Over the past 90 mins or so the basic data I have gathered on the scale of current operations has already forced me to reconsider this, we may very well be onto something here.

Because of my recent work on Finolex Industries I think I should be able to collect my thoughts on this over the next week or so. Will post here once I am done with my analysis

@zygo23554 what’s your estimate of the fair value of the company? After merger, it has 1.1 Cr shares outstanding and at CMP of 709, market cap is 780 Cr. In H1 of FY 18, company reported a net profit of 5.6 Cr vs 8.3 Cr in the same period of last year, a drop of 32%. Based on the TTM profits of 13 Cr, company is already selling for 60 times earnings. It is already trading higher than my most optimistic valuation and that was based on FY 17 results My valuation will have to be lowered since the profits have dropped in H1.

In this whole exercise, promoters swapped shares of subsidiary with that of the parent. Nothing has changed on the ground. Valuation of the company has risen from 150 Cr to 780 Cr as a result. Someone who bought at the beginning of the story would be contemplating an exit now. Fear of missing out appears to be at play here.

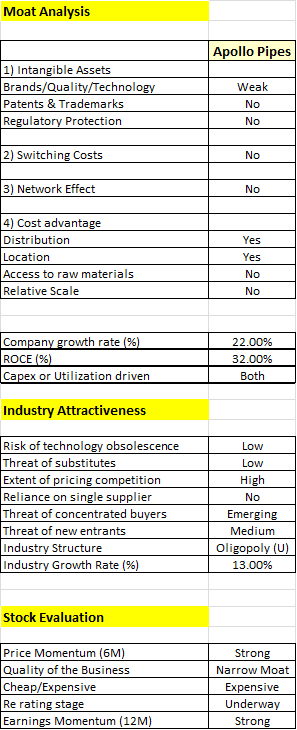

With APL Apollo, valuation was fair when the story started unfolding. Here, investors have already priced in next 3 years of growth. Apollo Pipes is up against other much larger companies in the industry so it not an easy march from here the way investors are expecting ( at least that’s what has priced in). PVC pipes is a commodity product. Many companies are getting into it. There is no doubt there will be growth, but IMO, it is already priced in.

Current installed capacity of the company = 53000 MT

Looks like capacity will be increased to 73000 MT in another 6-12 months going by the reports. Another 25000 MT expansion planned in South India, game plan appears to be take the capacity to 100000 MT by end of 2019. As per 2017 numbers the realization is in the range of 85000 - 86000 per MT which is what one would expect for this business at this scale.

In short in 6 months the company can do upwards of 520 Cr sales if they were to run at 85% utilization. At a 7% PAT (which is doable since the debt levels are very hygienic) that translates to a potential PAT of 37Cr for FY2019. Of course this will not happen so soon, one cannot build an investment thesis purely on this.

What I have understood from looking at multiple companies in this sector, one will end up spending approx INR 20000 per MT of Capex. Given the WC needs of Apollo currently, approx 18-20% of sales will end up in the working capital bucket per annum. Hence for INR 85000 of sales, one needs a total capital outlay in the range of 35000 - 37000 per MT. At an EBIT of 9%, the ROCE will be very healthy at 20% and above. This unit economics is what ensures that most companies in this segment have healthy return ratios and have traditionally been able to scale without taking on too much debt. The larger players are all free cash flow engines. An FCF company usually looks cheaper in the reverse DCF model than it does on a P/E basis, hence I am more inclined to see how the reverse DCF numbers look like for this one.

At CMP of 700, the stock price appears to be discounting a high growth rate of 25-30% over the next 3 years followed by a 15% growth rate for the next 5 years (I usually run with a 8 year model). Working capital will keep scaling at approx 18-20% of sales over the time frame. My sense is that free cash flows will start accruing from 3-4 years, till then we may see some debt build up but nothing considerable that could worry us. Don’t think this will exceed a D/E of 0.5

The big levers in this case are -

Greater scale leading to lower cost of RM (Prince Pipes does gross margins in excess of 30% at a scale that is 2.5X that of Apollo)

Product portfolio and increased realization leading to better EBITDA margins (I find it surprising that Apollo has higher margins than Prince Pipes, I would be surprised if Apollo can do more than 13% in the long run unless they start making the compound themselves like Astral and FIL)

The ability to ramp up distribution network quickly leveraging the APL Apollo brand and goodwill in the community

Ramp up in sales coupled with higher utilization leading to very high incremental ROIC in the first 3-4 years (likely to do 45%+ and then approximate ROCE at 30% over the medium term)

Each one of the above has a decent enough likelihood of happening is my reading. What can make things tougher for them in realizing this scenario is -

Every large player is adding capacity (Supreme adding 150K, FIL adding 150K, Prince likely to add 150K, Skipper and Oriplast planning to add 50K each in addition to the usual run rate of Astral). Effectively almost 600K of additional capacity will come on board over the next 18-36 months on an installed industry capacity of 1.8 to 2 Mn MT. That is a 30% increase which is fine given that the volume growth rate in the industry is expected to be in double digits. At some point of time all the players will get hungry to sweat their assets and price competition may intensify unless unorganized players get hammered from here

Almost every large player is pursuing the same strategy - add more distributors to get national level scale, get higher share from construction segment and CPVC, increase proportion of fittings to 15%+. One cannot really find too many distinguishing features either in terms of product portfolio or in terms of operations. Every one is entering each other’s turf (Astral getting into agri), FIL tying up with Lubrizol - there aren’t any niches to be seen anymore

The key question will be if all of this can make pricing more competitive and put a lid on how much one can squeeze off customers. Distributors will need to be incentivesed to push products, would not be surprised if BTL shows a spike for all players. I don’t think one will see cut throat competition since there are no concentrated buying centers here like an e-commerce player who can squeeze out margins from OEM’s over time.

My base scenario is that Apollo Pipes in 7-8 yrs time will more or less attain Prince Pipes level of scale at approx 1200 Cr and 80+ Cr of PAT. It will be very interesting to see what Prince will list at, it is a 700 Cr IPO with 200 Cr going to promoters, my guess is it may list between 2500 - 3000 Cr market cap.

I would be fine paying around 600 Cr for Apollo Pipes considering all the possibilities and astute business sense promoters have shown in the case of APL Apollo. CMP is 25-30% higher than that and I will think hard about this one, may initiate a tracking position and wait for more data to confirm to my hypothesis before I build a large position. From current levels I cannot expect an IRR of more than 20% unless something changes big time over the next 2 years and the company scales to a level way beyond than I can envisage now. APL Apollo was a screaming buy since they have virtually no competition and were the only player expanding, Apollo Pipes does not have the luxury and will need to compete with much bigger players to hang onto their market share even if the current base is low.

Big risk is that if aggressive growth in sales does not materialize in the next 2 years, the stock price has nowhere to go but down unless the entire market continues to go bonkers.

Though Astral has other business as well now (Adhesive) this will be interesting to see how next 2 years unfolds for Apollo Pipes, specially they are planning to leverage APL Apollo brand for PVC/CPVC pipes.

Disclaimer: Invested & planning to increase the allocation once more information is available.

Two big takeaways (additional information over and above what was already known) for me -

In house compounding for the CPVC segment (a la Astral)

Adopted Cash and Carry model (looks like they are trying to a Finolex Industries here, at least in the agri segment)

If I read between the lines, they are already setting very lofty aspirations for this business. The above two are best practices which leading competitors have tried out and perfected over a period of time. Whether they actually pull it off or not only time will tell, but looks like they very clearly mean business.

In the presentation they state that sales volume over the period of 5 yrs, is around 50% of the installed capacity. For the FY 17, sales vol. is 28900 MTPA (54.5% of Ins cap), Does it mean that there is no demand as of now. Ramping up the capacity to 1 lac MTPA by FY 2019 may end up in idle capacity considering the compitition by big league.

Discl: Invested

There is a confusion in market cap. While Screener shows the Mkt cap as 742 Cr while money control and some analysts say mkt cap is 342 Cr. Which is correct?

correct market cap is 742 Crs. How do we justify the valuation gap as the stock seems to be trading at 40x FY19 earnings (assuming it doubles its profit of FY17). The company has couple of red flags:

a) got listed through the back door…reverse merger route while a simpler option and better price discovery would have been to come with an IPO.

b) The company’s name until 3 months ago was Amulya leasing…a big red flag in the past.

c) The capacity utilisation is 50% and FY15 had a big component from capital gains. Excluding that, the PAT margin is just 2% until FY15 (fy13/fy14/fy15)

d) The promoters I believe have sold to the marquee investors. Not sure how to look at this but maybe because the promoters and related entities had more than 90% stock due to the reverse merger process.

Why capacity utilisation is so low, they are not even utilising their available capacity but moving ahead with expansion.

Could not find any justification regarding low capacity utilisation.

Whereas astral pipes is utilising their plant at 95% as per their latest concall , moreover HSIL which has commenced its PVC pipes in Telangana is expecting revenue of about 800crs from 60,000mtpa in next two years.

Apollo pipes- whether they are unable to sell their products amid competition or something else is missing here.

Finally initiated a small position in this, am hoping the small cap correction continues and this gives better entry points.

Don’t see any great degree of comfort at a market cap of 600 Cr but one needs to begin somewhere. Let’s see how this pans out, worst case scenario I end up holding a laggard for the next 2-3 years, risk of capital loss is not high here.

I pretty much agree with your view of the business quality.

Distributed production and leveraging the APL Apollo distribution network can be a pretty good combination though one shouldn’t bet on that right away.

I think the crux of the story here is the very healthy volume growth in the overall industry and possibility of market leading growth from Apollo Pipes, coupled with 20%+ ROCE and the prospect of favorable industry economics resulting in a free cash flow engine that can fund its growth over the medium term.

Valuation is finally starting to look more saner though it isn’t cheap yet by any means. But then as I posted earlier, one has to start biting in such stories without being too much of a valuation nazi

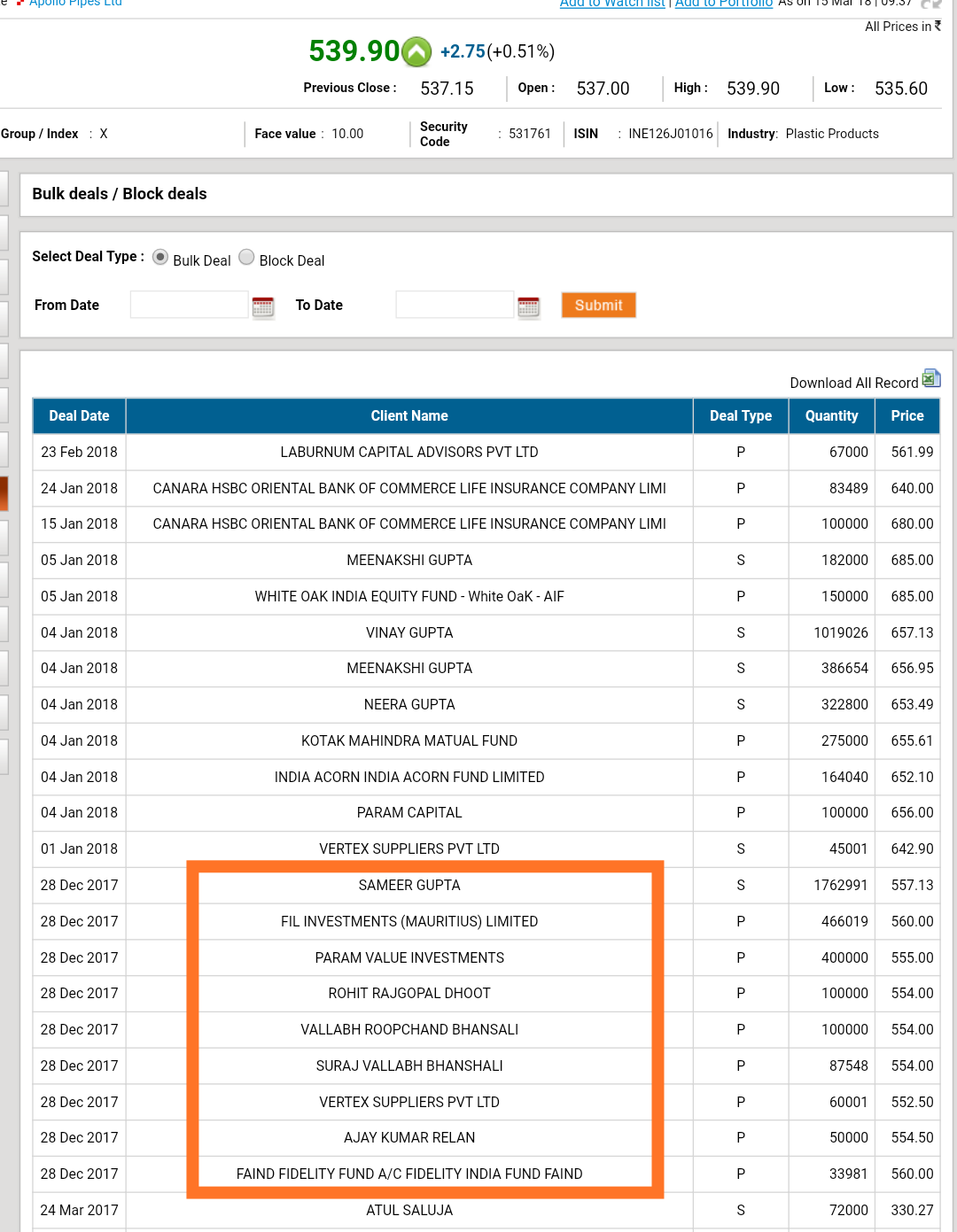

In dec many marquee names like Mukul Aggrawal, Ajay Relan etc entered d scrip.

Param value investment bought 4,00,000 shares more than 1%.

But despite that none of them is visible in shareholding pattern for dec quarter??