Hi,

Is there already a section describing how to analyze balance sheets?

Thanks!

Hi,

Is there already a section describing how to analyze balance sheets?

Thanks!

Thanks for raising this. Guess this is a common question for those wanting to bring some rigour into how they analyse a company’s stock.

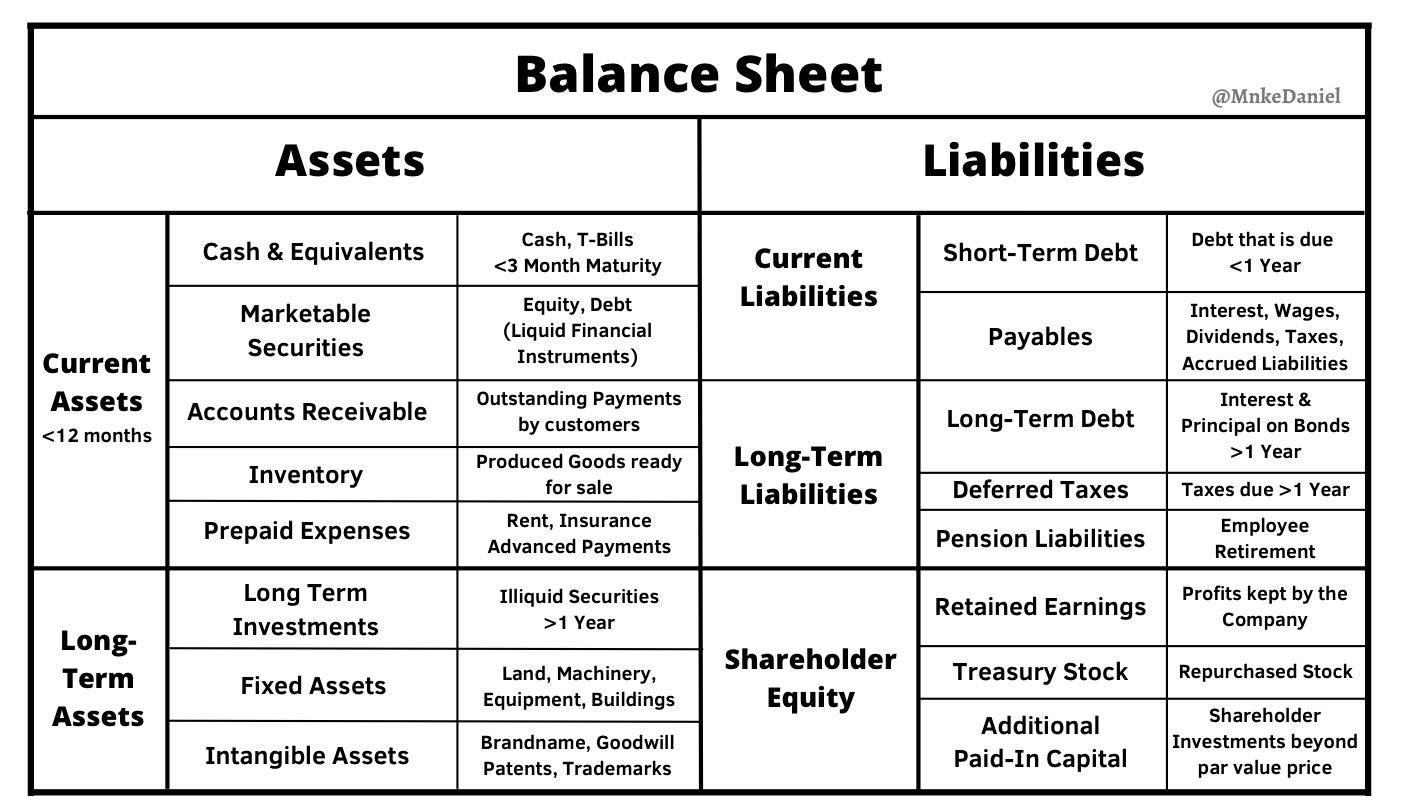

You will find an excellent starting place Stock Analysis Framework -a rigorous, step-by-step complete do it yourself package right here at ValuePickr!. See also Stock Valuation Framework.

If you are looking for specifics only on Balance Sheet analysis, perhaps you can jump straight to checking the Financial Health section.

Go through these and let us know your feedback. If you find these useful, perhaps many others would too!

this link is very helpful. THans

Can someone tell me why this difference in same year’ balance sheet published in two Annual Reports.

https://docs.google.com/file/d/0BxHCrqYP02M8b05yQUhTMjI2RlU/edit?usp=sharing

They would have published any explanations on this?

AVOIDING LANDMINES IN INDIAN MARKET

The Indian stock market, in aggregate, carries a relatively high risk that a minority shareholder will not realize the value in a listed firm because the controlling shareholder (or promoter as they are known in India) will appropriate value for himself, leaving little on the table. The risk is higher relative to certain other stock markets mainly because of limited regulation. In addition, lax enforcement indirectly encourages such behavior.

However that does not mean all firms can be painted with the same brush. There are many firms that take shareholder obligations seriously in letter and spirit irrespective of size, industry or geography. Notwithstanding this, there is an added burden for an analyst examining Indian markets, who not only has to figure out an undervalued business, but also has to be confident in his assessment that the value will not be misappropriated by the promoter. An imaginary 10th edition of Security Analysis would have provided us with the analytical tools to give some cues; sadly, now we have to develop our own.

A commonly observed technique among analysts is to meet management and/or the promoters. But I know that a promoter knows to put up an act to near perfection. It is only on rare occasions that they do not succeed in painting a future more glorious than the present or the past. Therefore, I am always left doubting my ability to confidently assess promoters through an interaction, and prefer more analytical approaches to the problem. The purpose of this write-up is to provide some analytical starting points on potential investment candidates to weigh this risk. This article may be considered more an initial attempt than any comprehensive statement on the subject.

âYou Are Right Because Your Facts Are Right and Your Reasoning Is Rightâ

Every annual report talks about the companyâs dedication to shareholders and the highest standards of corporate governance it embraces. This included a company that was part of Indiaâs leading index â Nifty. This company had just won a prestigious global award for corporate governance and had on its board an Ivy League professor, someone âwho also co-led Corporate Governance, Leadership, and Values initiative, launched in response to the recent wave of corporate scandals and governance failuresâ. Soon after the financial crisis emerged in 2008, the promoter of this company confessed to perpetrating the largest and the longest accounting fraud in India.

In other words, a better assessment can be obtained not by how the promoter dressed up the company, but by how well he resisted the temptation to put the companyâs money into his own wallet. If such temptations were resisted in the past, itâs likely to be the case in the future as well. The best way to assess that would be to look into the companyâs past, and the promoterâs behavior in relation to the company. If there have been actions in the past that appear intended to benefit the promoter at the cost of other capital stakeholders, we can conclude that there is a non-trivial risk of misappropriation.

And much like what Warren Buffett said about not playing the Russian roulette even if there were a million chambers and all empty except one; whatever the payoff, we avoid the firm. The absence of such promoter behavior would also give us sufficient confidence. In addition, the longer the past under observation, the wider the set of circumstances. There would have been more opportunities for misappropriation, more good times and bad times to influence the promoter and hence a more reliable guide. I propose a window of 10-15 years for the proper assessment of such behavior.

How to Detect Instances of Misappropriation

The analyst starts by looking at publicly available statutory documents beginning with the annual reports. An analysis of this report is subject to the integrity of the auditor certifying the accounts. That would decide if the company is worth analyzing at all. I know of no easy process that will determine with confidence the answer to this question but experience does help. However our analysis is predicated on credible books of accounts.

The analyst then keeps looking for transactions that give any indication of misappropriation. An analyst experienced with poring over many such transactions will identify a set of broad transactions that have come to be âaccepted waysâ of doing such business. Sharing such a list will be useful to the investing community and that is what follows below.

Broadly, misappropriation transactions can happen in ways that have an impact either on the profit and loss statement or on the balance sheet alone. Transactions affecting the former will have the impact of immediately depressing the return on equity, but they are difficult to deduce from audited accounts. Transactions affecting the latter are easier to recognize, though they have permanent damage. Sometimes, the misappropriations can get fatal to an unsuspecting shareholder.

Table 1: Examples of Misappropriation Impacting the Profit and Loss Statement

Examples of Misappropriation Transactions

1)Under invoicing of product to the distribution channel. The channel sells the product to the customer at market rates. The channel keeps a fixed margin and remits the remaining as follows: a. the invoiced amount to the company and b. balance to the promoterâs account. Thus the company realizes a lower amount for every product sold which is transferred to the promoter.

2.)Seek over invoiced amounts from vendors to the company.The modus operandi is to pay the over invoiced amount to the vendor, part of which is then paid back as cash to the promoter. This has the twin advantages to the promoter of reducing tax expense in the listed firm and meeting cash expenses in his personal accounts.

3.Having dummy employees on payroll with their bank accounts controlled by the promoter. So the salaries get credited into their accounts (kept at a level to create no tax liability for the dummy employees). This creates a tax deductible expense in the company.

4.A more audacious mechanism observed is to âdevelop intangible assetsâ by capitalizing expenses. These intangible assets are amortized over a period of 4 â 5 years.

5.Write-offs of bad debts, Sundry balances written off. Self-explanatory.

The above transactions are consistent and done in a routine manner, and I find it difficult to confidently deduce this (except 4) conclusively from the audited accounts. In Table 2 below, we see transactions that impact items on the balance sheet. A wider variety of techniques employed by promoters can be better understood when viewed from the balance sheet of the company. These can be one time or ongoing and range from the simple to the bizarre. While the audited accounts presented in the annual report provide a good starting point, they may not reveal the complete picture; especially if the firm carries large debt.

Table 2: Examples of Misappropriation Impacting the Balance Sheet

Examples of Misappropriation Transactions

Inflating receivables and inventory to seek higher working capital limits for funding by banks and subsequently taken out to settle âcreditorsâ.Banksâ main source of corporate credit is working capital finance; the size of which depends on the working capital needs of the firm, so firms inflate their working capital to be able to draw more from the bank.

Paying for promoterâs other business misadventures.Promoters typically have privately owned businesses other than the listed entity and not all businesses do well. Typically promoters will want to enter a new growth area setting up a new business with the intent of roping in investors when âvalueâ has been built. The business would have been heavily leveraged and the promoters soon find they canât rope more investors. The funds of the listed entity would then seem handy and a scheme would be devised that would effectively stick this promoter owned capital sucking entity with the listed company via âschemes of amalgamationâ. This would entail issuing fresh shares of the listed entity to the promoter for buying out this high growth business the promoter has created. The valuation would be arrived at by an âindependentâ valuer and approved by Independent Directors. Ownership of the listed entity by the promoter would increase and the listed entity is stuck with an unwanted business (typically as a step-down subsidiary).

Taking cash out of the listed company that has just sold of a part of its business.In recent times many listed entities have sold off their business divisions to large foreign firms in a manner called as slump sale, where the division assets and liabilities are transferred and the remaining entity continues as it is. This acquisition route is preferred by large global businesses entering India, for various reasons. A slump sale takes a business division out of a company and leaves cash in the company. The promoter would want to keep the cash either with himself or with the company but not part with it. This cash comes out of the company and to him through ânew and promisingâ initiatives that the company now wants to deploy the cash in and set up subsidiaries where this is funneled. In some cases, remaining businesses âare given a boostâ by providing heavy cash incentives to the customers, and quite unsurprisingly these cash incentives do not work (because they flow back to the promoter) and the firm books heavy losses.

Raise loans for their promotersâ private ventures by providing the listed entityâs assets as collateral.Some promoters want to create new businesses, for themselves, without much of their personal funds. They would need the funds of the listed entity without the attendant shareholders â so how to manage that? Raise loans for their new ventures by providing the listed entityâs assets as collateral. In one instance loans soured resulting in claims on the assets that took shareholders completely by surprise. The price of the firm has fallen by 95% in the past one year.

Raising promoter stake in the listed firm without any funds.Sometimes promoters want to raise their stake in a listed entity but do not want to pay for increasing their stake. To get around this they would float another company, get it valued by âan independent valuerâ, including for intangibles like âcustomer contact valuationsâ and get the firm merged with the listed entity at a valuation with a stock swap, issuing shares of the listed entity to the promoters as a consideration for acquiring the firm. Itâs that simple! There are also other routes to raise their holding. Take a long term advance from the listed entity in a manner that avoids reporting under related party transactions; use these funds to buy the shares of the entity and over a period of time write-off the advance as bad debts!

Restructuring family holdings in multiple listed entities resulting in cash of the company transferred to a few promoters based on an undisclosed arrangement.As promoter families get larger they want to streamline their individual holdings in âfamily assetsâ, i.e. various listed entities (say A, B, C). Through a âscheme of demergerâ relevant assets and cash is taken from one listed entity (A) and a new listed entity is created (A1). This listed de-merged entity A1 would have the cash and the shares of another listed entity (B) whose control is to be transferred to a family member. A shareholder may not suspect that the cash in A1 will soon disappear to buy out the stake of other family members in B. While this arrangement is known to the family members it is not shared with other shareholders.

Create bogus revenues, along with real ones, use leverage as mentioned in 1 above, show higher returns on equity and continue this cycle till an unsecured convertible debt or equity is raised. Subsequently funnel the money away and let the business collapse. Along the way, dress up the business with well known Independent Directors, hire known industry experts. A firm managed to get its valuation primed to over $ 500 million just before it raised convertible debt. It is now valued less than $ 5 million.

Recently, a dramatic case of misappropriation came to light. A listed entity mired in debt reported that its equity has been wiped out by ârobberyâ of the firmâs assets. It reported that â The miscreants has (sic) looted the factory and taken away critical machineries (sic), raw materials and finished goods and several documents were destroyed.â This led to a dramatic reduction in fixed assets and inventories and wiped out the companyâs equity.

Conclusion

To conclude, these are some popular means adopted by promoters to appropriate funds of the company. Some of the more commonly observed ones are shared in this article for the benefit of analysts, but this is by no means exhaustive. The recent economic slowdown in India has taken the bargain cloak off many such listed entities revealing only liabilities and no assets inside. And in that sense, it has been quite educational!

Vivek - Thanks for the article. When copying/quoting articles or blogposts and even news items/analyst reports, due credit must be given to authors.

Please provide the relevant link(s)/author credits and ensure this is adhered to in future as well. ValuePickr prides itself in providing due credits and ensuring there is no violation of Intellectual Property (IP) of others from the larger Investment Community.

Rather, if we see good content anywhere, we must endeavour to promote that within the community. Provide the links - the readership will decide for itself.

http://www.beyondproxy.com/author/kimi-venkataraman/

Noticed first in a blog got the details subsequently.

Indian companies will have to present IFRS converged (Ind AS) financials. Over 350 companies would be applying these standards from fy-17. Thus as per my understanding first quarter results would be as per new sets of standard. Also Opening Balance Sheet would be impacted by these standards. Motilal Oswal has presented a note which analyses impacts of these standards on the companies. I have attached the same here. Hope it will be useful for the members.

Also would request the members to share the literature if any available with them.

Thanks

INDIA-AS-20160323-MOSL-SU-PG100.pdf (2.9 MB)