APL Apollo Tubes Ltd

Highlights of Q1 FY19 Results

Financials

Revenue grew by 45 % to 1676 Cr yoy

Sales volume grew by 14 % to 3.02 lakhs MTPA yoy

The period saw increase in realisation across the product categories lead by the higher steel price. Company pass on any increase in the steel price directly to the customer Going forward as raw material price stabilize volume movement will increase in the upcoming quarter.

EBITDA grew by 38 % to 108 Cr yoy. EBITDA per ton stood at around 3500 Rs against 3000 Rs last year same quarter.

Interest cost grew by 49 % to 26.3 Cr and it proportionally increase of topline by 45 %. Interest cost as percentage of sale remain stable at 1.6 %.

Key Highlights

Management has increase the Inventory to mitigate the volatility of availability of raw material around the market.

Company was taking raw material from Bhusan steel so there was lot of disruption happen over the April and June . Finally TATA subsidiary has take over it and now it has been stable. Commercial and supply both side are now normal so now supply has become very smooth now.

The technology which company had adopted couple of month back. Almost all of them have become operational . In a year or two year full benefit of that technology will start coming in.

Company production is running smooth now and company now is in talk with the persons for supply Many projects have taken up for Infrastructure, Oil and Gas Refinery.

Q&A

Will company maintain the outlook of 20 % volume growth and how company see the market going forward ?

o In 20 % guidance 5 % plus minus can be there . In first quarter company have achieved 14 % growth as there was some uncertainty and going forward if company will remain to manage 15-20 % annual growth it will be good because company base line is quite high and economy is growing to 6-7 % but infrastructure spending has not come to that much from the government in Metros and others but still company is targeting household sector , solar sector and getting good results. So growth will depend on particularly on the spending of Infrastructure.

How company will maintain the rise in interest cost due to rise in steel prices ?

o If company maintain the EBITDA per ton than interest cost aslo get managed and as volume scale up the interest cost will be managed.

Any update on the compensating of GI plant ?

o Company already have GI plant capacity of 7-8 thousand ton per month and in four GI plant the investment is not so high it is only near to 10 Cr which is coming in Raipur , it will be operational by September. So that will give company a combine capacity of 12-13 thousand ton and at this moment company don’t want to increase capacity beyond that because that will be sufficient to take care of domestic as well as port level. Once company cross 10 thousand ton level than company will think of increasing capacity.

What is the reason for de-growth of volume in current quarter ?

o The plant which was close has only come in month of may so company only got part benefit of the plant coming up and in July - September there can be again some disruption because of rainy season lacks for GI but from October there will be full capacity sitting utilised.

How the steel price has been trending and does company is looking for steel importing as well ?

o International steel prices vary from 600-640 $ . The landed price are equal to domestic prices so there are no arbitrage opportunity.

How company has maintain the high EBITDA per ton for the quarter ?

o There was a rise in raw material prices of 8-10 % and company get benefit of inventory that kept before the quarter of around 200-300 Rs EBITDA per ton.

Does there is demand constraint rather than a supply constraint in the sector ?

o Correct the Infrastructure spend is not as expected but company have a advantage that company produce products which are used in Household, Solar , Hoardings, etc so company is supplying to these sectors . Overall company must be doing 1,00,000 ton per month as it is doing per month .

How is the unorganized market playing out post GST and introduction of E-Way Bill ?

o There has been some impact because shifting from unorganized to organized is slow and it is because some people has move on to organized track of paying GST and producing E-Way bills. But some are not coming to GST platform and not gaining GST benefit and these people will realize that it will not stand for a longer period so they will also shift . Unorganized sector capacity is shifting to organized sector so organized sector is growing fast. There is a shift from Duty awake sector to duty paying sector and competition has reduced to some extent.

Does company is providing discounts to the dealer to get them toward organized market players ?

o No company don’t compromise on margins . Instead of that company is developing other way . So company is working on creating demand specially on that. Company is working on different products like De-galvanized Pipes, BFC technologies . Company growth is coming from GI pipes , GP pipes and from sections which are specifically made for special customers. So volume growth will be coming from these three products and not by giving discounts.

From total volume how much goes to Infrastructure and residential purpose ?

o 85 % of company sales take through dealers and distributors and 6-7 % directly from large customers and another 5-6 % company export. From 85 % going to dealers almost 35 % go to fabricators which are having small demand like household demand , retail demand , commercial demand. Another 25-30 % goes to large suppliers so these are fabricators who take large quarter which could be metro , Household , Commercial Building. Rest 15-20 % goes to equipment manufacturing or advertising boards . So Infrastructure contribute to 25-30 % of company sales. Company is also making special sizes products for infrastructure but they contribute very little for example 3-4 thousand ton in a 1 lakh ton sale and expect it to increase as the infrastructure spend increase.

What is the EBITDA per ton company get in all high end products ?

o EBIDTA is 3300 rs per ton and these special size product can give 30-40 % more EBITDA depending on sizes.

What steps company is taking to maintain the volume growth ?

o Company is spending a lot on campaign and digital campaign is already going on and giving very good response and company is getting queries and orders from digital medium . Company is also coming on the mainline media. So this things company is doing to ensure the volume growth of 15-20 % continuous and also that company margins remains study.

How much capital expenditure company is planning and advertising expense ?

o Company is looking it as very moderate level so company is planning to spend 20-25 Cr per annum to begin with and once the momentum picks up company will increase it. CAPEX will be 50-100 Cr for Galvanized and De-Galvanized segment and company is also working for bringing some kind of backward integration in the materials so that cost of raw material procurement will go down so that facility will be coming this year . So CAPEX is very limited this year

What is the company planning for increase in exports ?

o Earlier because of DFP company was not able to break the US market and previous quarter company had break the US market and now company is looking at Canada also. From the new DFP technology company will grow to new markets and increase Exports from 5-7 % to 8-9 % and EBITDA will be in similar range to domestic.

Is the de-growth of volume is also because of ASP or it is pure because of demand ?

o No ASP has no effect on it. Demand was also steady than issue became in April and May as there was uncertainty in supply because of so much noise of Essar going not going , Bhusan going not going so there is a disruption in supplies for a vary limited period and in limited sizes . So company found it difficult to source from suppliers. So it has effect of 2-3 % in sales. It result in increase of Inventory where company is holding almost 50 days of inventory instead of 35-40 days of normal inventory .

How company see the steel price going forward in the year ?

o There will be a increase of 3-4 % not more than that.

On working capital does company is seeing any collection difficulty ?

o Company is improving . Each month company total debtors has been reducing .

Any progress on SKU ?

o Very good progress company is introducing SKU every week . But these are very specific and customized . So by providing more and more SKU company is getting the presence . On an every month basis company is selling 3000 SKU . Overall company basket is increasing day by day.

Why has the change in the guidance for growth of 20 % to 15-25 % ?

o Sector is growing in 7-9 % and within that growth company is likely to get higher share so on a year on basis it will be 20 % but qoq it may vary . Now the Election year is very close so come of the project may get postpone so it can have some impact but more important than that company base line is increasing yoy. Last year it was X so now it is higher than 20x so baseline effect will also be start coming in time. Despite all this company is targeting 20 % growth in any case.

By how much percentage the organised market growing and what is the company market share in the industry ?

o Company is producing 1.2 million ton and company market estimates between 8 million tons so on that basis company market share is 15-16 %. Organised players are growing at 10 % and unorganised players are growing at 3-5 %.

What is the company distributor or dealers strength ?

o More than 400 distributors and increasing in tier-2 and tier-3 cities.

Kindly give some brief on the initiative that company has taken in backward integration ?

o Basically it is on supply side as company is supplying steel pipes from 1 mm to 10 mm . Standard size is 2.5 mm. Materials below 2 mm are slightly difficult to find . There were period of shortages in area of thinner material. So to take care of both supply issue as well as pricing issue. Company is trying to put some reduction in terms of thickness on how the company can get material so that company don’t have to depend on outsourcing. That will reduce the prices of raw material for company . It will be operational by this year end .

What will be the interest cost for the company going forward ?

o It will be in a range of 20-25 Cr sustainable and company volumes will be only higher so company will be normally operating between 20-25 Cr by the quarter and that level should be maintain.

What production does company see in the year for GI pipes if the new capacity comes in ?

o In GI pipes production was 23,000 in Q1 and this will be between 25-30 thousand in coming quarters. Fourth GI plant will be coming in month of October- December after that company production will go 30,000 ton plus.

What was the holding cost for inventory in the quarter ?

o Company is carrying around 45,000-50,000 ton as inventory so the holding cost will comes to 1.5 % around 600 rs per ton.

How is the channel financing going on ?

o It gradually increasing right now company is doing 100 Cr . Company has started giving cash discounts to customers in which payment is done within 10-15 days of supply. So dealers go for financing so company expect lot of people to go out for channel financing and this scheme is announce recently. So going forward it will increase.

On the DSP side , Is there was any improvement in production ?

o There has been improvement in production , it is marginal but it is improving and that will be on the hollow section side.

What would be the capacity of DSP when total capacity will scale up ?

o DSP should contribute 25 %.

What is the current debt on the books ?

o Around 950 Cr. Company will start reducing debt from now onwards because company have extra inventory also and it will also decrease going forward by 10-15 days .

How is the agriculture demand is trending ? How many distributors company have open and how much touch points it reach ? Which states are growing ahead of 14 % plus volumes ?

o Agriculture use pipes for two purposes one is absorption of underground water and secondly for irrigation. Company is endeavour toward focusing in underground water absorption . In other sector where company pipes are uses like green-houses company is getting very good success. There company will be increasing their presence even further. Forward the growth rates are not very high . Company will only be growing at 5-6 % in that area.

o Volume contribution from agricultural side is not more than 10 %.

o Company have around 400 distributors out of which 50-60 large distributor . They are focused mostly in the large metro cities and than there are small distributors which are in small cities like Rajkot , Kanpur and Baroda. Company presence will increase in Tier-2 and Tier-3 cities. Company has include many new dealers in cities like Jamshedpur , Bhubaneswar . Company need to increase presence in smaller cities because of that loyalty becomes higher . Every year company will add 20-30 new distributors. Each distributor service to around 50-100 retailers. So total 20,000 retailers are there which are connected to company. Growth wise company is getting good growth in the south and now company is focusing on north and east as well in coming quarter.

What is the reason for the stock price being depressed for so long?

The EBITDA margins are going to show an uptrend after DFT completely kicks in.

The company is also living up to its talks of increasing sale of high value products and capacity utilization is also increasing every quarter. Also, lots of brokerage houses now have recommendations on this stock.

Steel prices have been volatile and the company has performed well in passing on the prices. I understand that prices are a function of supply and demand, but there is honestly no change in the story of this stock. I am sure slowdown in the q-o-q revenue growth is not only the reason

Correct me if I have missed any negative information.

If you have the conviction on the stock, please add and sit tight.

If one gets swayed by dips without any sustainable reason, then stock picks are solely based on luck and no hard work.

If I go with a 7 year horizon to value this stock, CMP appears to be pricing in a sales growth of close to 12% and a PAT growth of 15-16%, assuming an exit multiple of 20 at the end of the period.

I am also modelling for a conservative EBITDA/MT of INR 3300, dividend payout of 20% and incremental working capital requirements of 25% of sales

All the above numbers are realistically feasible, in fact base case may turn out to be better than this

At CMP, my calculations tell me that the stock is going at a 10% discount to the intrinsic value. This is never meant to be an accurate or a precise exercise but one does get a sense of the risk/reward for investors at CMP

Disclosure: My largest holding as of now, adding more at every 5% fall

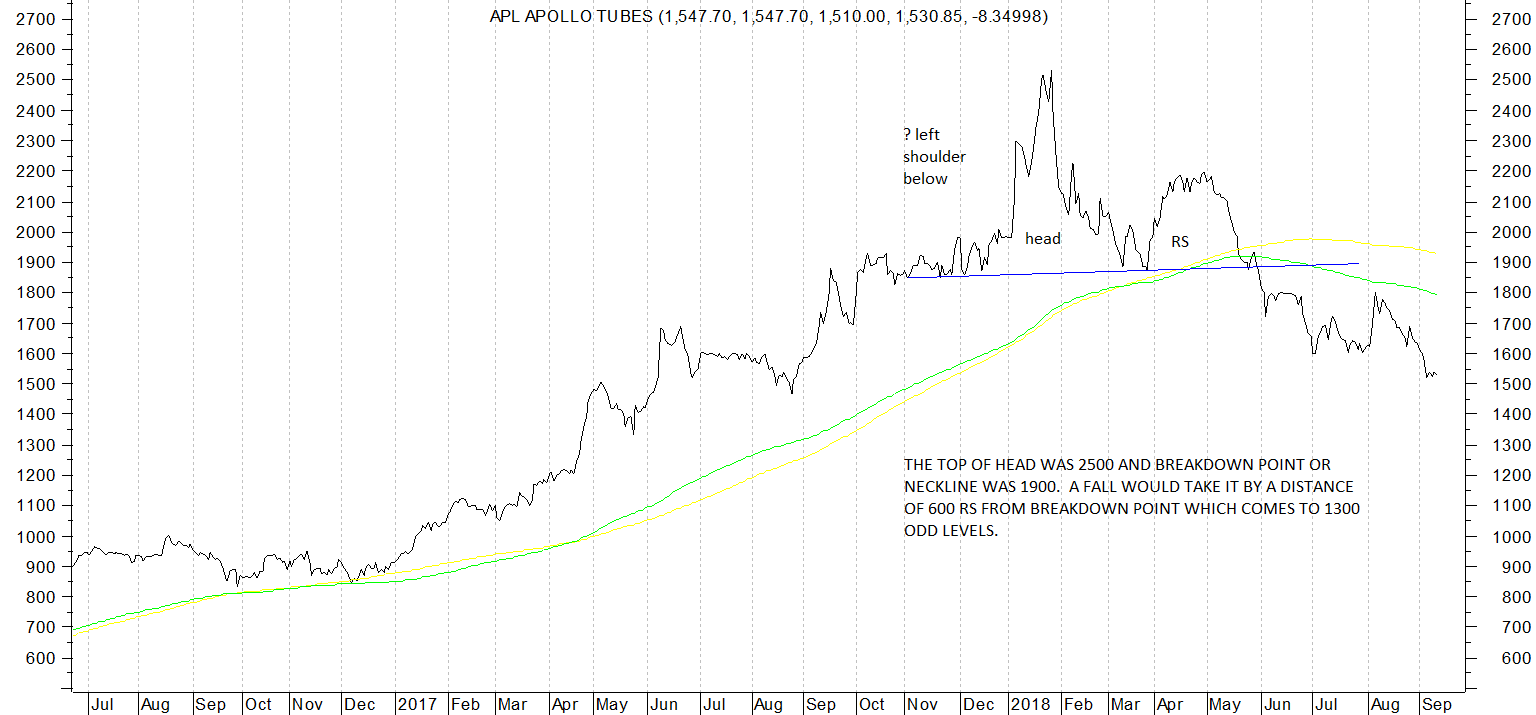

APL Apollo has been churning out very good nos since a long time now. Stock price had a dream run from 880 in Dec 2016, post demonetisation to a high of 2500 plus in the frothy times of Jan 2018 and since then has corrected to current levels of 1530. A correction that happens in a stock that has gone up 3 fold in a matter of 13-14 months is likely to take atleast a decent amount of time. And as can be seen from the attached daily line chart it had formed an atypical head and shoulders pattern whose ultimate target could be 1300 odd. (dont know if it will go down to those low levels as it is a high quality company with a decent track record) Its under my watchlist but the charts at present dont give me enough confidence to venture out a buy. I would first like to see some kind of a signal of strength in the stock price indicating a reversal of downtrend.

Hitesh @hitesh2710, it seems APL Apollo is coming closer to 1300 as you mentioned in your study. Just want to understand, how would you study the signal of strength in the price which would indicate a reversal of the downtrend?

Discussion with Mr. Ashok Kumar Gupta (MD [executive])

GST has benefitted us along with all the organized players.

July had seen de-growth in sales on account of flooding in Kerala and Karnataka along with other parts of the country. Kerala account for 10% of our sales and is the highest contributing state in our overall sales while Karnataka is second highest contributing state in terms of sales. However, sales have recovered in August and September. In fact in September, the company has achieved its highest ever sales for a month.

We have strong presence in GI and structural pipes in India. We are market leaders in them (30 – 35% market share in India in GI and rectangular structural pipes). Surya Roshni has strong presence in GP pipes and we don’t compete much in it as it’s a commoditized market. Even the black round pipe market is commoditized.

Impact of Direct Forming Technology (DFT) – Although the margins of the company haven’t improved because of DFT, we are seeing good growth in customised products manufactured through DFT. We are a reliable and quality supplier of the products we manufacture.

Currently, our capacity is 1.7 – 1.8 million metric tonne (MMT). Post installation of new capacities in Delhi and Hosur in current year, we expect our installed capacity to increase to 1.9 – 2.0 MMT. Normally, a pipe mill runs at 80 – 85% capacity utilisation. Post expansion, our capacity will increase to 2 million MMT by this year’s end.

We are targeting sales growth of 15 – 25% per annum over the next three years. The sales growth will also be dependent on overall economy as well as state of steel industry.

For GI pipes, we are increasing capacity in Raipur where the competition is less compared to other parts of the country.

For section pipe, our price is the highest. Whenever we raise price, other companies follow us. For some of the specific designs in sections like 300 X 300 pipes, we are a dominant player in the market. Using DFT technology, we are introducing new products in the market.

Exports sales in US and Europe have been impacted because of import duties introduced there. Its just been 6 – 8 months since we started in this markets and they are not a major focus area of the company.

GI Pipe expansion to come up in January – February, 2019

There might be some increase in debt of the company on account of increase in inventory due to increase in prices of steel.

The company is setting up a cold rolling mill with a cost of Rs.50 – 70 crore. It will basically use the HR coils from steel companies and convert them. The project will be funded through internal accruals.

Despite take over from Tata Steel, we continue to enjoy healthy relationship with Bhushan Steel. As much as we are dependent on Bhushan, they are also dependent on us as we are one of their biggest customers.

We still have a long way to go in terms of improving efficiency, building team and taking company to the next level of growth. We have three marketing teams – one for trades, one for OEMs and third for exports. In trade segment, we have four regional heads looking after each of the regions. We also need to work on our quality and delivery.

In branding we have plans to spend Rs.20 – 25 crore every year in the medium term while this year we will only be spending Rs.4 – 5 crore. We want focused marketing which is targeted to our customer base. We have even started digital marketing campaign.

Post the floods, the demand has recovered in Kerala. In GP pipes, we recorded highest monthly sales of 25,000 metric tonne (MT) in September.

For dealer finance, 5 – 10% of the business is with recourse to us.

Dealer addition is not much important in our business while effective customer base is more important. However, this year, eastern region will see dealer addition.

We have an agreement with supplier of our DFT machines that they cannot supply machines to any other company for three years. Although, Chinese companies make machines for DFT, they are not of good quality. Chinese companies also manufacture DFT machines but these are not of good quality.

Given our growth plans, we can never be debt free.

Rs.3,400 per tonne is our base EBITDA and we plan to improve that by Rs.100 – 150 per year.

Discussion with Sanjay Gupta, promoter

We plan to significantly grow our EBITDA in next 3 years. We have a definitive plan for this. The major reasons for increase include – increase in production by 20% every year, improvement in profitability through better innovative products and putting up of cold rolling mill.

We have recently hired ex Chairman of SAIL. We are also looking to set up a new HR coil rolling mill at Raipur the cost of which will be Rs.200 crore. The capex will be funded through internal accruals.

The MD was also worried about Bhushan takeover by Tata Steel and that is the reason we loaded up on inventories in June and July. However, our relationship with Bhushan remains intact and we are now getting rates from them which are even lower than JSW Steel.

On the issue of infusing funds in Best Steel, the management said that its a risk that they are taking and didnt want to fund it through APL. They will merge it with APL at appropriate time once they establish the market at the share price at which promoters infused money in Best Steel (they have actually done that now).

Direct forming technology or DFT is good but it is not something so radical which will make conventional method of tube making obsolete. Agreed it does have its advantages but then the scales at which big Indian Tube manufacturers are operating they can copy Chinese tube manufacturing process wherein one mill continuously rolls a single size.

Further I must add that one of the very major tube manufacturer is also starting ultra large diameter tube(bigger than 250x250 size) manufacturing with a tube mill which can roll both Circular as well as Square/Rectangle tubes. Whereas DFT mill can only roll Square & Rectangular tubes.

I am a shareholder of Best steel , Would appreciate any insight on what is exactly happening - APL Apollo buying stake in Best steel through subsidairy . What is the significance and consequence of this move for Best steel minority shareholder prospective

Extensive experience of promoters in pipes industry

Market leadership in ERW pipes segment with consistent enhancement in capacities

3.Expansive manufacturing base with extensive distribution network

4.Diversified product profile

5.Consistent growth in operating income

Healthy debt coverage indicators

7.Comfortable liquidity position

Credit challenges

1.Vulnerability of operating profitability to raw material price movement

2.Intense competition from large as well as unorganised players

3. Profitability remains rang bound

4.Elevated debt levels

5.Relatively low promoter holding