Make sure you add value to the stock discussion. This kind of one liners are strictly avoidable.

4 Likes

This is a double blow for Ashok Leyland. Such a capable manager leaving to join a competitor (I don’t know if he’s going to be CEO for only Royal Enfield or whole of Eicher?)

I thought when Dasari said it’s time for new learnings as reason for leaving ALL, he’d join some other industry or maybe retire.

Wonder why Ashok Leyland couldn’t retain him! Big loss in my opinion since good managers are so hard to find in Indian CV industry.

3 Likes

It is for Royal Enfield only. RE is getting a CEO for the first time. Siddhartha Lal will continue as overall Eicher Motors head.

Still, it is disappointing that ALL couldnt retain him.

2 Likes

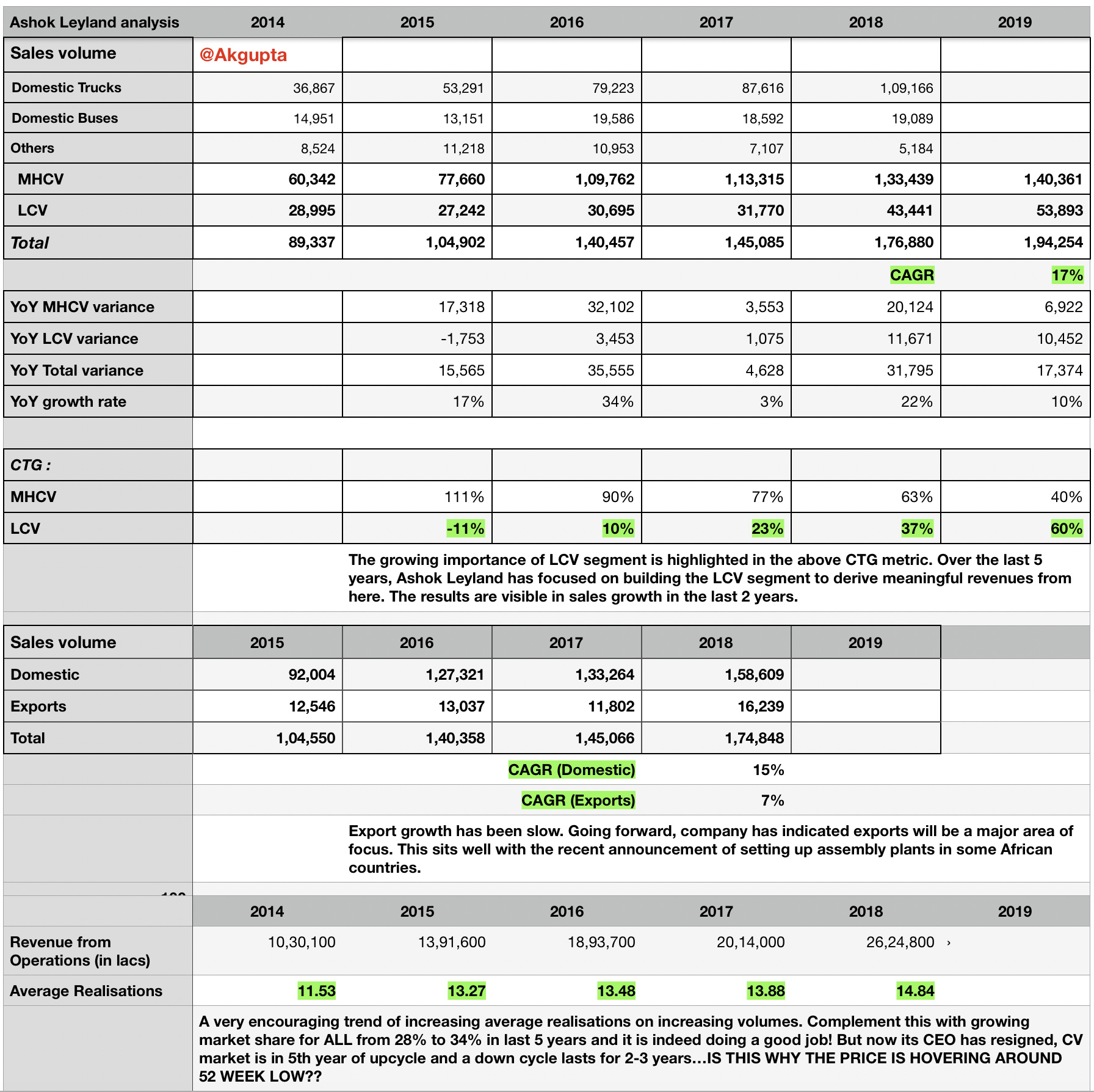

I frequently try to analyse numbers of companies in my portfolio and I have conducted a similar exercise for ALL. I have only looked at 5 year sales volumes and realisation numbers for ALL and they do paint a good picture of the company (All numbers can be referenced in the snapshot below)

The gist is -

- Company has been able to more than double its sales from ~90K units in FY14 to 195K units in FY19. Operating revenues have grown 2.6X in this period.

- Particularly in the last 2 years, volume growth has come from LCV segment.

- Average realisation has gone up from Rs 11.53 lacs in FY14 to Rs 14.84 lacs.

- This stellar performance is coinciding with CV up-cycle which started in FY14. How long will this up-cycle last is anybody’s guess. Much depends in how the BS6 pre-buy goes in FY21.

- Company’s future growth will come from emerging segments like LCV, exports & defence, thus reducing the reliance on trucks & buses sales which are cyclical in nature.› In line with this strategy :

-

LCV sales growth is clearly visible in last 2 years

-

Co has won some 31 tenders in defence segment (Orders from these tenders are yet to start coming in. Probably once the elections are over, orders will pick up again. This was discussed in Q3 FY19 concall)

-

Exports have grown at 7% CAGR but recent announcements to set up assembly plants in African countries and order wins for buses in Bangladesh bode well for the company. They are also trying to establish a foothold in some Middle East markets.

9 Likes

2 Likes

Fantastic Dividend.

5 Likes

Ashok Leyland June Sales update. Auto woes continue

Have been studying ALL and posting some thoughts.

ALL and the M&HCV Market:

Ashok Leyland had about 25% market share during the previous downcycle in FY13, FY14. Over the past few years, the company has strengthened its position a lot by focussing on increasing distribution network and offering premium-ish products. Now, their market share hovers around 33%-34%.

The company is a very stronger player in South India but weaker in Northern and Eastern markets. Increasing their distribution in those markets helped increase their market share, however still not as good as they are at South. So the company may not benefit from any sudden growth in the market from Northern markets. This has happened in Q4FY18.

The M&HCV market is seeing lots of discounting from competitors. Though ALL is not the one driving the discounts, they are having to follow the route to some extent to stay competitive. The management is not at all happy with the discounting in the market and thinks it is not very sustainable for competitors to continuously do so. ALL believe in offering premium products, providing better service, penetrating distribution network over discounting. So they do walk away from deals where they have to provide the truck as well as leave money in the table to fleet operators. ALL’s average discounts are increasing however with time. So need to be a bit careful.

Market is observing a shift towards higher tonnage trucks. This is because of emergence of hub-and-spoke model being adopted by organisations after GST. So realisations of the company have been improving. Coming to growth rate of the market, CV industry follows the GDP growth rate of the country in the long run. If a company wants to grow faster than the GDP growth rate, then it should either increase its market share or increase its revenue share from exports.

Trucks will be the last ones to be affected by EV. However, intracity buses might be one of the first ones. ALL is already in the game here by trying out three variants like - Fast Charge, Swap, and Flash. Their swappable battery EV buses have been receiving some good attention from media.

From the MD to the entry level executive, everybody has three metrics in the company and the variable pay (performance bonus) is connected to that. Those three are market share, profitability and working capital. So all the three need to be balanced.

Innovation:

During the BS IV transition, all the competitors went to traditional solutions like SCR or EGR, however, Ashok Leyland has come up its in-house developed solution called iEGR, which is more Indian specific solution. One can go through the below video to understand how this works.

Though some European competitors involved into cheap tactics of publicizing negatively about the product, sales of Ashok Leyland stood strong which only suggests this was a successful technology. In fact, some STUs found that the TCO for iEGR vehicles is much lower and insisted on buying those.

The company is now working on modularizing its manufacturing process. They expect this to reduce the costs of the company. Coming from software engineering background, I’m a big fan of modular programming and comes with lots of benefits like easier plugging / unplugging of systems, localization of implementation and easier learning for new engineers. I’m not sure how much of the same benefits exist in truck manufacturing too but management says it will reduce their cost and is excited about it.

Another quick example I can think of is Ashok Leyland Sunshine school bus which has lots of safety features.

ALL is the only CV company to have achieved two Deming awards, which is like a pinnacle of quality.

Revenue Mix:

Have taken statements from management through various conference calls.

So these are only my estimates. So please take with pinch of salt.

Domestic M&HCV Trucks => 65-70%

Domestic Buses => 6-7%

LCV => <10%

Exports => 8%

Defense => 6-7%

Some other statements which I heard from conf calls are: For trucks are 20% of demand is from tippers; 40-45% of demand is from construction; Tippers + ICV account for 40%; Scooter carriers, car carriers account for 10%.

LCV Business:

LCV business was launched in the beginning of this decade and is a successful turnaround for the company. Dost, which is their flagship product for LCV, is super successful. They are not present in all ranges possible in LCV at the moment. The company plans to come up with lots of LCV products to fill the gaps in its product portfolio after BS VI transition. Current product portfolio addresses only 40% to 45% of the market.

LCV business operating margins are higher than the M&HCV business. So once this achieves scale, this should be margin accretive to the company. LCV business is far less cyclical compared to M&HCV and hence should also help de-volatize the company’s performance.

Other businesses:

ALL also sells gensets and spare parts along with commercial vehicles. However, I’m not too excited about these as their contribution to total revenues is low. On the gensets part, there has been no volume growth as they used to sell 15000 to 20000 gensets per year 10 years back and still at the same level now. Gensets contribute about 2.5% and Spare parts contribute about 6-7% to total revenues.

ALL also has a subsidiary called Hinduja Leyland Finance Limited (HLFL). This is an NBFC companies whose loan book primarily consists of loans given to M&HCV customers. 50% of their loan book is of M&HCV sales. Remaining comprises of 2W, 4W loans. And to some extent, even housing loans. Revenues are increasing strong from 814 crores in FY15 to 2560 crores in FY19. And profits have risen from 111 crores in FY15 to 275 crores in FY19.

Other subsidiaries which the company has are Optare and Albonair.

Optare is on the verge of turning around according to the management. However I see that its sales haven’t been rising much over the years and is continuously posting losses across the years. However, the losses (80 crores) are small enough to make it ignore it for now.

Albonair works on developing SCR systems which are to be used in Euro 4, 5 and 6 norms. The numbers of this company are too small to worry about (Revenues < 20 crores) for the size of the company. So didn’t dig too much.

How is ALL paning out in the current slowdown?

I’m focussing more on M&HCV sales as they form the major part of the company. LCV business just started getting momentum and is yet to take off fully. If you look at the monthly sales data below, you can see that the sales were down by 7% in Q4FY19 and 16% in Q1FY20.

However, this needs to be looked at with perspective that Q1FY19 has shown an exceptional growth last year. Below table would help you with that. Q1FY18 to Q1FY20 CAGR gives me CAGR of 9%. So I’m not really disappointed with Q1’s performance.

| M&HCV (Dom+Exp) | 2020 | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | |

|---|---|---|---|---|---|---|---|---|

| April | 8918 | 8968 | 6549 | 7873 | 6549 | 4523 | 5251 | |

| May | 8635 | 10421 | 6139 | 7469 | 6888 | 4884 | 4932 | |

| June | 8427 | 11257 | 9202 | 8685 | 8016 | 5501 | 4717 | |

| July | 10996 | 9026 | 8182 | 8835 | 5750 | 6266 | ||

| August | 13158 | 10567 | 8201 | 8903 | 5832 | 4939 | ||

| September | 14232 | 11804 | 8958 | 12146 | 6625 | 4715 | ||

| October | 9797 | 9140 | 9575 | 7176 | 5865 | 4093 | ||

| November | 8718 | 10638 | 6928 | 6297 | 5204 | 2715 | ||

| December | 11295 | 15948 | 8782 | 9703 | 7210 | 3890 | ||

| January | 13663 | 13643 | 12056 | 11208 | 8009 | 5530 | ||

| February | 12621 | 13726 | 11329 | 10801 | 8230 | 5576 | ||

| March | 15235 | 17057 | 15277 | 13240 | 10027 | 7718 | ||

| Total | 140361 | 133439 | 113315 | 109762 | 77660 | 60342 |

The company is attributing the slowdown to the NBFC crisis as the whole industry depends on financing. Speaking of monthly sales, you can clearly see that the industry is seasonal and sees much higher sales in Q3 and Q4.

What’s coming next?

With the company achieving its vision of Global Top 10 players in M&HCV trucks and Top 5 in buses, its next goal is to be among Top 10 in CVs. Listed out some points which would help the company grow in coming years.

- BS-VI prebuy: Fleet operators are well aware of technicalities like BS-IV, BS-VI unlike car owners. So CV industry expects pre-buying during BS-VI transition. This should help pick up sales from Q2 and Q3. Pre-buy happens as vehicles cost increase after BS-VI introduction.

- Modular Platform: Modular Platform should help the company increase its product portfolio and also help manage its costs effectively.

- Scrappage Policy: After the BS VI, govt is expected to introduce scrappage policy which will help replace lots of trucks older than 20 years. Industry estimates there would be at least 3 lakh such trucks. So even if 20% such trucks are replaced, that would give additional 60000 sales. Current M&HCV industry size is close to 4 lakhs. If scrappage policy would be at 15 years, then the number of vehicles to be scrapped is even higher at 6 to 7 lakhs.

- Broader portfolio with LHD Variants + Fleshed LCV Portfolio: LHD variants will help penetrate export markets. BS VI would give entry into lot more export markets to whole auto industry. Booming LCV business to get more momentum with new products.

Current capacity of the company is at 200,000 to 220,000 for M&HCVs, with a bit of de-bottlenecking required, which will help the company grow without significant capex. Capacity fo LCVs is about 75,000. This might need to be pushed ahead given the rate at which their sales are growing.

The company suggested that CVs in the next decade might start making money in solutions mode than product mode. Will have to see what kind of interesting business models will emerge. I think this will be lead by EV penetration (mainly in buses segment).

Efficiency metrics:

20%+ consolidated ROCE during the good times, however <10% during bad times like in FY14.

However, standalone ROCE is much higher at ~30%.

Working capital is very strong. Continuously decreasing and almost close to 0.

| Working Capital | 2019 | 2018 | 2017 | 2016 | 2015 | 2014 | 2013 | 2012 | 2011 | 2010 | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| Inventory Days | 33.55304742 | 26.77011275 | 41.79745666 | 31.20781239 | 36.81676448 | 48.67171966 | 55.17158294 | 62.89675753 | 72.419528 | 81.74229069 | |

| Receivable Days | 29.76065044 | 14.25395193 | 15.59487411 | 23.72456707 | 31.81812809 | 43.53479239 | 41.30290568 | 34.70375815 | 38.85755609 | 50.99719713 | |

| Payable Days | 56.72462033 | 61.53442669 | 51.06190878 | 43.85092324 | 72.43599437 | 81.7192023 | 72.3207859 | 72.49335325 | 99.59998184 | 129.3347665 |

Valuation:

P/E ratio of 11. Historically it was trading at 10-20 during the good times.

However dividend yield is high at 4%

Concerns:

- High debt of 15000 crores and low interest coverage ratio of 3 as per consolidated statements. I think this is due to their finance subsidiary (HLFL) which inflates their debt / interest numbers. They were planning to launch HLFL IPO and separate it out but couldn’t due to NBFC crisis breakout as they wouldn’t get the right valuations. Debt and interest coverage ratio look much better in the standalone statements.

- Every Annual Report starts with a letter from the chairman talking about the achievements. However, it was skipped in FY14 which was the worst year for ALL over the past decade. Also in the same FY14 AR, the consolidated financial statements didn’t include FY13 numbers avoiding comparison.

- Exit of Vinod Dasari to Royal Enfield. This man has played a super important role in the company over the past decade. Search for new CEO is still going on.

- Company is trying hard to increase their exports to 25% of revenues but has consistently failed to do so. Bright side is that they acknowledge that they didn’t achieve it and are now going to introduce LHD variants to penetrate more markets and are going to come with lots of LCV products post BS VI transition.

- Other expenses like “Power and Fuel”, “Service and Product Warranties”, “Packing and forwarding charges”, “Selling and administration charges” are increasing at faster rate than sales.

- GDP slowdown of the country. If this is a structural slowdown, CV industry would be badly impacted. However, if this is a temporary one, this is a good buying opportunity.

Further Research Ideas:

Gather construction and mining data from an official source and correlate it with ALL sales to check if we can get any interesting insights / lead indicators. If anyone knows any source, request you to share. I can dig if we can get interesting conclusions.

Discl: No holdings. However, find the current opportunity interesting. Please do your own research before investing.

32 Likes

ALL Press Release on Q1Fy20 results

Ashok Leyland : Q1 FY '20 Revenues at Rs. 5684 Cr; EBITDA at 9.4%

Gains Market Share in M&HCV 81 LCV

Ashok Leyland Limited reported a revenue of Rs. 5,684 Cr which was 9% lower than the same period last year (Rs. 6263 Cr). The Total Industry Volume had

come down by 17%. PBT for the quarter was at Rs. 361 Cr (Rs. 536 Cr) and PAT was at Rs. 230 Cr (Rs. 422 Cr).

EBITDA for the quarter was at 9.4%. The Company’s market share in the MHCV segment for the quarter grew

bv 4% to 34.1%.

Mr. Dheeraj G Hinduja, Chairman, Ashok Leyland Limited said, “While the industry has witnessed a decline in

volume of 17%, Ashok Leyland’s market share has grown by 4%. Our EBITDA at 9.4% despite decline in revenues

signifies efficient cost management in the Company. We are well on course to introduce BS VI vehicles and will

be seeding vehicles shortly. Despite a drop in TIV by 5%, our LCV business continues to do very well and posted

a growth of 12%.”

Mr. Gopal Mahadevan, Whole Time Director and Chief Financial Officer, Ashok Leyland Limited said,

“With signs of slower demand, we are closely watching the developments in the industry. We continue to take

cost out and drive productivity and growth initiatives.”

The Company has published the Consolidated Quarterly results for the first time in this quarter.

The company launched a slew of products in this quarter; Boss 1916,4623 Tractor, 4223 MAV, High Horse Power

Tractor 5532 and the 24 & 32 feet fully built containers in premium and economy segment were the star

introductions. Under the Customer Solutions Business, the Company also launched “Sadak ka Saathi” a

breakdown assistance program with Hindustan Petroleum Corporation Ltd. This introduction makes

Ashok Leyland, one of the largest roadside assistance providers in the country for Commercial Vehicles.

In July '19, the Company has launched “Oyster”, the next generation AC midi-bus in the premium category.

These multi-purpose premium airconditioned bus range has been designed and manufactured in-house for staff

and tourist commuting.

4 Likes

To expand in Africa

1 Like

Commercial Vehicle sector has been sharply affected by the economic-downturn.

News are reporting a sharp fall in sales figures of the market leaders:

Ashok Leyland

Tata Motors

Eicher Volvo

Mahindra and Mahindra

CV sales fell 60% YoY.

Bad times for these stocks. These stocks are cyclical in nature, and cannot be evaluated the same way as regular stocks, therefore am not sure what is good value.

2 Likes

Good analysis

(I found it via Twitter post by Dinesh Shriram )

14 Likes

Thanks for sharing.

I compared the charts of Ashok Leyland with one of their biggest ancillary parts partner Jamna Auto. The charts are mirror image in terms of levels in downturn to upturn and value it created for the investors.

Personally, I agree with the thesis - this is just playing a CV cycle - only we dont know where or when is the bottom done. I foresee lot of pain with no immediate recovery but also feel could be worth the wait & pain.

Disc : Tracking Ashok Leyland but invested in Jamna Auto at 33

1 Like

ALL has captured market share during the previous slowdown in M&HCV from 23% in 2012 to 28% in 2015. Looks like they are doing the same with LCVs now.

| Monthly Sales of LCV (D+E) | 2020(ALL) | 2019(ALL) | 2020(Tamo) | 2019(Tamo) | 2020(ALL%/ALL+Tamo) | 2019(ALL%/ALL+Tamo) | |

|---|---|---|---|---|---|---|---|

| April | 4280 | 3709 | 13996 | 14620 | 23.41869118 | 20.23569207 | |

| May | 4226 | 3238 | 12695 | 15558 | 24.97488328 | 17.22706959 | |

| June | 4383 | 4534 | 15094 | 16771 | 22.50346563 | 21.28138935 | |

| July | 4205 | 4203 | 10937 | 15624 | 27.77043984 | 21.19836586 | |

| August | 3882 | 4228 | 11082 | 17426 | 25.94226143 | 19.52526092 | |

| Total | 20976 | 19912 | 63804 | 79999 | 24.74168436 | 19.92973747 |

However, LCV contribution is tiny to ALL’s topline. So real impact may not be extra-ordinary to the company’s numbers. LCV might see even higher market share in coming years as they will introduce even more superior products after BS VI transition as planned by management.

Note: TaMo numbers are of SCV segment. TaMo’s numbers of June FY19 & July FY19 are slightly approximated.

Disc: Initiated position in last 90 days. May add more.

4 Likes

Guys,

Anyone in the group what is the best way to know the potential for CV growth in the next few years. Say 3 to 5 years.

This will be the deciding factor, as CV sales are not impacted by Ola and Uber or millennial mindset,which are the major concerns for PV slowdown currently faced.

I want to do a growth projection for the potential for Ashok Leyland, I feel there is a big runway ahead and the stock is at a discount.