very well summarized. thanks

Thanks @varundarji for sharing notes. I have two question, may be little late to party.

-

If they are expecting decline in Supima and Giza cotton, why they are thinking to increase the capacity of spindle? Is it because even in the decline they will have demands for new one as they have good relationship with existing customer ?

-

Does the same spindle can be used for other cotton blending also because you wrote “In future, if there is a shortage of Supima/Giza, the buyer will understand and Ambika can blend other cotton varieties as per the requirement of the client.” . If yes, this means they can grow in other segment but I guess they don’t want to because it is already overcrowded?

1 Like

thanks for sharing your meeting notes.

Catamaran Investments (investment vehicle of Infosys founder - NR Narayanmurthy), has invested in Ambika Cotton as per latest shareholding released for 30 Sep 2015, with a 2% stake…

Catamaran has had an excellent track record identifying investments early with multibaggers in CanFin Homes, SKS Microfinance, Hector Beverages (Paper Boat), Manipal Education amongst other investments…

8 Likes

Couple of links from Capitalmind highlighting potential issues for Yarn Industry.

1)The Trans-Pacific-Partnership-The US, Canada, Japan and 9 other countries are getting their free trade act together.

2)30% crash in Yarn prices since last year

two-danger-signs-for-the-yarn-industry-which-will-impact-our-exports-big-time

6 Likes

Read here about my concerns about RM supply and possibility that Ambika is already using 5-7% of global supply of PIMA + GAZA. Ambika Cotton Mills

To get clarification on the same I attended AGM. Would not post on the details of AGM as someone has already posted the same. Few highlights

1. MD said he is not aware of the market size or past historical growth of market.

2. Ambika is using 5% of Pima plus Giza global production.

3. No more spindles expansion.

There is a very high possibility that overall market for Ambika niche cotton is not very large and is not growing. So its unreasonable to expect them to grow volumes at 15% CAGR for next five years. I was under impression that Ambika holds less than 1-2% of market share and can grow comfortably at 15% CAGR Whatever growth will happen post 30K spindles expansion will be driven by forward integration. Promoter is a capable man and am not doubting that forward integration will be any problem. But my understanding that current business could grow at 15% or higher volumes for next 5-7 years was wrong.

I don’t think he is being too conservative is saying that no more spindles expansion. With already 5-7% of global supply which might increase further with current expansion, spindles expansion may no longer be feasible.

18 Likes

Average results from Ambika.

No growth in revenue and profit

http://corporates.bseindia.com/xml-data/corpfiling/AttachLive/4B21AD1E_20F1_4885_925F_58EFCA2AA1AF_154105.pdf

Thanks Varundarji for your AGM report,good details on imp.aspects.Regards,V

Can anybody tell me what is the current count of number of spindles excluding 30000

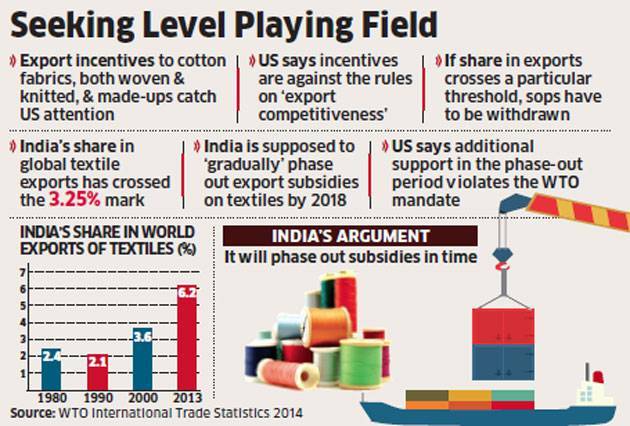

US opposes India’s latest round of incentives to boost textile exports

NEW DELHI: The United States has opposed India’s latest round of incentives to provide a fillip to exports, alleging violation of a global trade rule for export competitiveness in textiles.

Commerce department officials said the US raised this issue more than a week ago, after India increased support for exports of several products including textiles while expanding the scope of the Merchandise Exports from India Scheme (MEIS) on October 30.

The government included exports of cotton fabrics, both woven and knitted, and made-ups to leading markets including African countries under the MEIS. Under the World Trade Organisation’s agreement on subsidies and countervailing measures, when the export share of a developing country with per capita income below $1,000 a year touches 3.25% in any product category for two consecutive calendar years it is deemed to have gained “export competitiveness”.

Such a country is then required to phase out export subsidies for the items for eight years from the second year of breach. The WTO mandates developing countries to phase out the export subsidies within the eight-year period, preferably in a progressive manner. The WTO had in 2010 asked India to consider phasing out the subsidies for textiles and clothing.

“However, a developing country member shall not increase the level of its export subsidies, and shall eliminate them within a period shorter…when the use of such export subsidies is inconsistent with its development needs,” the agreement says.

The US has flagged the issue of export competitiveness in textiles and said that India cannot give additional subsidy during the phase-out period, said an official, requesting not to be identified. Another official, in the Cotton Textiles Export Promotion Council, said India has crossed the export limit and the government is aware of this but the market is moving slow.

“As for the removal of subsidies, we can either gradually phase them out or immediately stop them in 2018 on a pre-decided date,” he said.

What will be likely impact of this on Ambika??

Sanjay as per the 2014-15 annual report the current count of spindle is 108228. So management is planning a 30% expansion in capacity at a cost of 130 crores funded through internal accruals. This from understanding mean management still sees further demand for their products. The cost of capacity expansion for 30000 swindles is 130 crores.

So the cost of total capacity including the 30000 spindle would be close to 600 crores if someone were to create a similar capacity . Of course there is depreciation and other factors to be considered. For me at 500 Crores market cap(CMP 800) it looks fairly valued considering the fact that it is a debt free company with close to 20% gross profit margin.

Disclaimer: Invested in this stock

but have they done the expansion…i mean it was supposed to add in the revenues in the last quarter itself…since it was not reflecting in the last quarter results i became a bit skeptical…

Somewhere it was mentioned that Ambika’s threads break much lesser than that of its competitors(i.e superior quality of product). Isn’t that a moat already? I couldn’t help asking this question as people are still saying that they couldn’t isolate a proper moat for Ambika.

I came to know about a great gesture by promoter Mr P. V. Chandran through the latest blog post by our favorite Prof. Sanjay Bakshi.

As per the latest disclosure to exchange, Mr. P. V. Chandran proposed to annul 2% net profit commission which was earlier part of his remuneration and it was accepted by the remuneration committee. It is an excellent example of promoter integrity and simplicity.

Disc: Not invested.

2 Likes

This is my first post in this august forum.

Union Commerce minister has voiced her worries that recent signing of Trans pacific pact between 12 nations will hurt India specially Leather, Textiles and Chemicals. As India is not signatory to the pact, Export oriented industries in the affected segments will have to compete against MFN status enjoyed among the signatory nations.

In view of the this recent development, whether Industries are equipped to meet this challenge or yet to prepare themselves.

Members views are requested.

1 Like

Catamaran has put in more, now stake at 3.73%.

Eicher family (investment company) has pepped up the stake to 2.21%.

Source: bse

Disclosure: on watch list for last 6 months. ( I generally maintain an excel with the businesses (stocks), I want to own at my desired valuation and scoop up when prices kiss during volatile mkts). Ambika for me will be a buy at 680 or 7x ttm PE

1 Like

Visible slow down in sales & profit growth. Also decline in net margins.IMO…Moat is missing & its in a fragmented & competitive market, where aggressive pricing or/and capex investment (interest & dep) will keep check on net margins.

Valuation wise attractive compared to peers. But Business quality & performance wise its lagging. Overall Welspun & Indo Count are better placed than Ambika.

3 Likes

I think Management part is what we should also be considering. Ambica Cotton scores pretty high in this.

There is considerable weightage to be given for Management. BMV model i,e Business-Management-Valuation. I would like to give equal weightage to all 3 instead of just focusing each of them in an isolated way.

4 Likes

Please share the xl if possible.