https://www.bseindia.com/xml-data/corpfiling/AttachLive/31015f26-01b9-462a-854f-9e3ace02a646.pdf

Here is promoter’s integrity in question or Not?

These promoters sold when price was at peak and now again bought through warrant !

| Jan 08, 2018 | Apollo Pipes Ltd | Sell | Market | 182,000 | 688.20 | 1,252.52 |

|---|---|---|---|---|---|---|

| Jan 05, 2018 | Meenakshi Gupta | Sell | Market | 386,654 | 708.90 | 2,740.99 |

| Jan 05, 2018 | Neera Gupta | Sell | Market | 322,800 | 708.90 | 2,288.33 |

| Jan 05, 2018 | Saroj Rani Gupta | Sell | Market | 21,520 | 708.90 | 152.56 |

Be caution about such action by Promoters …in future also they might play “PUMP and DUMP” !

why they sold earlier at price about 700 - Are they short of money? If yes, they why they are buying again at 590?

Probably they didn’t expect markets to fall

The wanted money for expansion

They came with an ingenious way to do it

Sell your shares in the market and then do a preferrrential issue

I think it’s ingenious instead of going through a fresh issue with outsiders!

In the end they probably will open the same percentage and the company will have funds for expansion

The fact that markets crashed is not really their fault

2 Likes

Please check posts 86 to 92, this has been discussed, they sold to other investors and given loan to company

FY19 Q2:

Good set of numbers

Investor presentation:

2 Likes

My notes from interaction with Apollo pipes.Thanks @zygo23554 for insights into the business.(There may be few mistakes from my side while preparing notes)

Q.It’s been impressive growth story for Apollo pipes ltd(APL) from last few years. What has been enabling us to deliver industry leading growth rate of 25%.None of the other players are growing at this rate, what is is that we are able to do? Baseline industry volume growth appears to be 11-12%.

A: Our market share is just 2% compared to top players having 8-10% market share which gives us large opportunity to grow. We are expanding to other markets of India from northern region. Our brand is also helping us to grow rapidly and acceptance of market for our pipes is good. We have started institutional sales to real estate and infrastructure players. Our group is in the pipe business for long and we know how to take risk, execute and expand the market.

Q. We have planned to expand our capacity aggressively for next few years to reach 150K MTPA by Fy20. What has changed in industry/ pipe demand which is making us to look for such capacity additions. What is driving/expected to drive the plastic pipes sector business .

A: PVC pipes market demand is good. Basically metal pipes is replaced by pvc pipe which is cheaper. Going ahead there is no replacement for pvc. Demand is mainly lead by agriculture, infra, govt push for sanitation, krishi sinchayee yojana, housing for all. PVC pipe demand will remain strong for many years.

Q. Commoditization of the piping space seems to be underway as nearly 30-40% of excess capacity will come online in next 1-2 yrs by various players. What do you think of competitive intensity/pricing pressure. How APL is trying to mitigate this scenario. We are seeing new entrants like HSIL and HIL targeting 200 Cr revenue within 3 years from launch?

A: PVC industry technology is not something unique or difficult, so everyone is trying to expand here. But as the competition intensifies smaller players will exit. Already few noted players have slowed down and looking to move away from pvc pipe segment. we can not generate higher EBITDA multiples in pvc pipes. It all depends on how well you are execute, distribution strength, cost control and efficient procurement of raw material which APL is capable of doing. We are using best technology, moulding machines like top players in industry.

Q. Our current utilisation is around ? 60% against available capacity of 70k MTPA. Do we plan to wait for utilization to raise before next expansion or continuing with planned addition.

A:Last year our production was 33K MT. Our target is 45K MT this year which is looking difficult to achieve. We are looking at capacity utilisation of 65% this year. We are planning for new plant at Raipur for 20K MT by FY20. This will help in catering to eastern region and provide better synergy with existing plant at Dadri UP. Dadri plant expansion will also happen along with this. New plant in south India will come by FY21.

Q. Can you please tell us about our Gujarat Plant utilisation. It’s been competitive market with Finolex dominance. Gaining market share in western India should give us additional confidence for other regions. How many dealers have been added in this particular region and convinced them about selling APL products.

A: Not much sales happened from Gujarat for initial few months as getting certain certifications like ISI was delayed. We are ramping our utilisation and selling 3k tons per month. We have appointed distributors(15 in no) in various districts of Guj which will drive sales. We started supplying to surrounding states from Guj plant which we use to supply from UP plant saving logistic costs.

Q. What is our targeted dealers no from current level of 120 by fy20. Do we have to extend credit for the dealers in the beginning. Normal receivable days. Receivable have increased in H1F19.

A: Our distributor no will be increased every year. We don’t extend credit to distributors normally. In Q2 receivables increased as we have push sales due to weak quarter. Normal receivables days will be in the range of 40-45 days. Even with govt sales we go for tenders where receivables are in control and sure. Institutional sales are done with letter of credit so that our money is guaranteed.

Q. Since technology is not unique and intensive, distribution seems to be the key variable here. As more players try to tie up with the same distributors, power balance may shift? What distributor margins are we paying compared to competition?

A: Distributors, brand strength are important to grow. We offer certain % margins to distributors, how much is passed on to customers is left to them. Some distributor will pass on entire margins to reach sales target and get extra incentives from company. We have certain agreements, sales target and incentives for distributors.

Q.As we use APL Apollo brand to expand market, the same dealer likely to be used for Apollo pipes also? How many common distributors are Apollo Pipes and APL Apollo Tubes likely to have 3 years from now?

A:We are not going to have common dealers with APL Apollo tubes. It’s our conscious decision not to depend on single distributor for both companies. Percentage of common distributors with APL tubes is less than 10%. We will leverage APL brand to market our products.

Q. Do we have exclusive distributors or can our distributors sell other company products as well? How does this work? In general curious to know how the distributor community likes to build their business, do they try out various product makers and eventually settle with 2-3 or do they have to commit to exclusivity right from day one?

A:Product range in PVC pipes is very diverse. It is not possible for distributor to keep high inventory/products of many companies. Generally they will have distribution with single company or few distributors will have maximum of two.

Q. Astral has grown significantly because of their association with plumbers who keep recommending the Astral brand to consumer constructing house. At APL how has been association with plumbers. In 2018 we have hardly spent 3.5 Cr on advertising, 1.3% of sales - what is more effective in the industry? Adverts or below the line marketing activity and dealer incentives?

A:Over the years Astral has built strong brand and known for its cpvc products which offers high margins. We are targeting to spend 2% of sales for advertising in Fy19. Most of the activities will be below the line model, meetings with plumbers, creating awareness among farmers, workshops for plumbers, incentivising distributors. In Gujarat we have used auto-rickshaw movement to build brand. We already have brand strength which we want take it further.

Q. Even though cpvc is mainly used for Housing, its known facts that PVC pipes also used commonly for housing. APL being predominant pvc players what is our opportunity with real estate coming back. Do we plan to expand CPVC pipes? What proportion of the business comes from agri segment? Will the growth rate here match the overall company growth rate going forward?

A:.We have been focussed on agriculture sector. Most of the sales comes from agri which has been given importance by Govt. We will grow in cpvc also. We have launching various value added products, fittings, flow regulator, valve and water taps. (I have seen some these products which they will be marketing soon). Our cpvc products will grow but as proportion it may not have much impact as pvc will grow much, We will introducing products like water taps as replacement to metal to use in houses along with various pipes.

Q. I have been hearing about banning of lead used as stabiliser. What is the present situation and govt intention on it. If we need to move towards non-lead based technology what are additional investment in existing plants. What does whole industry/APL think about it.

A:Nothing has been finalized yet. If something comes in the form of regulation whole industry has to adopt it. It is for cpvc only. It is not difficult to change the technology. It will require additional investment which will be passed on by whole industry. To some extent this was promoted by one company which is producing non lead based compound.

Q. Compared to other competitors our raw material cost as a % of revenue is high. How does this is going to change once we reach size of 1 lac MTPA or more. Can we expect raw material cost to go down as%. Operating margins and benefits due to reduction of logistic costs.

A:We import raw materials rather than buying from domestic players. Our raw material procurement is as efficient as leading players in the country. Competitor margins are high(15%) due to lot of value added products. As we continue to add value added product our margins will improve. Our operating margins will be in the range 12-13%.As we spread to other regions of country our logistics cost will come down in next few years. It will be slow process

Q. How many months of raw material inventory we maintain as company policy. Any inventory loss with sudden drop in pvc price in last one month .

A: our inventory will be for 40 days. When pvc resin price drops suddenly there will be some inventory loss.

Q. Cpvc compound sourcing. Do we have in house compounding as mentioned in Q1 PPT. Is it technically difficult.

A:.We don’t buy cpvc compound from MNCS like other players. We have technology to make our own compound from raw material. But our revenue from cpvc segment is not much presently.

Q. Working capital days and debt level over fy19-20. Capital for expansion and revenue targets?

A:Our WC days will be around 90 days. Target is to reach 80 days as we grow further and stabilises. Working capital will be funded by bank debt. Capacity expansion is done through money infused by promoters. Our target is to reach 700 cr revenue by fy21.

Q. How much premium do organized players like yourself and Finolex Industries charge in agri segment?

A: We are selling at lesser price compared to leading players in the market. As we have high growth target we need to offer discount compared to other players.

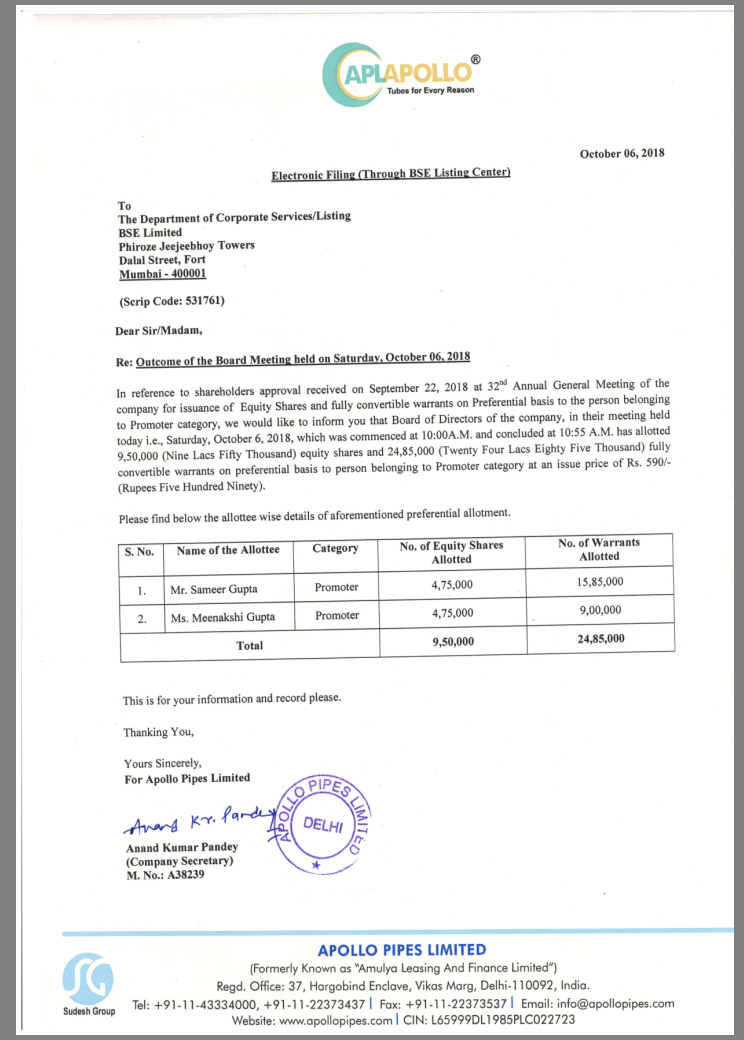

Q. Promoters initially sold stake and now increasing shareholding through equity/warrants? What is the thought process behind all these?

A:Many of existing investor in the group companies wanted to be shareholder of Apollo pipes from the early stage. Promoters have sold shares and the money has been given to company which is generating extra income for us. As APL did not require money no QIP was done earlier. As we expand our capacity money infused from promoters through equity/warrants will be utilised as required.

Overall I felt APL will grow at 20% on conservative basis(they may do better) for next few years led by capable management who knows pipe industry well.

Discl: Invested

19 Likes

Thanks for sharing ur interaction. Got some great insights about d company and industry.

Only ques that comes to my mind is why they are unable to increase their capacity utilization, being present in market for quite long still they are not able to increase share in existing markets?

Though they expanding their capacities in order to capture new markets, but what if they may struggle to increase capacity utilization at new plants.

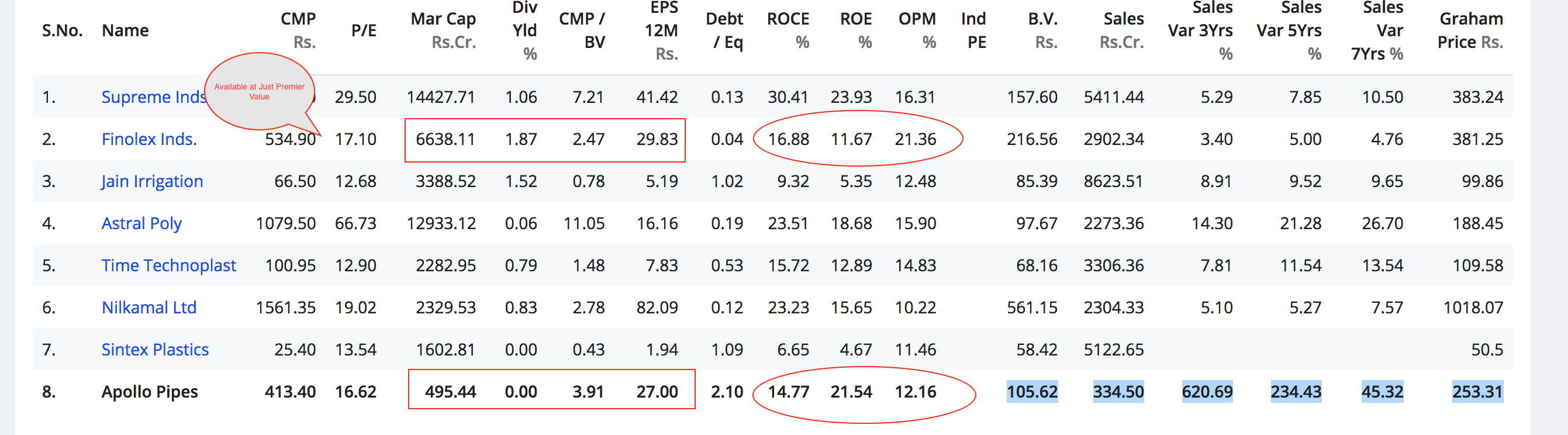

Hi All I was going through the comparision of Finolex Industry and Apollo Pipe wanted to know why one should pick Apollo Pipe over Finolex ?

One thing is the base for apollo is very small while finolex has a very large base. This means, the company can grow at a faster pace than finolex even during tough times and it has been growing fast (check past 2- 3 years).

It all depends on what kind of investor you are. If you believe in the story / product & management quality, it may be worth paying 17-18 times earnings otherwise finolex is better with proven management & products. It also has about Rs 1000 cr investments in finolex cables…

Disc: Invested in none.

2 Likes

Hi Can any one tell me what is the debt to equity for this company it is different no mentioned in different site like money control, screener,valueresearch online … i went through AR i believe it is 15cr if anyone knows please confirm as i am not sure @narendra

3 Likes

ROCE seem to be depressed here because of the huge non interest bearing fund infusion by the promoters. This fund is for aggressive expansion and to become the top 5 player in the industry. I think for this particular case we should look at ROE and it is much better than the industry average and may be due to advanced or new machinery at work.

My take on this whole sector :

- No moat or technology barrier for a new entrant to enter.

- Sector is going to expand exponentially.

- At the same time many new player are coming and existing player are expanding.

- First mover advantage is given to Astral and Finolex. But Apollo is also a strong brand which can create value for its investors.

- In this competitive sector low leveraging, high ROE , strong Brand, strong distribution and company with pan India presence will be the winner.

6.U wont get multibaggar return in this sector in near to mid term but if there is correction than we can have a decent return form this sector. - Sector is also cyclical as it is related to Infra and Reality.

Please share thought here

Disc: Holding few shares at lower level.

5 Likes

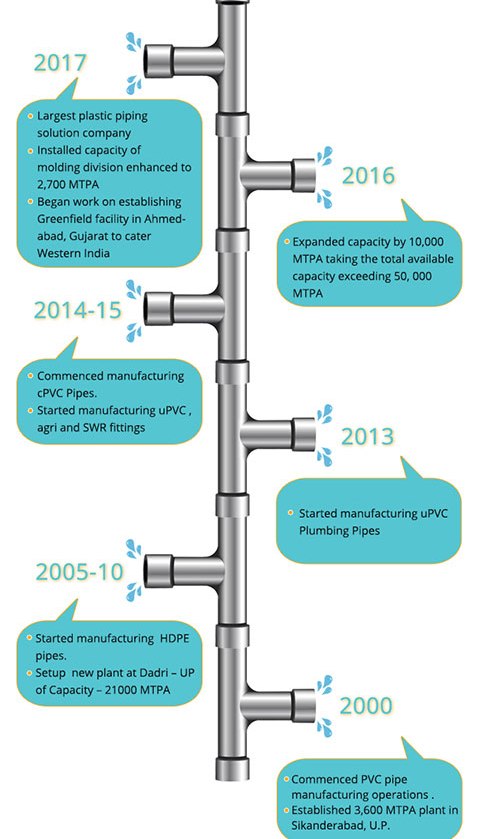

.Majority of Apollo pipes market was limited to northern region. Pvc pipe technology is nothing unique other than brand and distribution strength. Obviously other players would have taken away market share in northern region. Unfortunately the previous annual reports(Amulya leasing) does not through any light on their capacity utilization or pipe business. Below pic give you an idea about how they expanded.

FY 18 AR is very clear with their plan to expand to other regions of country and expanding capacity region wise which will help in reducing logistic costs. The concern raised by about underutilisation of capacity is genuine which we need to monitor. Management seems to be aware of it and already delayed capacity expansion by a year. They will set up Raipur plant by FY20 instead of Bengaluru plant which was planned for FY19.

I was invested in finolex considering the low valuation when compared to peers and their backward integration of pvc resin manufacturing which I thought as additional advantage. After going through the below report I understood it may not have any additional advantage and infact prone for significant inventory loss/gain. Please go through the below report which gives an idea about pvc/caustic soda market. Particularly chapter no 3 and 4 gives idea about trade agreement which gives an impression that importing may be better than infusing capital for backward integration (as per my understanding).PVC- caustic soda Report.pdf (2.5 MB)

As per H1FY19 balance sheet:

D/E= total liabilities/ shareholder equity =400/126=3.1

7 Likes

Hi Thank you so much indeed the whitepaper was containing huge information about PVC Sector and Caustic Soda . So if my understanding is correct you left finolex because it is not adding the enough capacity as compared to the demand projection by 2020 right and u opted for apollo pipe because they are increasing the capacity which is the need of the hour of the industry

Apollo Pipes Limited: Ratings upgraded to 'CRISIL A-/Stable/CRISIL A2+

3 Likes

Series of tweet from the Apollo Pipes twitter handle. Have posted a comment asking if this will be from the house Apollo Tubes or Apollo Pipes. From the series of promotion it appears Apollo Pipes. They did mention about getting in to faucet and fittings but I always thought that was in plastic. This is all new steel range. Isn’t that diversification ??

3 Likes

This group (APL Apollo) knows how to play the market for capturing “value”, so I won’t be surprised if this is an entirely new company, say ‘Apollo Fittings’ or some such.

4 Likes

Hi, All these products are made up of plastic only not steel. These products are so well designed,on first look it’s difficult to identify as made up of plastic. When I saw one such product(water tap)during my interaction it took some time for me to realise it as plastic.They did mention that they will be introducing more such products. Hope they will gain market share in this which is not very easy.

4 Likes

Well …all these products are from “ALP apollo pipes” or from the “ALP apollo tube”???

All these plastic products are from Apollo Pipes.