People who are already holding as muti-bagger, it’s wiser to see the qtr result. Since, even if the result as not expected, it won’t fall so fast. You will get plenty of time. There will be always some investors, who will enter at higher price. So keep chilling and spread good msg only and do not encourage -ve msgs.

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/7BAA6E5A_D907_46ED_9448_89C66A3B88EC_175243.pdf

Q2 results are out

Flat topline

Good growth in NP 44cr vs 34 cr EPS 48.4 vs 37.6

avanti results again are a mixed bag. bottomline great, topline flat

Total Income flat at 532 cr vs 531 cr y-on-y

Domestic sales up from 439 to 449 crores.

Exports down from 90 cr to 77 cr.

OP up from 51 to 60 crores.

NP up from 34 to 44 crores.

EPS up from 37.6 to 48.4

Half yearly eps at 98.73 per share.

Co looks to be on track to achieve EPS in the vicinity of 200 per share. (or nearabout)

Long term borrowing at 3 crores. Current investments at 111 crores and cash and equivalents at 13 crores.

Net cash balance sheet.

disc: invested and occupies more than 10 of PF.

8 Likes

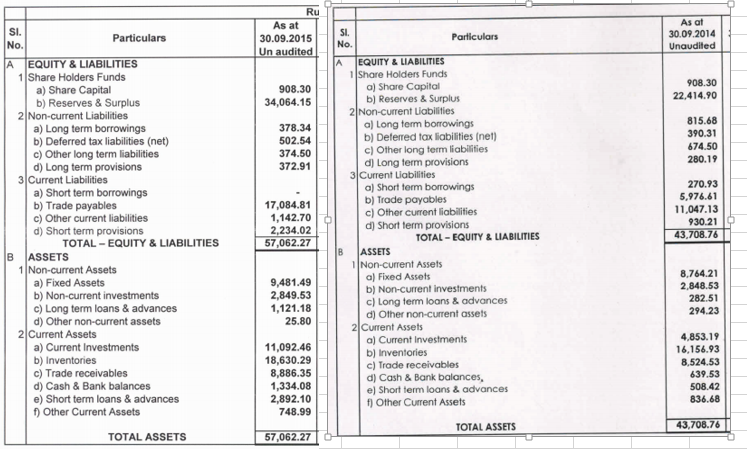

Current Liabilities -> Trade payables (increase); Other current liabilities (decrease)

Is this you want to highlight ?

Disc: Invested, more than 10% of PF

trade payables have increased by a whopping Rs. 110 Cr. but then it could be a reclassification issue - given other current liabilities have shrunk massively. so, my guess is not that.

Provisions have jumped up 100% from 9 Cr. to 22 Cr. - so that could flow into write-offs assuming that this is on their inventory or hits on products they shipped already. that’s an worrisome sign IMHO.

Other current liabilities have decreased sharply from 110 cr to 11 cr. Major contribution to this comes from Customer Advances. This could be a strategic move by the management to increase the margins. since their receivables is in comfortable position and they have enough cash balance, they might have taken this decision to improve margins (higher selling price)

Hi @dkirand ,

I would agree with @varadharajanr that this could be more due to some re-classification or may be there were loans to be repaid last year which get classified as current liabilities. It can’t be due to decrease in customer advances as it used to be just about 15-20 Cr last year as per the annual report.

Regards,

Ayush

1 Like

During the year Inventory writedown is typically not routed through provisions. It would be adjusted in Inventory Valuations itself. So there typically is never a writeoff of Inventory Provision in financials.

In case of Avanti, provisions include -

- Proposed dividend

- Dividend Dist. Tax

- Provision for tax

If they are planning a slump sale/transfer of shrimp processing unit, there would be a Capital Gain Tax for that which could affect Provision for Tax figure.

2 Likes

Trade Payables and Current Liabilities have a very thin line.

For eg. Payables for RM would be Trade Payables, but payables for logistics costs would be Current Liab.

Often companies have confusion and auditors make them reclassify such figures.

Even in Avanti’s financials, the biggest component of Current Liablities is Creditors for expenses

1 Like

ashwini

thanks - the way I thought about it was such short term provisions are also created for issues related to product liabilities - eg., warranty claims, deficiency in quality. Given that I know for a fact that there have been a few issues, is it possible that they created a provision which they will flow into the P & L whenever approrpriate (when litigation is complete or negotiation is done), so could it be a few containers of shrimps which are returned/of lower quality which will soon hit the PL.

your views would be enlightening.

Provision anyways hits PL before coming to Balance Sheet. Try passing a JE for inventory hit without routing through PL.

Also this kind of expense would have shown in the margins or the exceptional items in PL.

1 Like

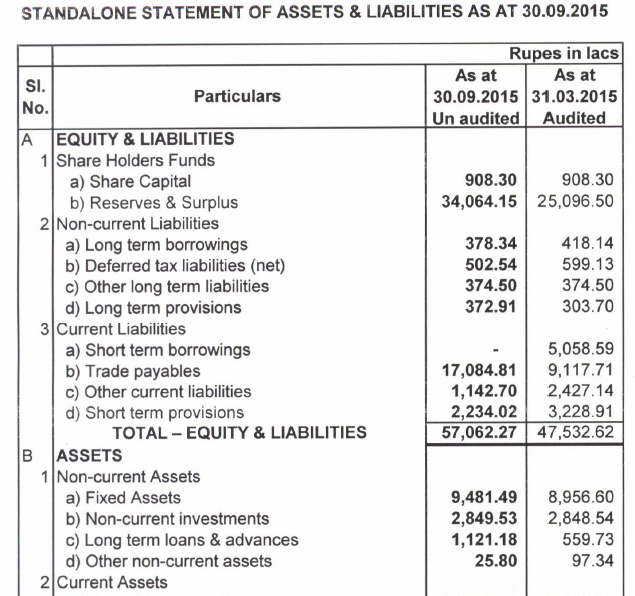

I just re-went through the post of @dkirand. I think the confusion will go away if we compare the balance sheet posted by the company:

The major variation between trade payable and current liability seems to be due to reclassification of heads.

Regarding the point raised by @varadharajanr, the provisions have reduced from 32 Cr as on March 2015 to 22 Cr as on Sept 2015 and these could be general in nature.

Regards,

Ayush

2 Likes

Excellent Accounting stuff explanation Ashwini. I never thought there would be a difference in classifcation of trade payables vs current liabilities and between RM and logistics cost. Thanks much.

Thanks Varadha. Looks like unless you are a private equity fund, you can’t pass a inventory writedown just via the balance sheet  - ( https://foragerfunds.com/bristlemouth/dick-smith-is-the-greatest-private-equity-heist-of-all-time/ )

- ( https://foragerfunds.com/bristlemouth/dick-smith-is-the-greatest-private-equity-heist-of-all-time/ )

Thanks Ayush. Given the nature of Avanti’s business, it would be unfair to compare Q4 to Q2 balance sheet. I was trying to understand the flow of business YOY. But your re-classification point is well taken.

My confusion stemmed from the fact that given Avanti wanted to ramp up shrimp processing (as feed business can only take it so far - or so, it seems from the surface), it was only logical that they might have procured shrimp from farmers (apart from in-house production) in exchange for selling them feed. This might have bloated trade payables. But then again, shrimp processing revenues (volume not given unfortunately) has steeply fallen. So, there was a dichotomy.

But if it’s just re-classification, then we should be ok. Balance sheet is anyway quite strong.

Kiran

3 Likes

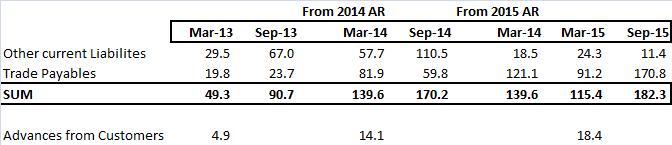

Till 1 hour ago, I was in @dkirand camp on this- This big decrease in Other current liabilities is sign a worry since most of this should be Advance from Customers. And we all know, a big decrease on that front is a big sign of worry.

However, after @ashwinidamani and @ayushmit explanation, my mind asked me- Now which camp are you in, Sir? ![]()

So, I decided to check the past trends of Other Current Liabilities, Trade Payables & Advance from Customers.

And the result is - There was Reclassification (from Other current Lia to Trade payables) in March-15 Annual Report.

i.e March 14 Balance sheet numbers were reclassified in 2015 AR.

So, Sept-14 & Sept-15 Other current liabilities are not like-to-like.

Full data below-

Have captured Mar-14 numbers from both the balance sheets - AR 14 & AR 15.

8 Likes

Is year on year no growth in revenue any cause of worry?

q2fy15 - 532 cr

q2fy16 - 533 cr

Avanti has also shown decrease on cost of material consumed

q2fy15 - 429 cr

q2fy16 - 405 cr

which resulted in 29% YoY growth in Net Profit.

I tried to compare these number with only other listed feed company Waterbase but this does not look like industry trend

revenue

q2fy15 - 82 cr

q2fy16 - 99 cr

cost of material consumed

q2fy15 - 42 cr

q2fy16 - 48 cr

Any insights?

While it is a worry, it shouldn’t be a surprise as there were reports of farmers going for low stocking with low shrimp prices being told as the main reason and fear of EHP disease being another ‘lesser’ reason. Shrimp processors have been struggling to get enough raw materials and this should help shrimp prices which have been raising. Regarding EHP, check this article:

Disclaimer: Major portion of portfolio, invested from lower levels and converted the recent dividend into shares yesterday.

Avanti Feeds Ltd has fixed November 27, 2015 as the Record Date for the purpose of ascertaining the entitlement of the members for sub-division of equity share of Rs. 10/- each into 5 equity shares of Rs. 2/- each.

http://www.equitybulls.com/admin/news2006/news_det.asp?id=173558

When EHP in an area is left untreated, bad things happen. It has been especially prevalent in China for a number of years. The spores build up in the environment, resulting in slower and slower growth.

If the first year farmers could produce 20-gram shrimp, they might see 15-gram shrimp in year two, and 10-gram shrimp in year three.

This is largely the story of China shrimp culture at the moment. Farmers have been unable to produce large shrimp, and they are turning to antibiotic use to treat disease.

As a result, China exporters have had to import shrimp both to get the size range they needed, and to guarantee antibiotic-free shrimp to ship to the US and elsewhere.

The spike in rejections of shrimp from Malaysia due to high levels of antibiotic residue is also to be traced to this problem. Chinese growers who could not sell to local processors apparently transshipped their shrimp to Malaysia, and the rejections for antibiotics spiked by the FDA.

In recent months Malaysia has cracked down and successfully prevented this practice, and FDA rejections have fallen sharply as well.

Finally, unlike EMS that led to widespread mortality, it appears that the impact of EHP is more akin to that of sea lice on salmon… it slows their growth and weakens them but is not usually fatal.

As a result, it will be hard to pick the EHP signal out of the normal variation in shrimp farming results based on weather, other diseases, feed and broodstock health.

EHP is not likely to dramatically collapse production the way EMS did, however it is a headwind that will prevent production growth to a greater or lesser extent in various regions.

Because detection has not been perfected it is hard to know for sure the extent to which the spores already have spread.

It does seem clear that the newer production areas where there has been a spectacular growth of output, such as India, will see a leveling off as ponds become less productive in their third or fourth year, leading to lower density, or more failures to grow large shrimp in higher density ponds.

1 Like

One of the reasons attributed to flat topline growth for q2 fy 16 in case of Avanti is that the ponds and shrimp producers observe a 45 days production holiday to reduce chances of disease.

I got this info while talking to a fellow investor who is a keen follower of the industry and its trends.

4 Likes