Thank you. Yes, reading again it mentions in the fine print that these are all plastics faucets.

Still point being, from being a PVC / CPVC pipe manufacturer, they are getting in to bathroom fittings. Are they going to manufacture it or simply buy and brand it as APL Apollo ? These should require a different expertise and set up to manufacture vs a pipe. What’s the rationale?

Chrome plated plastic faucet market is dominated by Chinese and unorganized see sectors. There is no moat . People who afford good faucet they always go for metal as plastic in bathroom is considered as cheap status

1 Like

Trying to find its dealers and presence in retail. Cannot locate in UP. Major cities not covered. Any idea/update on it?

Apollo pipes Q3 results show top line growth of 16% and net profit increasing from 4.5 to 5.3 Cr mainly led by other income.(without other income of 3.4 cr nos does not look impressive).

| Particulars(Crs.) | Q3FY19 | Q3FY18 | Y-0-Y Change | 9MFY19 | 9MFY18 | Y-0-Y Change |

|---|---|---|---|---|---|---|

| Income from operation | 87 | 74.7 | 16 | 272 | 219 | 24 |

| raw materials | 65 | 53.7 | 21 | 202 | 157 | 29 |

| total expenses | 83 | 68.4 | 21 | 255 | 204 | 25 |

| PBT | 4 | 6.3 | -37 | 17 | 15 | 13 |

| PBT Margin% | 4.6 | 8.4 | -45 | 6.3 | 6.8 | -9 |

| other Income | 3.4 | 0.9 | 278 | 9 | 2 | 350 |

| PBT+OTHER INCOME | 7.4 | 7.2 | 26 | 17 | ||

| Tax expense | 2.2 | 2.7 | -19 | 7.8 | 6.3 | 24 |

| PAT | 5.2 | 4.5 | 16 | 18.2 | 10.7 | 70 |

| EPS | 4.4 | 4 | 10 | 15.5 | 9 | 72 |

| sales volume(MT) | 9300 | 8934 | 4 | 30210 | 25061 | 21 |

| revenue/MT | 93,548 | 83,613 | 12 | 90,036 | 87,386 | 3 |

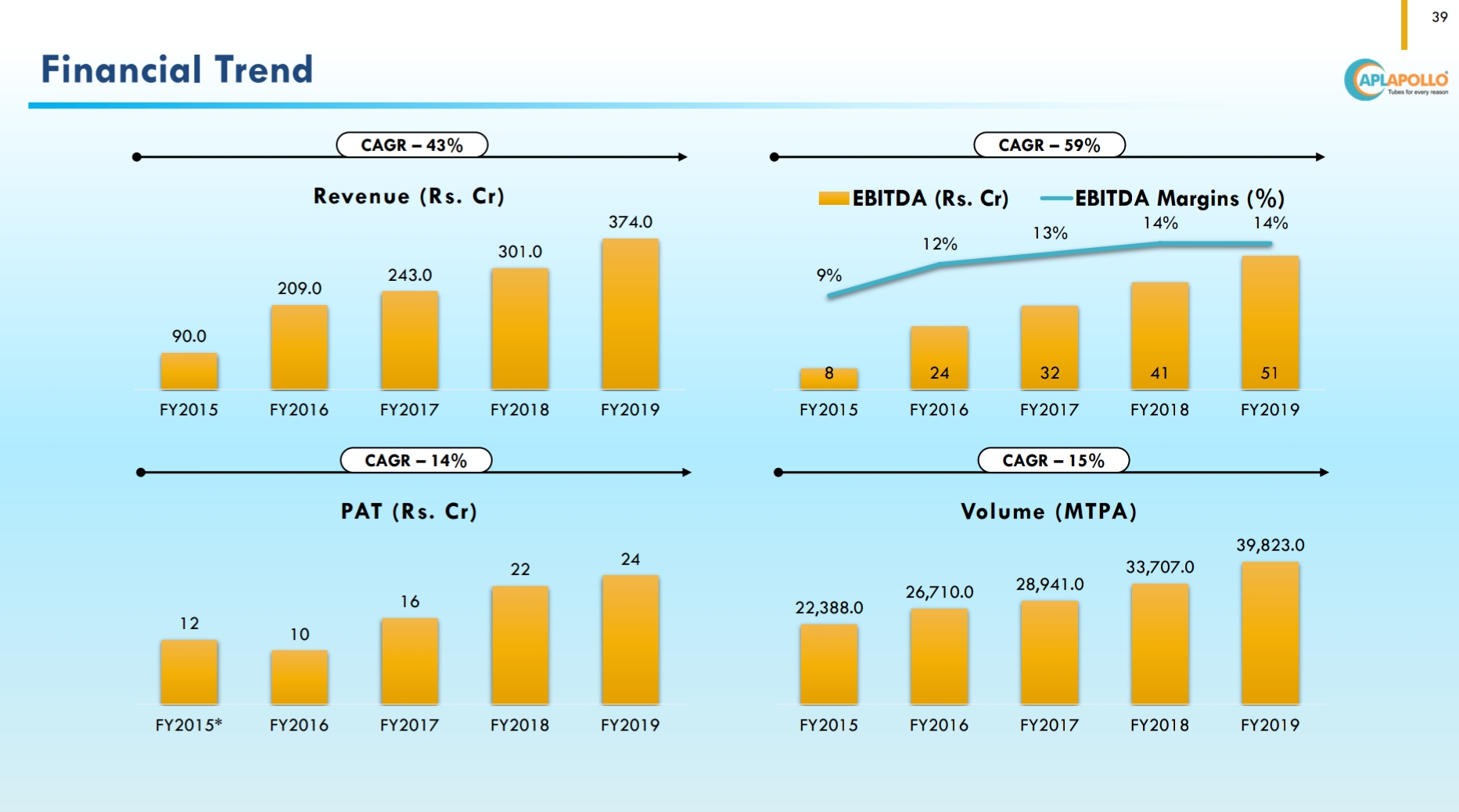

Greenfield capacity of 15,000MTPA at Raipur by December 2019 to expand footprint in central and western India.

25,000MTPA of capcity at Bengalurru by March 2020 to cater to southern market.

Total target capcity of 116,000MTPA by2020.

Launched new product portfolio of plastic taps,faucets and accessories.

Focus on increasing revenue contribution from fitings to 15% by FY2020(from 11%)

Q3FY19 PRESENTATION.pdf (2.5 MB)

6 Likes

I believe they have annual capacity of 70000MT. Utilization is roughly half of that. Any specific reason for this?

For whatever it’s worth, but Catamaran ( Narayan Murthy fund ) and Vallabh bhansali exited from the company during Dec quarter. Or may have reduced the holding to less than 1%

Finolex and Astryl both reported subdued vol growth in Q3. Management commentary was suggesting difficult quarter which traditionally is not the case in agri sector. Weak demand due to tight liquidity. Jan and Feb so far have shown decent demand and they feel it will normalize as liquidity comes back to system. Overall both management sounded bullish over long term but cautious/ bearish in short term.

Equity dilution has happened so the number shares must have remained same but in percentage terms numbers have gone down from threshold 1. This is my explanation for u.

Have great respect for Summet Nagar and his approach towards investing. As an investor in Apollo Pipes, its always frightening to listen to capex plans of Astral and Supreme each quarter. Take comfort from the small base, decent management quality and low cost manufacturing skills of the group. Also hope that the remaining ~145crs are converted at 590/s and are well allocated.

A few questions :

- Why was the Blore plan postponed while Raipur is now coming before Blore ? Astral too is coming up in the East.

- How long will it take for the company to completely utilize the proceeds received back in Jan’18 ? 1H19 results suggests external debt has been added, does this mean the remaining cash will be converted into equity soon and deployed towards capex ?

- Cash-n-carry model will alleviate working capital needs but whats the hit on the margin in a commoditised business ?

An increasing capacity utilization + growing fixed asset base + a slow move towards light working capital structure can do wonders.

But where are the margins ?

2 Likes

I am actually happy that the management has decided to defer the capex plan. When they are hardly doing 45000 MT per annum, what is the point in taking capacity to 150,000 MT by 2020? I’d rather have the cash sit on books and make other income rather than get stuck in fixed assets and depreciate till they get to respectable capacity utilization. My base case has always been that capex will end up being much slower than what management is projecting.

The central hypothesis for me is industry leading volume growth - maybe at lower margins than leaders for a while till they generate enough traction with the channel. Finolex Ind volumes actually went down YoY for Q3, Astral did lower growth than their usual rate. In such a scenario 15% volume growth is pretty good. If the volume growth starts falling I will need to revisit this, then you are just left with a me too business selling PVC pipes.

Part of the debt on books is an overdraft against the FD in which the 202 Cr raised has been parked. Q2 saw the working capital cycle get elongated - mostly due to the company pushing inventory at higher margins to the channel.

Recent margins are lower due to - lower gross margins in Q2 and Q3, higher employee cost and other expenses as % of sales. The latter two are to be expected till the time the new plant starts doing healthier utilization, then the overheads just get spread over higher sales and EBITDA will come back to the normal range. Gross margins should get better with product mix and higher volumes over time, Prince Pipes does a gross margin of 31-32% at more than 2X the volumes so one might expect that over the next 3-4 years.

Let’s see if they can continue the industry leading growth rate, this is a story where you enter and wait for the market to excited over the high growth rate and for the story to get priced accordingly. My sense is doubling of PAT is possible over 3-4 years which is enough for the market to get excited, once the volume per year crosses 100,000 MT growing at 2X industry rate won’t be that easy and the growth will need to taper down.

Disclosure: I am a SEBI registered investment adviser and hold this in my portfolio and customer portfolios under advise. I have added to my allocation in the past month and may add more depending on the market condition

16 Likes

Apollo pipes topline for the quarter grew by 20% and for year by 23%. PBT margins without other income come down further for the quarter and year.

Fixed assets increased to 95 cr + WIP of 12 cr

Total equity increased to 229 Cr with promoters completing infusion of 202 Cr.(out of 2,485,000 warrants, 1,125,000 have been converted to equity shares on 2nd April 2019.Thank you @tejassavani for highlighting this)

Received positive response from market for product portfolio of plastic taps,showers,faucets launched in Q3. company is targeting market share gain in this high margin product category.

Aquisition of production unit (near Benagluru) which is spread over 7 acre with manufacturing line for uPVC and cPVC with space for future expansion.

Phase wise capacity expansion at Dadri by 7,000 tons. Ahmedabad to be expanded by 5,000 tons.

| Particulars(Crs.) | Q4FY19 | Q4FY18 | Y-0-Y Change | FY19 | FY18 | Y-0-Y Change |

|---|---|---|---|---|---|---|

| Income from operation | 89 | 74 | 20 | 361 | 293 | 23 |

| raw materials | 65 | 52 | 25 | 267 | 209 | 28 |

| employee expense | 4.4 | 3.7 | 19 | 17 | 14 | 21 |

| others expenses | 10 | 9 | 11 | 43 | 35 | 23 |

| total expenses | 83 | 66 | 26 | 338 | 270 | 25 |

| PBT | 6 | 8 | -25 | 23 | 23 | 0 |

| PBT Margin% | 6.7 | 10.8 | -38 | 6.4 | 7.8 | -19 |

| other Income | 2.9 | 6 | -52 | 12 | 8 | 50 |

| PAT | 5.3 | 12.2 | -57 | 23.4 | 22 | 6 |

| EPS | 4.4 | 10.8 | -59 | 17 | 20 | -15 |

| sales volume(MTPA) | 9613 | 8646 | 11 | 39823 | 33707 | 18 |

| revenue/MTPA | 92,582 | 83,613 | 11 | 90,651 | 86,925 | 4 |

5881719f-1c4b-4f31-b03d-a8e128fb97cf.pdf (422.4 KB)

3 Likes

Decent presentation this time.

Targeting 30% volume growth.

Dividend first time.

Concall first time 30th May.

3 Likes

I’m sorry but i think there are some anomalies in the above posts:

“Total equity increased to 229 Cr with promoters completing infusion of 202 Cr”. 1.36m worth of warrants are not converted to equity yet and thus are not a part of current BV. Also warrants converted on April 2, 2019 are excluded from the total equity value. Maybe wrong but Including the total 202cr infusion, total equity or BV will be ~340cr after adding Q4FY19 profit.

Targeted vol growth is 25% over 5 years and not 30%.

Few negatives observed:

- Even after accounting for drop in of interest income, Q4 PAT has dropped substantially considering the growth in volumes. Stress seen in all large players Astral, Supreme and yesterday’s result by Finolex.

- FY20 capacity plans have gone through a lot of changes since the 202cr funding raised early last year and now stands at 90k mpta (down from 150 to 116 to 90). Though no capex is better than ideal capacity.

- Available capacity reduced from 70mpta(Q3FY19) to 63mpta (Q4FY19), not sure how this is possible?

- Even if margins and growth come back, i m not sure how the business will justify a 200cr equity addition/dilution at least for the new few years.

- a 7 acre facility in Blore but no info about the base capacity provided.

Positives:

- Looks cheap when we consider the M.cap/Fully converted BV and compare it to expected ROE at higher capacity utilization

- Cycle may turn positive in 6-12 months.

- Blore plant may provide better ROI than a green field investment.

3 Likes

30% volume growth is for this year. Mentioned in presentation.

Lot of discussion happened here about the capacity plans. Hopefully some sanity from the management.

1 Like

The negatives -

-

Struggling to deliver industry leading volume growth, 11% for Q4 is well below par given the lofty talk of 25% volume growth from here. On an annual basis 18% is still industry leading growth but on a low base of < 40,000 MT they have to deliver more.

-

Fall in Gross Margins might be seasonal given the way prices have been fluctuating, but they have to get to a level of 30% and above. I doubt how they can preserve margins while chasing 25% volume growth, core EBITDA is low - other income is propping up EBITDA for FY19. On an operating basis FY19 has been a bad year, revenue is up 20% but PAT lagging behind since gross margins have fallen YoY

-

How does capacity number suddenly change to 63,000 MT from 70,000 MT? Goal post on capacity has been changing, so have been the expansion plans

The positives -

-

Focus on bringing down receivables is good, they keep mentioning about the cash and carry model which so far only Finolex has been able to pull off. We need to ask more questions on this on the conf call

-

Sanity has prevailed and they have guided down the capex plans. It is insane to expand to 150,000 MT when they are struggling to sell 40,000 MT. Cash on balance sheet is better than idle capacity which will just eat away into profits for the next 3 years

-

Acquiring an existing plant may be better than fresh expansion provided further details are given about how much capacity they are adding from this 30 Cr acquisition and from who.

-

Plans to leverage the APL Apollo brand - once again we need details on how many common distributors are there. How will the bigger scale of APL Apollo play in favor of Apollo Pipes and how does APL Apollo plan to extract it’s pound of flesh by benefiting Apollo Pipes

-

Due to the equity infusion balance sheet quality is good and one does not have to worry too much about this aspect - provided industry leading volume growth comes, if it doesn’t equity dilution will hurt the stock price more than help it

Let’s see how the conf call on May 30 goes

Disclosure: Invested for self and customers, have added over the past 3 months and may add more depending on market conditions. I am a SEBI registered IA and also run a fund

6 Likes

Happy with the investor call? could someone please share the summary

Edelweiss note:

Apollo Pipes Ltd. Q4FY19 Result First Cut (Not Rated)

Price - INR 399

M.Cap - INR 523cr

Strong revenue growth with decline in margins due to increase in raw material cost

Elevator Analysis (Q4FY19)

![]() Apollo Pipes reported a revenue of INR 89cr up 20.2 % over Q4FY18. The sales growth was on account of 11% YoY growth in volume and 8% YoY improvement in realization. The growth was also with increase in contribution from HDPE and fitting products.

Apollo Pipes reported a revenue of INR 89cr up 20.2 % over Q4FY18. The sales growth was on account of 11% YoY growth in volume and 8% YoY improvement in realization. The growth was also with increase in contribution from HDPE and fitting products.

![]() Gross Profit reported was INR 25cr flattish over Q4FY18 with decline in margin to 28.1% (vs. 33.5% in Q4FY18) due to the raw material prices increasing 30.1% over the same quarter previous year.

Gross Profit reported was INR 25cr flattish over Q4FY18 with decline in margin to 28.1% (vs. 33.5% in Q4FY18) due to the raw material prices increasing 30.1% over the same quarter previous year.

![]() EBITDA was INR 11cr down 12.3% over Q4FY18 with the margin coming in at 11.8% vs. 16.2% in Q4FY18.

EBITDA was INR 11cr down 12.3% over Q4FY18 with the margin coming in at 11.8% vs. 16.2% in Q4FY18.

![]() PAT was INR 7cr down 41.8% with a margin of 7.8% vs. 16.1% in Q4FY18; due to an inflated other income in same quarter previous year .Adjusted for other income, the PAT was down 30.8% over same quarter previous year.

PAT was INR 7cr down 41.8% with a margin of 7.8% vs. 16.1% in Q4FY18; due to an inflated other income in same quarter previous year .Adjusted for other income, the PAT was down 30.8% over same quarter previous year.

FY19 Analysis

The topline saw a growth of 27.2% over FY18 coming in at INR 362cr. The sales volume grew by 18% to 39,823 MTPA - the growth was primarily driven by strong growth in HDPE products and cPVC pipes. Increased contribution from the high-margin Fittings segment also assisted sales performance during the year. Gross profits came in at INR 99cr (up 21.4% YoY) with the margins declining 130bps to 27.5% with the increase in raw materials. EBITDA came in at INR 39cr up 19.1% YoY with the margin coming at 10.8% vs. 11.6% in FY18. PAT came in at INR24 growing 8.5% over FY18 with the margins at 6.6% vs. 7.8% in FY18.

Balance Sheet

The company decreased its Inventory to 53 days (vs. 57 in FY18). Debtor days decreased significantly to 36 (vs. 49 in FY18). Overall the Cash Conversion Profile of the company came down to 52 days (from 56 days in FY18). Also, borrowing reduced to INR 97cr from last year INR 155cr.

Valuation

Apollo pipe has 63,000 MT capacity in its two plants and expected to take it to 90,000MT by end of FY20. Also, the company is focus on continuously improving product offerings, its sales contribution from PVC pipes reduced from 79% in FY18 to 74% in FY19. Apollo expecting growth from improving utilisation of its existing plants (reported utilisation at 63% in FY19), capacity expansion in other geography, launch of new products and increase in its distribution channels. I believe that the company is in right direction and with sector improvement in coming years through GoI emphasis on water infrastructure and irrigation, Apollo would be one of the major beneficiary. Apollo Pipes is currently trading at 22x FY19 earnings.

Concall Update

![]() Capacity increase by 43% with similar growth in sales volume, expected by management. Existing volume improvement by 30% plus Bengaluru acquisition.

Capacity increase by 43% with similar growth in sales volume, expected by management. Existing volume improvement by 30% plus Bengaluru acquisition.

![]() New product portfolio of Plastic Taps, Showers, Faucets & accessories, expected to clock INR 20-30cr in coming years. Apollo is manufacturing 50% of its sales volume.

New product portfolio of Plastic Taps, Showers, Faucets & accessories, expected to clock INR 20-30cr in coming years. Apollo is manufacturing 50% of its sales volume.

![]() Company expecting the contribution from building product segment to improve to 30% going forward.

Company expecting the contribution from building product segment to improve to 30% going forward.

![]() Company has cash & balance of around INR 150cr in its book.

Company has cash & balance of around INR 150cr in its book.

![]() Apollo planned capex of ~INR 55-57cr in FY20, including Bengaluru plant acquisition.

Apollo planned capex of ~INR 55-57cr in FY20, including Bengaluru plant acquisition.

![]() Government projects contributes ~10% of its sales.

Government projects contributes ~10% of its sales.

![]() Apollo focus on distribution expansion and advertisement in coming years.

Apollo focus on distribution expansion and advertisement in coming years.

Regards

Edelweiss Professional Investor Research

3 Likes

Earning call Transcript:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/3b0f2b7c-659e-4274-90f8-b114e80ed0cd.pdf

1 Like

Q1 FY2020 results (link). Sales increased by 15.6% (volumes grew by 20%) but EPS declined because of equity dlitution.

Disc: Invested

@zygo23554 any comments?

Results on expected lines though I would have expected a higher volume growth from Apollo Pipes given that Finolex Industries grew their pipes & fittings volumes by almost the same % on a much larger base

Gross Margin at 28% has scope for improvement, going fwd even if the lower PVC resin prices continue INR depreciation can hurt the company since they import their RM. That said 28-30% gross margin should be the baseline going forward

Lower EPS anyway is expected due to the capital infusion by promoters. What is more interesting is that their have completed acquisition of the Kisan Pipes unit at Tumkur, Karnataka where they have added 9,000 MT per year at a consideration of 21.5 Cr going by the exchange filing of Kisan Pipes. This also gives them 7 acres of land which can be used for future expansion to tap into the South India market. Once they start sweating these assets from Q2 onward the volume growth for FY20 should trend higher towards 25% and maintain this growth rate through FY21 as well.

Market expects Apollo Pipes to grow much faster than industry and also build some margin comfort due to the increased scale. Let’s see how things actually pan out, if not for the high growth trajectory this does not look like a great story

Disclosure: Invested for self and customers

6 Likes