Hi,

Im a homemaker and I started investing towards the end of 2013.

The main things that I look for while selecting companies are the opportunity size and management competency. The checks that I do to assess management competency are to see if the mgmt. has followed up on their plans from the past annual reports,profitability ratios of the company and basic checks about promoters from publicly available information.

I don’t prefer to churn my portfolio a lot. My top 6 holdings except Natco have been holding for last 4-5 yrs averaging up on some occasions.

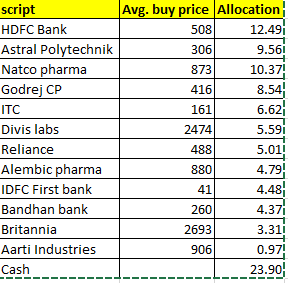

Last october, I did some clean up, and now this is how my portfolio looks like.

Company Average buy price %of portfolio

HDFC Bank 810 20%

Tata Elxsi 307 13%

Astral Polytechnik 379 9%

Natco Pharma 868 8%

Godrej cons. prod 460 8%

Jyothy labs 94 7%

Gruh Finance 142 7%

IDFC First bank 41 5%

Reliance 488 5%

Deepak Nitrite 240 3%

Repco Home fin 497 3%

Other than these I have 1-2% tracking positions in Mayur, CCL prod and vinati organics and remaining in cash

Rationale for investment:

HDFC Bank- most reliable and safe in banking industry and has still a long runway for about 20% growth

Tata Elxsi - Operates in niche area and huge opportunity size. Negatives are that merger with TCS is a possibility and dependence on JLR

Astral - High growth, they have been growing profits at 20% when the real estate sector is down. My expectation is that things will get even better for them when real estate picksup.

Natcopharma - This is one company that has been dragging down my portfolio’s performance. But I have faith in the management and Im willing to hold it for another year to see where it goes.

Godrej consumer products - very innovative company with high appetite for growth. Their Indian business is doing really well. Their international business is not doing so well in latin america and Africa. Everything depends on how quickly they can turnaround and become profitable in these geographies.

Jyothy Labs:This is one company that understands the indian consumer mindset very well. Their products Ujala, Exo and Pril are doing very well against HULs Robin blue, vim etc.

Im betting on them coming up with a few more blockbuster products. They have plans to acquire some regional brands and take it national .

Gruh Finance:

I have been holding this since 2014 and it has been a steady compounder for me. Now the merger with Bandhan Bank came out of blue. Im continuing to hold it since I believe that it is not a bad deal for Gruh finance share holders and Bandhan has good operating metrics.

IDFC Bank.

The only reason Im invested in this bank as of now is my faith in Mr.Vaidyanathan’s leadership.

I strongly believe that he can turn things around at IDFC bank.

Reliance- for adding stability to the portfolio.

Deepak Nitrite - The new phenolics plant is expected to double the revenues and company has plans to produce downsteam products from phenol and Acetone.

My risk taking ability is moderate. Portfolio is down about 18% from the highs of mid 2018, but im not too much worried about it. I’m expecting 20-25% returns from this portfolio.

I request feedback from seniors and fellow Value Pickers on my portfolio