant will be “state of the art” and house raw, cooked, and value-added production lines with raw material production capacity of over 25,000 metric tons per annum, Rittirong Boonmechote, who run’s Thai Union’s global shrimp business,“There is plenty of raw material in India. We have the skill in managing shrimp processing plants and can transfer our knowledge to the new JV in India and lift up the standard of the production and quality,” Boonmechote told Undercurrent last year.

India is well known for commodity shrimp production. Thailand, which has seen raw material supply dive from 650,000t to around 200,000t in 2014 due to early mortality syndrome (EMS), is more focused on value-added products.

With the planned JV plant, “the concept for us is more value-added products and less commodity products. Anything we do in Thailand, we can help our partner to do”, said Boonmechote, last year.

if we closely look at dec q3 results. They have already mentioned that capital employed in shrimp processing is 86 cr. A look on bse announcement (link below) by company also proves that they have already subscribed to 60 lakh shares of Avanti frozen on 31 dec. This clearly means that Avanti needs no new fund infusion to this JV as of now.

So in short the whole announcement on 16th March was just to confirm that the JV has been approved and 40% shares have been subscribed by Thai union at 125 cr.

What it means for existing shareholders of Avanti

The shrimp processing business is now valued at 313 cr. (Rs 313 * 1 cr shares)

Avanti share value @ 60% = 187.8 cr

If this is taken on the book value per share = 187.8/4.54 = Rs 41

I am not sure how the slum sale of 128 cr which is Rs 28 per share and this value Rs 41 per share contributes to book value of Avanti.

While I was looking at March 2015 balance sheet I see that total assets on standalone is 475 cr and on consolidated is 480 cr.

It will interesting to see how this sale impacts both book values.

he said avanti is still very very strong - they give the least credit and have the larger farmers so their throughput per shrimp farmer would eb much higher than Water base or CP and that will help them in margins

2.avanti is trying to build stickiness by buying back shrimps from farmers and processing and exporting. this type of double loop can be a very powerful network effect.

water base is geetting very aggressive in lending credit and ramping up market share.

pretty much all the products are more or lesss the same. so, its a question of the effectiveness of your feet on street. Avanti has a lot more people on thei rown rolls whereas water base is trying to get more distributors to grow faster.

overall,looking at avanti’s cash conversion cycle which is best in class and this initiative to impove farmer loyalty, I am quietly impressed.

I sold avanti at 550 or so but will try and re-add at 350 levels.

Prima facie the news looks negative but in my opinion its always difficult to gauge the impact on its own without taking into account the relative depreciation of currencies

Last hike had negligible impact (but that may have been on good demand on account of EMS in thailand)

Also the severity of impact depends on company to company as Falcon marine duty is expected to cut to below 1% while Liberty foods which mainly deals in black shrimp is around 8%. Devi foods duty is close to 3%. This may even turn out to be a blessing in disguise for organised player like Avanti who has BAP 4 certification although in short term it may impact feed sales until its own processing capacity scale up.

.Disclaimer Please do your own research as I am biased

2% is not a small raise given frozen shrimp is almost a commodity product with little product differentiation so price is everything.

There would definitely be some negative impact. The question of how much is something that we will find out in coming months data and need to monitor carefully.

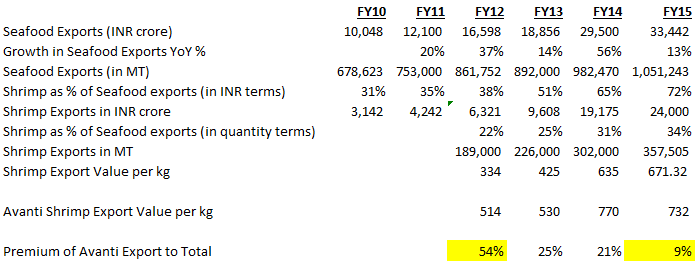

As can be seen, Avanti commanded a 54% premium in FY12 to industry standards of per unit shrimp exports. This has fallen to 9% in FY15. (Please note that Avanti numbers exclude export incentives of ~7%).

Perhaps:

a) Avanti is facing competitive pressure on the shrimp processing business and is unable to maintain the earlier premium, and/or

b) Avanti has changed the quality of shrimp (count size) lending to lower realizations

Is this a concern ? Am I overlooking something?

Much of the future growth prospects lie in the TUF joint venture and would be linked to shrimp processing - wanted to understand this better from those tracking this business closely.

the person in the second video is an indpendent producer by using his own land.

he was refering to low cost production of shrimps by using plant protein as feed

he is using soya and husk of til seeds after extracting oil as feed . and the plant

protein help in improving imuunity levels of shrimp to fight against viral and protozoal infections

this is my first post in the forum thank u all

Satya

More then anything Avanti requires a strong stomach to withstand periodical rumours or news or conjectures of disease, cyclones, anti dumping duty , prices declines etc which keeps on coming at regular intervals.

There are some astute stock pickers who bought Avanti very cheap at 20 Rs pre split few years back but sold out too soon doe to these variables . And there are some who are still holding on to Avanti even now after buying at same price looking at big picture and withstanding these developments. They have achieved financial independence in life due to their temperament and confidence in Avanti.

Avanti has a lovely scalable business model due to huge opp size n v ethical promoter with execution track record of 23 years

Discl- I am invested in Avanti since Feb 14 n it’s my top holding