Margins seem to be better than experienced and industry leader like Finolex Industry?

Rcvd following clarification from co. regarding increase in debt.

Really appreciate their investor relation dept for prompt reply.

-

Borrowings under Non-current liabilities hv increased from Rs.11.54cr to Rs.151.07cr for year ending 31st March 2018.

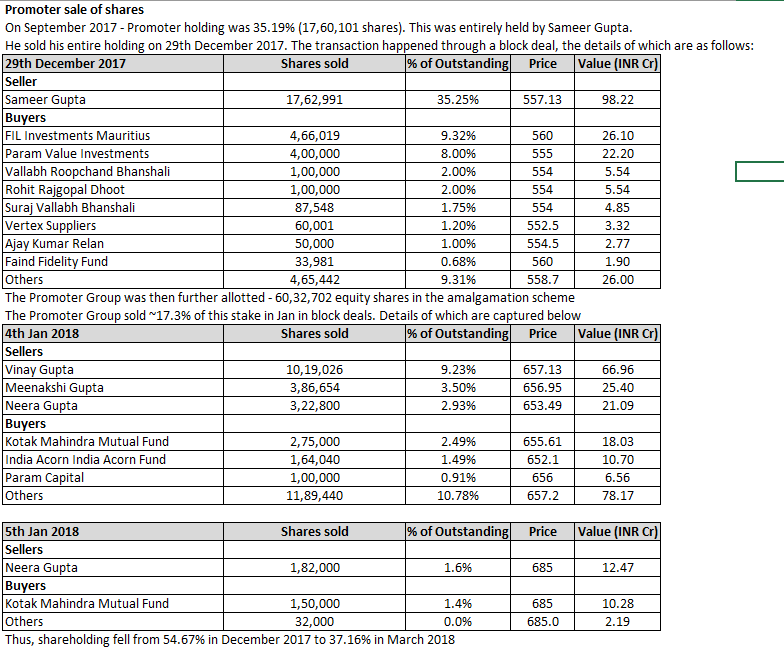

Actually post merger, the promoters sold certain stake in the company and collected the proceeds. They reinvested that amount in the company, the same is in the shape of Intt free unsecured loan.

2.Bank bal other than cash and cash equivalents hv increased significantly from Rs.1.22cr to Rs. 204.5cr for year ending 31st March 2018.

The company parked those funds in the shape of FDRs until CAPEX utilization…

11 Likes

I just have a small doubt in my mind.

Why is the promoter group selling shares when they don’t have any source to deploy the excess funds?

Promoter shareholding is now just ~37%

Does anyone have any idea about this?

I think some amount of funds the promoters got after selling shares has been parked in Apollo pipes itself. Some amount of funds have been used to acquire Best Steel logistics. This company has been taken over by Rahul Gupta who is the son of Promoter of Apollo pipes. The acquisition happened just after they sold shares of Apollo pipes. I might be wrong in the assumption.

Disc: Invested in Apollo pipes from 170 levels and also invested in Best steel logistics around 130 levels

2 Likes

Assuming this is correct, promoters converted their equity stake into interest free unsecured loan. No idea why this was done but it indicates that promoters consider equity to be riskier than an unsecured interest free loan. That’s not a good signal coming from promoters. They obviously don’t need the money for some other purpose as they reinvested it back in the company. Just changed the nature of the investment from equity to debt.

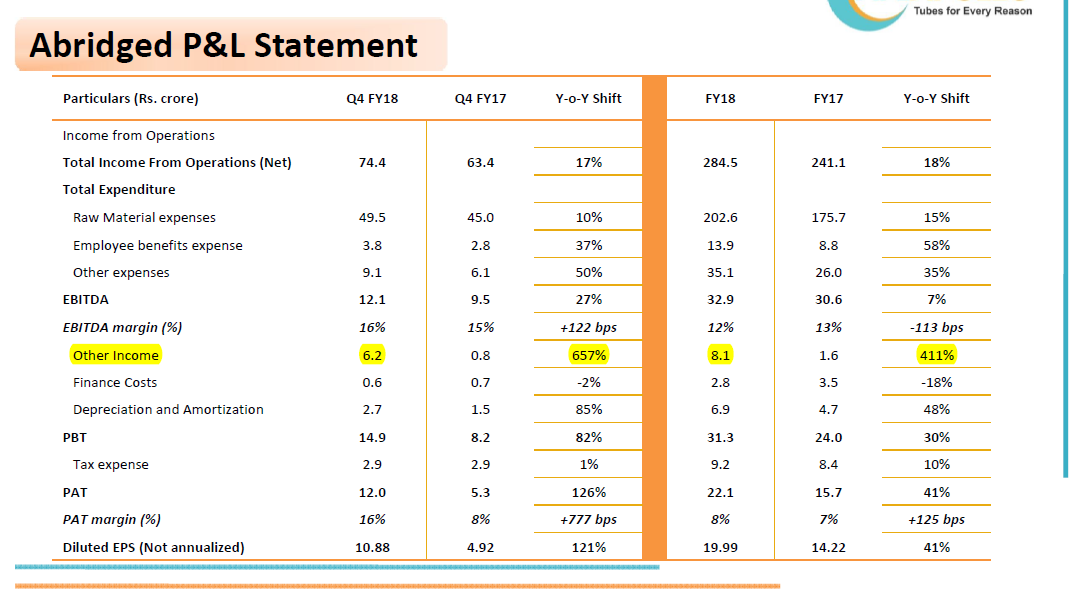

Another question I have is about Other Income of 6 Cr reported in Q4 FY 18. Any idea what is this?

This is significant amount considering net profit is only 22 Cr. Without this other income, net profit would hve been flat. Assuming a PAT of approximately 17 without this other income (net of tax on other income), At current market cap of 587 Cr, TTM PE works out to be 35. That’s a steep price to pay.

1 Like

Some of it could be interest on FDR (on interest free loan parked)

1 Like

Details of promoter sale of shares - this should help clarify some doubts. This is now put into the business as an unsecured loan. The other income is because a large portion of this is unutilised and company is earning interest on it.

One basic question/Clarification- If Promoter is selling why is the money coming to the Company bank account, is there any Preference allotment done in between?? or they have given this amount as loan to company and that money is parked in company bank account and company is earning interest on it ??

1 Like

Before we jump to conclusions on the intent - a good chunk of set of investors to whom stake was sold were the same investors who bought into APL Apollo before the stock took off. I do not find it very surprising at all that the promoters got some of the same investors on board here too - some relationships work very well and cannot be seen only through the financial lens.

Look at it this way - Promoters sold stake, money came to their personal account which they could have done anything with. Instead they got the money back into the company as a loan, it is another matter that the company does not need the money. For all we know this may be a legal way to manage the earnings for the next 3-4 Q’s through higher other income, nothing wrong with this since the best managements always figure out ways of managing and meeting investor expectations.

Apollo Pipes will share a lot of channel resources with APL Apollo, they have always spoken about APL Apollo with pride in all of their presentations and will look to cash in on the existing good will and distribution network. I do not see why a promoter family would want to put a bigger brand like APL Apollo at stake by doing some nonsense in a smaller entity like Apollo Pipes. If anything they would want to replicate the stock market success of APL Apollo with Apollo Pipes as well.

I know that a majority of what I have written here is qualitative and one can argue both ways; this is my view of the sequence of events considering the incentives involved.

Chor promoters find ways and means to siphon money off the company accounts and fill their personal accounts/assets, here you have the reverse happening. I frankly am not too concerned, would suggest folks speak to the management to get their view on this rather than jump to conclusions

3 Likes

Company is planning to add almost 100k capacity over next 18 months. Company’s current balance sheet size is 200 cr (excluding cash) for a capacity of 70k and that too based on historical cost. My back of envelope calculation suggest that they will need around 300 Cr in near future and that’s a conservative number. They will generate maximum 30-40 cr from internal accruals over this period for the rest they will have to raise debt and equity.

They could have gotten those investors on board by issuing fresh equity which company will need in near future anyway. There is nothing wrong in promoter selling their stakes to other investors. But it is little surprising when they chose to sell their stake instead of issuing fresh equity when the company will need large capital in near future for all the planned capacity expansion.Company received debt capital instead of equity which raises risk for everyone. If the company is expected to do well in near future why sell out so early?

At 35 times earnings I don’t think Apollo Pipes will replicate success of APL Apollo Tubes. 5 Years ago APL Apollo was selling for 5 times earnings. Apollo Pipes as a business will do well, but I am not so sure about the stock.

2 Likes

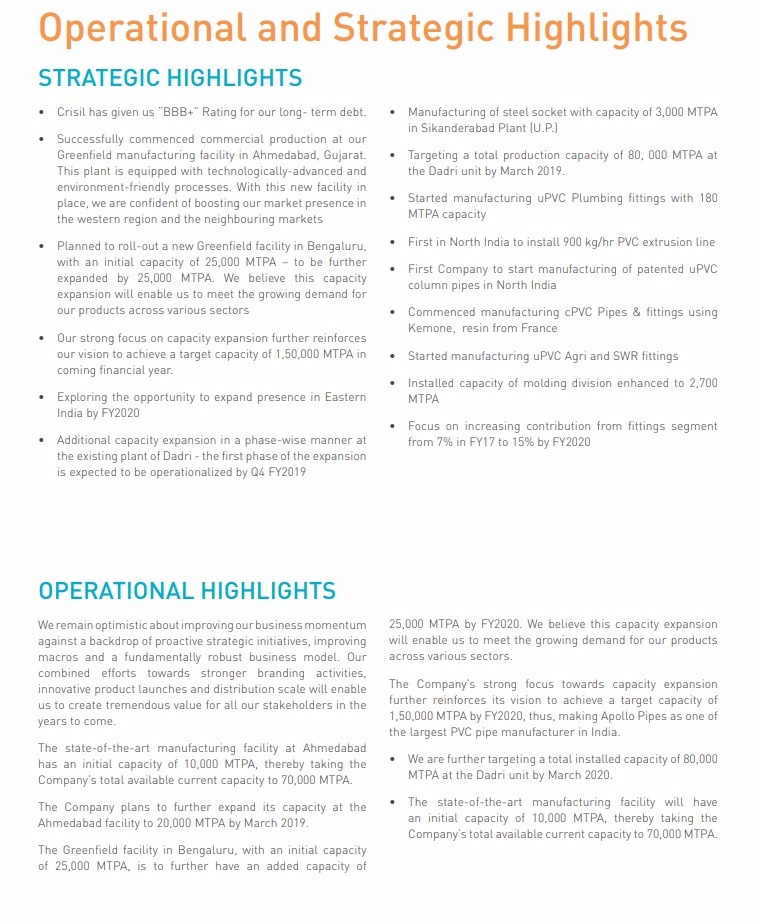

Dadri plant - 60,000 MT capacity through installation of additional lines. Additional land already secured

Ahmedabad plant - initial capacity of 10,000 MT, additional capacity through additional lines

Bangalore plant - to be commissioned by Mar 2019, land most likely already secured

Plan is to take the capacity from current level of 70,000 MT to 155,000 MT in 2 years time.

Land is already in place (100% sure) at 2 of the locations, hence capex will not be that high for additional lines. For additional lines at existing land, capex needed will be in the range of 15,000 - 20,000 per MT at max

For FY2019 and 2010 my guess is operating cash flow of approx 40-45 Cr is doable, they will at most need to borrow 100 Cr more to get to the planned capacity of 155,000 MT. Obviously the company needs money to expand but it does not need 200+ Cr on books immediately

Also their capacity utilization is approx 52% right now, my sense is that capex will be calibrated based on how much volume growth they can derive. If volumes grow aggressively, OCF will go up as well hence they won’t really need more than 100 Cr of debt/other capital in addition to internal accruals even if they were to aggressively expand and buy one more tract of land in the Eastern part of the country. Assuming their debt goes up due to aggressive capex, the D/E will still be under 1, I don’t see high risk due to capital structure here.

Valuation obviously is not cheap so one needs to be clear about the trade off here.

5 Likes

Astral poly has a current capacity of 152,100 MT, approximately same as what Apollo is planning for in 2020. Astral poly has a gross block of approximately 500 cr and total balance sheet size of 1300 cr.

5 years ago Astral had a capacity of 60,00 MT approximately what Apollo has today but Astral’s gross block was 270 Cr and total balance sheet size of 550 Cr compared to Apollo’s gross block of 100 Cr and total balance sheet size of 200 Cr (excluding cash from promoters).

Apollo Pipes has significantly lower capital cost. I don’t understand why. What am I missing?

4 Likes

@Yogesh_s Would like to update you regarding the funds required by the company.

As per management the total investment required in Bengaluru plant will be around 75cr for 50000mtpa by 2020. Though the cost of land is not included in it but still the capex will not be so high i.e 300cr.

They will be able do it easily with internal accruals n the cash which they hv on their books.

Regarding the shareholding if u see promoter holding of APL APOLLO TUBES promoters hold around 37.25% stake and promoter holding of Apollo Pipes is around 37.16% which is kinda similiar. U r right that promoter should not have sold the stake so early but maybe that could be the best possible funding available when the stock price was high.

2 Likes

Catamaran Advisors LLP (Narayan Murthy) holds 1.71 % as per latest share holding.

IDFC and Kotal mutual fund both increased stake comparing last quarter.

1 Like

Good Sales Growth QoQ as well as YoY. However the cost of the material has also gone up which has resulted in lower profits/EPS QoQ but much higher YoY.

Can someone please explain the impact of Warrants and preferential shares @ 590.

The preferencial issue being made to promoters at a price lower than mkt price does indicate that promoters are not fair to share holders

The share price is 570 while the preferential issue is 590… How the promoters are unfair?

Sorry,

I got confused with appollo tube share which is around 1800

From FY18 AR …“The Company’s strong focus towards capacity expansion

further reinforces its vision to achieve a target capacity of

1,50,000 MTPA by FY2020”

1 Like

In this annual report it showed their ambition to become 1,50,000 Mpta. But keep on repeating same points 2 to 3 times.