This is a free cash flow business here on, FCF yield is in excess of 6%. Assuming the aggressive expansion continues from here, all capex can easily be funded from internal accruals

Interest as % of sales continues to come down, absolute level of debt has been more or less steady while business continues to grow in double digits. Entire savings here will accrue to the bottom line, PAT margin is in excess of 3% this year

Dividend Payout continues to increase since the balance sheet has gotten much healthier over the past 3-4 years

Continues to be a 16-20% ROCE business with ROE for this year in excess of 20%

I still do not see a worthy competitor to this business, the addressable market size is in excess of 30,000 Cr per annum and growing. APL has shown tremendous financial discipline (for this segment), good execution (ability to expand and capture market share) and the ability to tap into new segments. These are tremendous competitive advantages that will not disappear anytime soon, multiple small factors are working in favour of this story which cannot be understood with a superficial analysis.

Business is valued at 3200 Cr as I type this out, I still see a lot of room for business growth and the valuation will reflect this eventually. Not a no brainer multibagger from current levels though. I am obviously biased in favour of this story but I still cannot find too many loopholes in my initial hypothesis, till then I hold unless the story starts to become obviously overvalued.

Lower taxes helped the company this quarter. Y-o-y comparison will look bad next 2 quarters as margins were high in H1 last year. It sounds like company is pushing sales to increase utilization to keep its new factories running.

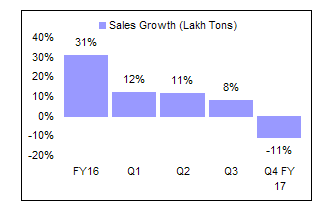

Sales growth is trending down as well but should pick up as Raipur plant will start contributing. biggest worry is valuation. Stock has gone up 70-80% in last 2 quarters and now in the overvalued territory.

Am still gung ho on the long term story but I have too much riding on this (16% of my NW in this stock right now). Taking some money off the table (~ 15% holding) since better opportunities are visible to me at this point of time within my existing portfolio.

From the current levels I would advise some caution for fresh allocation, don’t see too much of margin of safety on offer. To sustain current valuation company will have to turn in 25% and 20% earnings growth over the next 2 years - may happen but the cost of this not happening is high for me given my high allocation

11% volume growth and 25%+ vol growth through July and Aug - that is encouraging, for the capacity increases the company plans to go till 2020 one would expect a volume growth of 15% at the very least. At volume growth of 20% and above the margin of safety in a business like this looks more healthy since a realization drop of 5%+ can be absorbed and still deliver a 12% kind of bottom line growth.

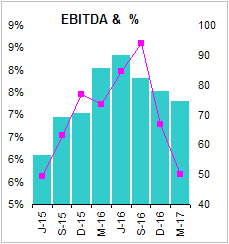

EBITDA margins have reverted to the 8%+/- 0.5% in this quarter. The next 12-18 months are crucial in the sense that the management needs to demonstrate the shift to value added products through incrementally higher and more stable EBITDA profile. If this can happen together while keeping volume growth at 15%+ this looks interesting. Higher PAT over a period is likely to accrue purely due to reducing debt% (not sure if they can meet their target of being debt free by 2020).

If they can deliver 20%+ vol growth over the next 2-3 Q’s, I will be pleasantly surprised and might take the stock price to the next level. The absence of serious competition is the biggest positive for this story, the same story with a couple of serious competitors would not have put the stock price into the current trajectory. The latest AR is a good one, I steadily see the quality of presentations, AR and articulation improve over the past few years. Will continue to monitor this closely

I feel the market has already priced in most of the growth for the next 2-3 years. At 20% volume growth for the next 2 years, company could do volume of about 1.44 million tons. Assuming increased ebitda/ton due to direct forming tech/branding/value added products at 3500 from 3000 this quarter, it can do an ebitda of 500 crs and a PAT of 270 crs. 15 times 2 year forward earnings(in a bull case scenario) is very expensive for a commodity company.

Honestly i dont see debt levels coming down drastically due to working capital requirements. However, interest costs should reduce due to rating upgrade.

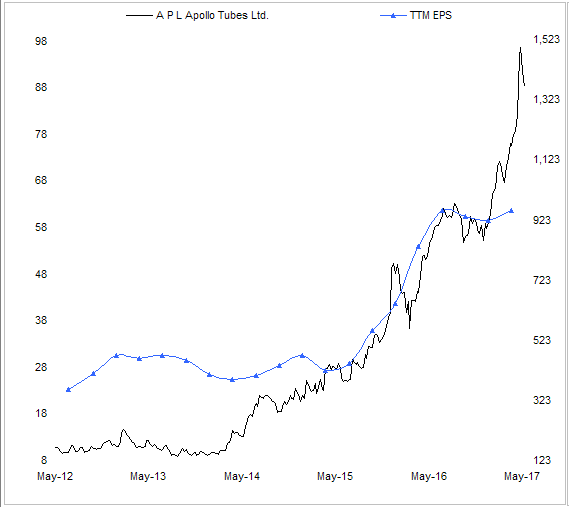

This is the single biggest reason why many people have stayed away from this stock. When I look back at when I invested (articulated to some extent earlier in this thread), I probably spent the longest amount of time pondering over this. Once I took a relook at some of the hard numbers the answer was apparent to me then (undervaluation in my opinion at 11 PE helped) -

Large player in a segment with 30,000 Cr market size and growing at 7-8%

Company growing volumes at 25%+ over a multi year period profitably and hardly accounting for 10% market share

Very low rate of new player entry

Existing competition concentrating elsewhere - Tata tubes has not expanded capacity since 2011, Surya Roshni scaling up the electrical good business

A management that has managed to walk the fine line between being aggressive yet maintaining financial discipline (D/E never crossed 1.2 though the company was acquisition heavy then)

Clear relative scale and distribution advantages over competition

Adjust these positives for lack of pricing power and volatile commodity prices. At 25%+ volume growth the margin of safety was huge and even at current price there is some margin of safety at 20% volume growth.

I think the reason the company is trading at valuations never seen before for this segment is because the market has come to the view that the multi year growth story will continue even if this hits a couple of speed bumps along the way. Market position of the company is unlikely to get weaker anytime soon, if anything it has only gotten stronger over the past 3-4 years. Stock market view of a story also changes for the better when the company demonstrates the ability to be FCF positive and can expand at will to capture a growing market. Healthy FCF combined with medium to high reinvestment rates in a growing market with minimal competition can make for a very good investment thesis even if the return ratios aren’t exemplary and the company deals with commodity products.

I agree that investing right now is a tricky decision to make given that some (if not all) of the positives are priced in.Investing in this now will call for a lot of qualitative thinking and the ability to breakdown the valuation into what scenario is being priced in over the next 5-8 years.

Emkay has joined the list of research firms/brokerages bullish on APL, this by far is the most bullish I’ve seen so far. The most important takeaway from the report for me is this statement - “The stock should not be seen as a steel sector play but as a bet on India’s construction/infrastructure/agriculture push”, kind of reiterates my view on why the quality of this business is higher than what appears at first sight.

Does not change my thought process too much on this, just that I am more certain that this business will eventually make the jump to being valued as a mid cap over the medium term.

Do your own due diligence on whether the business prospects justify the current valuation

Ebitda per ton was 3400 . Likely to maintain this level.

Interest cost was higher due to higher inventory.

Demand is growing at 8-9% per annum. South and west markets doing well. East is driving growth. North is slow.

Targeting 11.5 lac ton sale for the year. Expect 20% growth for the full year. Looking at 20% growth for FY19 and 20.

Currently exports are 7-8% of sales. We are targeting 15% sales from exports.

Currently branding and marketing was only done in Kerela. Full scale branding should start by March.

4 DFT lines have been commissioned. Getting repeat orders for DFT products. Have seen increase in export inquiries from middle east for DFT products. In DFT for the same products sizes Ebitda per ton is same. However, for customized sizes there is significantly higher ebitda (eg 300*300).

Sectors that are driving growth for OEMs - Solar and Pre engineered buildings. Agri and Auto will take time.

In line galvanizing lines to be commissioned by Q1FY19.

Nicely drafted! Did you looked at the scenario post the expansion plan which the company has indicated. DFT is a new technology which company is bringing in and this will improve 10% margin over their 400 products under offering. I was going by one of the latest report from DBS where in they have given target of 2812. I see if the top line grow even faster over a period of time then valuation may become attractive. It has already rallied quite high. Now i also think it doesnt offer margin of safety.

Have a lot of time on my hands this week to revisit my valuation models. Did this for APL today and was pleasantly surprised

My model tells me that APL might become debt free in 2021/2022 even at conservative assumptions. On a rudimentary P/E basis the stock looks fully priced in now but once I keyed in the numbers in my model, looks like the price is only fair and nowhere close to being richly valued.

I think the big change over the past 2-3 years has been that the company has transitioned into a free cash flow engine from a company that needed debt to expand capacity. This single change has the potential to transform all valuation metrics for a company and I have seen enough examples in the Indian context where the valuation accorded to a free cash company is in a different league altogether. Risk is that I maybe going too technical here to come to this conclusion (the average investor does not look at companies through the same same technical lens) but I am confident enough to stick to my guns on this one. An FCF company looks way cheaper in a DCF that it does on a P/E basis, this may likely be the case with APL as well.

CMP appears to be discounting a 20% kind of vol growth over the next 2-3 years and then a 15% kind of a number over the next 5-6 years or so. These are achievable given the industry dynamics and the infra related investment one expects to see in India over the next 8-10 years. This after assuming that EBITDA per ton stays in the current range, interest rates (and hence cost of capital) will trend higher and that the exit multiple will be hygienic at 20. There are enough levers towards positive surprises that aren’t low probability events and can materialize.

I would not be surprised if the dividend payout 7-8 years from now will more or less be equal to the current operating PAT number. Unless we see a massive fall in commodity prices again with APL taking inventory losses, I do not see too many scenarios which can upset the current growth path as long as competition continues to have other priorities. Long story short, I am not selling out anytime soon.

Disclaimer: Please adjust for my obvious bullishness on this, this constitutes a large part of my portfolio right and now and is likely to stay that way. I am not a SEBI registered advisor and this only conveys my opinion since this is a holding of mine. Do your own due diligence on this.

Volume growth guidance: APL Apollo has maintained its volume growth guidance of 20% CAGR over coming years. Further, in 9mFY18, the company has posted volume growth of 19% YoY and is confident of achieving its guidance in FY18. Further, exports will account for 15% of sales by FY20 compared to 5% currently. Exports also entail higher realisations compared to the domestic business.

EBITDA per tonne: The company is seeing high demand for steel pipes even when steel prices continue to be high. It generally passes on the raw material cost fluctuation within a week and expects EBITDA per tonne to hover around INR3,300-3,400, plus minus INR200-300.

First company to introduce DFT: APL Apollo is the first company in India to introduce direct forming technology (DFT). The company in Q3FY18 has already installed six lines of DFT technology and more two lines are likely to be installed in the next two-three months. The company has a three-year exclusivity contract with the DFT technology provider. Through DFT, the company will further solidify its position in

the structural pipes and tubes segment since it will not only offer more customised options, but also significantly cut the lead time to complete customised orders in comparison to the industry. Further, management remains focused on familiarising rising number of clients with the product the technology can offer and thus will focus on providing advanced customised products at similar prices and margins as earlier

and will benefit from higher margins in the long run.

JV called off with Japanese company Daiwa: Recently, the company has called off a joint venture with a Japanese company Daiwa as it restricted APL Apollo’s marketing geography spread. This is not expected to materially impact company’s performance as the intended JV was expected to account for marginal, around 3%, of current sales

Focus on branding: Management envisages increasing adoption of steel pipes and tubes in place of wooden structures. Hence, according to the management going forward APL Apollo as a brand will play a key role in the company’s growth. Towards this end, management has guided for expense of INR250mn in the coming year. The specified spend will be utilised to propagate the following brands - Apollo Costguard,

Apollo Fabritech, Apollo Agritech and Apollo Bheem.

This is from the SageOne Investor Memo May 2018 by Samit Vartak… Good business insights…

In steel industry, some manufacturers are converters. They buy steel from the integrated players and the value addition is very low. One of the companies I have studied is in structural pipes manufacturing for multiple industries. Their raw material cost is ~ 85% of sales and net margins are barely 3-5%, but they have shown the ability to pass on increase in raw material prices to the consumer and thereby protecting their profit/ton. Even in the steel down cycle when many integrated players were going bankrupt, they continued taking market share which translated into profit growth.

When margins are so thin, even small incremental advantages create a huge differentiating factor.

This company because of its economies of scale and timely payments could negotiate raw material prices 0.25-0.5% lower.

Their strong balance sheet enabled them to get working capital loans at rates 100-200 bps better than the competitors.

Their plant locations and distribution network enabled quicker delivery to the retailers across India.

Because of their strong balance sheet, they invested in doubling capacity with newer and more efficient machinery. This not only lowered their cost of production but also reduced their changeover time between batches from 24-48 hours to 2-4 hours. They could cater to smaller and more profitable orders.

Management was always on top of launching new value added products for newer industries thereby expanding the market in addition to gaining market share.

The combined savings could be just 2-3% of sales, but in this context the profitability differential is huge. With this ability, they can lower prices and drive the competition out. When they lower net margins from 5% to 3%, competition is breaking even. Such competition can’t afford to play or won’t want to play. Individually many of the above advantages could be replicated, but when you consider the balance sheet of the competitors, economies of scale and their management quality it is very difficult to replicate the combined advantage.

This company during the last 5 years of tough steel cycle tripled its top-line as well as bottomline.

My views on the story and why it makes for a good investment already elaborated in multiple posts on this thread.

Though this is by far the biggest holding in my portfolio right now, I just could not help adding more at current levels. I think at a price of 1700 and below the risk reward is hugely in favor investors though one cannot quantitatively establish this based on simple valuation metrics.

Conviction means nothing if one does not act when the odds are in your favor, so here I am buying more if this falls lower