Amrutanjan produces and sells ayurvedic OTC healthcare products. The company’s 100% subsidiary AHCL makes the chemicals for the products. The CMD of the company is Mr. Sambhu Prasad who took over 9 year back. The company is more than 100 yrs old and was set up in 1893. Earlier the company used sell only the yellow pain balm. Everyone in South India knows this company and must have used the pain balm. A few years back the company undertook a re-branding exercise and launched a white pain balm. It also acquired Siva Soft Drink which owns the Fruitnik brand.

From the FY14 Annual Report

We wish to grow the next 3-5 years at a CAGR of 33%. This is bold. But looking at the past, one can argue we are trending in the right direction. 2000-2005: 0% 2005-2009: 5% 2010-2013: 10%

Focus on Head , Body and Congestion areas for our core business and offer/build portfolios in each vertical. We wish to also expand on our smaller portfolio of other products like Sanitary napkins and foot care products(corn caps) that can grow by entering the distribution chain and reaching consumers. Once they individually reach a level of sales that is self sustaining brand investments can happen. We have other unique OTC products that will be entering the market space this year.

The challenges for a company our size is to match the investments in media attempted by our much larger competitors. We have to recognize that our nearest competitor is 10 times our size and two of the smaller brands have sold out to larger competitors in the last 5 years. This was a very dormant category till 2009! Inspite of these head winds we executed to sustain in this business. This industry is driven by investments in the brand and this is a fact. Share of Voice and Share of Market are correlated strongly. We wish to steadily increase our share of voice to a level that will help us build new brands, and sustain existing ones.

Key Investment Arguments

Even if company can sustain 15-20% sales growth (and not 33% like they are targetting) margins will expand meaningfully because of operating leverage which could lead to much faster PAT growth. You can already see the growth pick up in FY15 and 1HFY16 already.

684crs market cap company. Zero debt company and has net cash of Rs38crs. Pays 30-40% of profits out as dividends.

Has plant in Mylapore, Chennai which has been shifted to the outskirts of Chennai. The land available of 2.5 acres is worth upwards of Rs150crs. Dont know when it will be monetized though. In FY09 company sold land for Rs84crs and paid a special dividend and also did a buyback.

Key risks as I see it

Small company with a topline of just Rs171crs. Advertising is critical for sales growth. Dont know if it can spend and compete with the likes of Zandu. Elder’s Tiger balm is another competitor. Subsidiary which makes the chemicals for the balms is loss making. Consolidated profits are Rs2crs lower than standalone profits.

Big investors in the stock already

----Vijay Kedia of Atul Auto fame

----Sundaram Mutual Fund.

Disclaimer:

----Have only done research based on publically available data and not met management.

---- Am invested in the company so my views might be biased.

The management has covered their raw material costs for the year through long-term contracts. Hence, 2Q gross margin expansion of 299bps is likely to continue in 2HFY16. The company has tied up with a third-party manufacturer in East India for supplying beverages in that market from 4QFY16 onwards at favourable terms. This, in turn, will protect gross margin of the business and help the company save on transportation costs as it was supplying the product from Chennai till date.

The management is confident of delivering 5% volume growth in the OTC business, with 5-6% of price increase in its core pain relieving balm. New format products like back-pain roll-on and feminine hygiene products are expected to grow 100% this year. The beverage business will deliver ~17-18% growth this year, given that 1HFY16 was subdued on account of a short summer and disruption in business due to assigning a third-party manufacturer for the eastern

region.

Amrutanjan Health Care Ltd has informed BSE that the Board of Directors of the Company at its meeting held on March 11, 2016, inter alia, declared 2nd Interim Dividend of Rs. 2.65/- per share for the year 2015-2016 (132.50% on face value of Rs. 2/-) on the Equity Shares of the Company.

The Board Meeting commenced at 10.15 A.M. and concluded at 11.00 A.M.

Tracked this stock for a few weeks towards end of last year - what attracted me was the fact that their factory is located on a Rs 300cr piece of land in Chennai,which is a significant part of the valuation. However I’ve heard from a reliable source in Chennai that the MD spends quite a lot of time overseas and therefore there were concerns about his lack of intensity/bandwidth to grow this biz. It may still grow, but I’d rather invest in market leaders run by intelligent fantatics than companies such as Amrutanjan that at its core is more of a lifestyle biz. Odds may change if they professionalize.

This is company of interest due to the strong heritage brand which has a strong equity in south india.

One of the things that concerns me regarding this is their foray into Beverages - they have acquired a Beverage brand called Fruitnik (case of Diworsification?)

Notes to Amrutanjan’s consolidated financial statements (Page 109) reflects the above comparison. All segments other than OTC Products have been pulling the operating profits down for at least the past 2 years annual report data.

On the other hand, Emami’s Annual report 2015-16 has already been released and per page 196, Emami has a single primary business segment “Personal & Healthcare products”. So direct comparison on segmental profits and revenues with Amrutanjan is not facilitated. However, Emami’s 2015-16 annual report Page 34 states " the next few years will witness several OTC products launched by Emami across categories". Additionally, Emami has multiple OTC Brands-Zandu, Mentho Plus & Fast Relief.

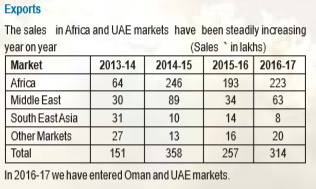

Just landed here anf when dig in to the company annual report i found they are increasing the topline and expanding their reach in african counteries (As per Annual report 2016-17)

in my opinion BALM is still in trends in the countieries with low income group

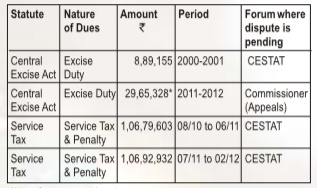

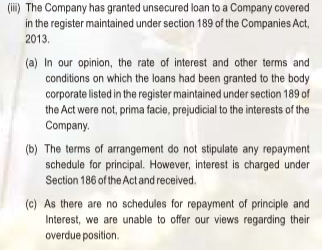

**Cautionary flags

There is amount which may be payable by the company are as

another flag for me is another snip from the annual report

Dis : i am not holding any stock of the company but doing the research to find rational for investment

I have been following Amrutanjan since a long time. I didn’t invest owing to Valuation. So that might give you a hint. But it’ll certainly make a good case for an analysis and Valuation.

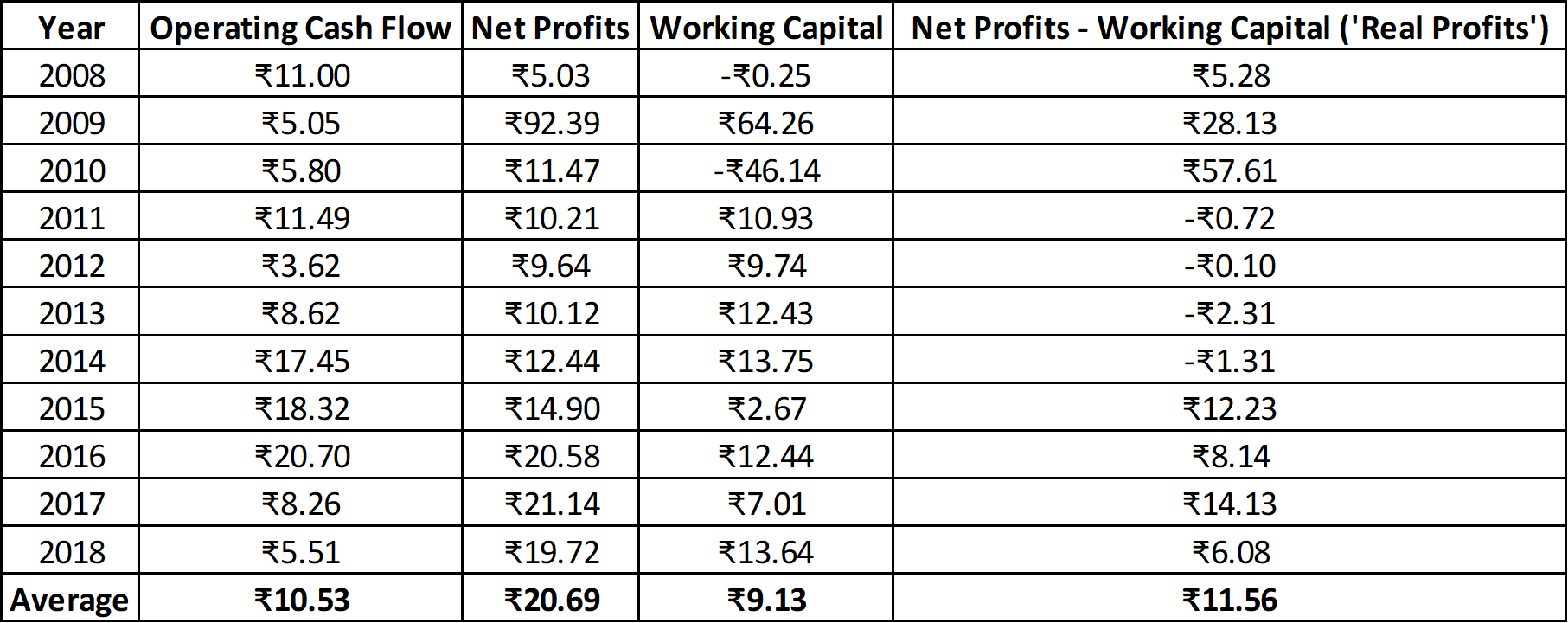

Please when you do consider analyzing this company please let us know the reason of gap b/w PAT and Cash Flow from Operating income. In the last 3 years there is huge gap

You can see that the average OCF of Amrutanjan is not far away from the calculated Net-Net Profits (Or ‘Real Profits’). So, I don’t see an issue there.

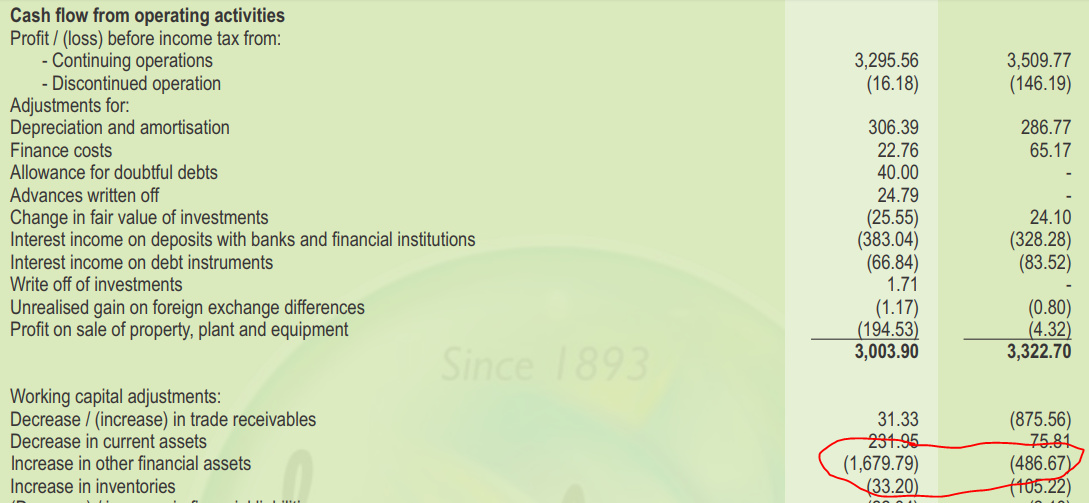

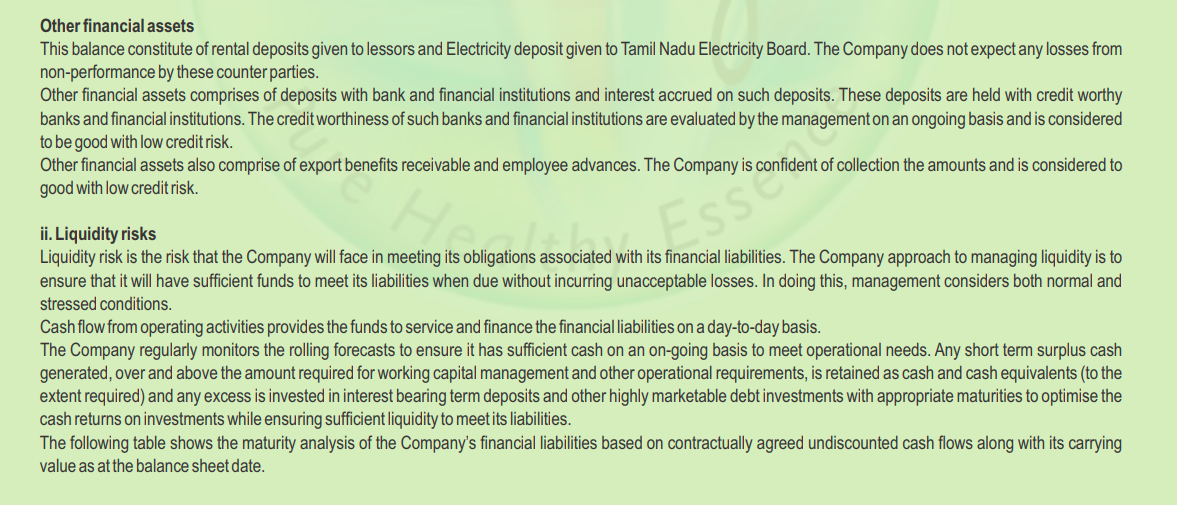

As far as the short term departure is concerned, this is largely due to the removal of change in ‘Other Financial Assets’ from the Profits in the Cash Flow Statement (Seen in Working Capital Adjustments):

Cash and Cash Equivalents do not form part of Working Capital and should not be deducted from the P&L to arrive at the OCF. I fail to understand how an increase in Bank Deposits is a ‘Non Cash’ item. And why they are being deducted from the P&L (Since they are a change in the Balance Sheet, not the P&L itself). They also seem to have made no adjustments to ‘Other Financial Assets’ in the transition to IndAS.

I supposed it could be an anomaly created by sticking to rigid definitions (Treating ‘Other Financial Assets’ as Working Capital without paying attention to the fact that they are just Bank Deposits).

in cashflow statement, adjustments are made to net profit which are non cash and non operational in nature to arrive at operational profit before working capital changes. then, wc changes are adjusted from this figure to arrive at ocf.

the real profit that you have calculated is net profit adjusted for wc changes. which is the non cash and non operational portions. i am not able to understand how this figure (non cash + non operational items) are compared with ocf, and then saying because they are almost the same, its ok.

as per CF statement,

NP +/- (non cash & non operational items) +/- wc changes = ocf

as per your table,

real profit = NP +/- wc changes

therefore (solving mathematically), real profit +/- (non cash & non op items) = ocf

But the major Non-Cash item that isn’t Working Capital is usually just Depreciation, which is fairly small.

As far as Non-operating items are concerned, these are usually Sale of Assets (Which is not a regular activity). Amrutanjan had sold some Assets in the last two years, but they don’t do it repetitively.

In conclusion, Working Capital covers almost 90% of the deviation from OCF and Net Profit. But yes, in order to be completely thorough, you need to do include the above items as well.

In this specific case, my biggest doubt is why a change in ‘Other Financial Assets’ (Consisting largely of Bank and other Financial Deposits) is being considered as a Working Capital change. In fact, a change in Cash and Cash Equivalents only happens in the Balance Sheet. They contribute nothing to the P&L directly and therefore, should not be adjusted (Reduced) from Profits to arrive at the OCF. Maybe someone well versed in Accountancy can answer this.