I would say that wind mills were required for securing the power, which was scarce in Tamil Nadu. So I would still call it capex. Though agree with other points.

1 Like

Hi @varadharajanr,

Your above post has one of my articles “Equity Research: Ambika Cotton Mills Limited” entirely copied from my website:

It is expected from you to give credits to the original author/work whenever his/her work is referred.

Vijay

24 Likes

A friend of mine called up and said as per his estimates Ambika cotton consumption is 10% of total production of Pima and Giza variety. I did my calculation independently and came to about same conclusion.

It’s quite possible that there is some error in the way I am looking at the data.

If not then we should worry about 1) opportunity size and possible growth going forward [Am looking beyond 30K spindles capacity expansion] 2) Availability of cotton itself owing to severe drought in California [it produces > 90% of US Pima cotton production]. In 2015 area under Pima has declined from 2 to 1 Lakh acre [read this article http://www.nytimes.com/2015/08/08/business/a-once-flourishing-pima-cotton-industry-withers-in-an-arid-california.html?_r=1] . Even in Egypt area under Giza cotton is declining due to removal of subsidies on cotton. [http://english.ahram.org.eg/NewsContent/3/12/119530/Business/Economy/New-subsidy-cut-may-be-the-end-of-Egyptian-Cotton.aspx]

Here are my calculations:

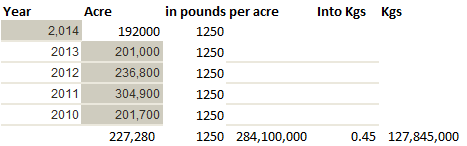

For USA

So US is around 13crs Kg . See this link for US area under PIMA cotton http://www.supima.com/view-reports/acreage-estimate/ . Pounds per acre is from NYT article referred above.

Egypt produced 370,000 bales during 2014 . One bale = 225kgs. This amount to 8.3crs kgs

[see this link http://gain.fas.usda.gov/Recent%20GAIN%20Publications/Cotton%20and%20Products%20Annual_Cairo_Egypt_3-30-2014.pdf] 90% of Egypt cotton is extra long and long staple variety.

So Pima + Giza amounts to 21crs kg for 2014. As per Ambika website cotton consumption for 2014 was 1.89 cr kg and for 2015 2.23cr kg. So as per my estimates Ambika is already consuming around 10% of global production. Atleast for next 2-3 yrs it seems global production is not going to increase. So to repeat 1) Opportunity size ??? 2) Availability of cotton ???

7 Likes

Hi Rohit - Agree that this will still be capex. But the point i am making is that it is not maintenance capex. On another note, this capex was not mandatory. An option available to Ambika mills was to go for a dedicated feeder and enter into a PPA with another wind power generator and simply buy wind power. Thus capex was not necessary.

This capex allowed them to improve their operating margins in long term and need to be viewed accordingly. Historical rate of increase in electricity tariff in India is 5.5% (CEA data). Few years down the line the wind mills will help in significant power reduction costs.

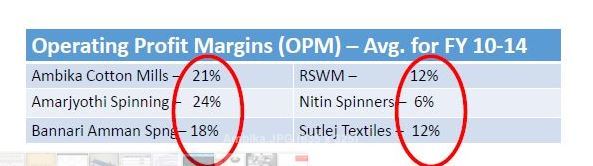

On a side note - As per an analysis that I have done on some listed companies in textile space, OPM for textile companies that have their captive wind projects is much higher for textile companies that do not have a captive renewable energy source. Companies on left have captive wind mills whereas companies in right do not (except RSWM which has commissioned a 20 MW wind mill an year ago. However even this 20 MW is equivalent to 4 MW of thermal power project. their existing thermal power project is of 50 MW. I am assuming therefore the impact is not much in this case even after having a windmill

1 Like

I was zapped for a moment and then I realized what I had done.

Oh my bad - if you notice carefully, the first section and last section contain inputs that I had solicited from industry experts. For each of the companies I track, I keep a master document containing everything I can lay my hands on the company. In ambika’s case, I had copied your blog’s inputs verbatim into the word document which was succeeded by inputs from a reputed textile entrepreneur in coimbatore.

I just copied the entire document into VP thread without bothering to remove your blog in the middle. I had no intention of claiming credit or passing off your work as my own.

apologies and sorry about that. Uploading the word doc I maintain on ambika as is - which incidentally has another positive ref check I had done.

ambika.docx (81.0 KB)

3 Likes

Hi Anil,

IMHO the link below can provide us insight that supply is not a concern yet as stock exists after taking into account local supply and exports.

http://www.supima.com/view-reports/supply-and-use/

The winds are favouring the Indian Textile industry and also factories in China are lowering their production due to high overhead costs and hence demand for raw material would decrease in China. The excess raw material can then make way to India.

Ok.

All the best for your investing journey!

3 Likes

First of all apologies it was not 44 million but 44 cr.I tried finding cash flow from data which are shared in Q4 report. This was before annual report came out . Actual FCF for 2015 was 32 Cr and if you take last three avg FCF it comes out to be 39 cr.

with these Value per share comes (11% growth in FCF) out to be 1167 and with 50 % margin of safety -583

DCF is dangerous and very hard tool to value company …you need to make assumptions and when there are regular capex it becomes more hard so only way out is averaging and using long term historical growth avgs. Ambika is more of consistent player so you can probably do this.

Trying to join this conversation and to keep it as simple as possible. -

- Ambika Cotton is a commodity provider.

- There seems to be a global slowdown, specially in China and Europe, US also has tepid growth.

- Domestic demand in india is slowing down…

- Due to 1 above, Ambika Cotton would be a cyclical.

- Due to 2,3 above Ambika Cotton would have a rise in inventories (about the same levels as in 2010 and 2011 is seen in the balance sheet). Last 4 quarters show flattening revenue growth and I would suspect declining revenues going forward.

- Due to slowdown in Commodity and Consumer Demand, people might want to switch to cheaper alternatives.

Which means headwinds ahead, Sales Slowdown and therefore Earnings/CFO slow down. So this should have an impact on Ambika stock prices going forward. Inventories going up and flattening sales means lack of demand…supply side constraints don’t apply if demand is slow. One way to check this would be to find out who the clients of Ambika Cotton are and see their income statements for the last 10 quarters…

I know this is simple without elaborate calculations…but I am trying to understand whether this is worth my time before diving deeper. If I have made any mistakes here pls. point out and I will be grateful.

1 Like

@drvijaymalik- sir i do read your blog. its one of best writings out there. its so nice to see u on valuepickr. your inputs will be highly helpful.

3 Likes

C Bhavnani who owns 38% stake in the Company is the wife of Mr Chandran. This is confirmed by the annual report of Ambika for FY15 - http://www.bseindia.com/bseplus/AnnualReport/531978/5319780315.pdf

Key points from AR

- Management is bullish on growth prospects – as was disclosed in the results, Company plans to setup another spinning unit of 30,000 spindles with 100% compact facility consisting of imported and indigenous machinery, with total cost of 130 crores. This will be largely financed by internal accruals

- AR says that specialty cotton yarn does not closely track economic growth, and is consistently growing. Company continues to have good demand for its products, and continues to strengthen its production base by modernization and adding balancing equipments

- Management focus is to maximize per spindle EBITDA, which as we know is one of the highest in the industry

- Export % of sales have been reduced from 65% in FY14 to 59% in FY15

- Long term Debt has been reduced from 61 crores in FY14 to 16 crores in FY15, and Mr Chandran is focused on working with minimal or no debt

12 Likes

Thanks @sta

I am happy that you liked my blog and found the articles useful.

Valuepickr is a vital source of in-depth discussions and understanding about many of the stocks. I have benefited from it and wish that other investors also make good use of the plethora of information available here and incorporate it in their stock analysis.

All the best for your investing journey!

regards,

Vijay

4 Likes

I will be attending Ambika Cotton Mills AGM in Coimbatore tom.

Please feel free to post your questions here which I could take up with the mgmt.

1 Like

@varundarji Thanks for doing this. Couple of questions from me

- Name of the top 5 customers and % of revenues from them.

- When will the new plant (30,000 spindles) be operational? and What will be its expected contribution to the revenue/profit?

1 Like

Hey Varun,

What is their vision for the future? What kind of scalability is possible in the next 5 years or more?

1 Like

- How does slowing china economy affects Ambika , why did exports come down

- Do they plan to move up value chain i.e. Weaving ,Garments (Forward integration)

- There is increasing competition from others in compact segment from Garment manufactures like Arvind

It will be great if you can publish whatever you learn from AGM. It is very difficult to get information on their plans., industry dynamics and future

Hi Varun,

One of the key concerns some investors like me have is the 2nd line of management - Daughters and other senior management team. It would be good if you can try and assess the same. For example-

Interact with daughters and senior management team to understand their competency level - Asking specific queries addressed to them during AGM or after the AGM, etc.

Thanks for your help

Hi Varun,

Please do share your notes from the AGM

I had the privilege to attend the AGM of Ambika Cotton Mills on Sep 23, 2015 at Coimbatore. Following are the key highlights:

On Mr. P.V. Chandran

• This company is what it is because of Mr. Chandran, he sounded very positive on the growth and future of the company

• Seemed much focused on the Corporate Governance of the company. Doesn’t use company transport, drives his self owned car. He said he feels he is robbing shareholders if he uses company assets for personal use.

• Very shareholder oriented. In the AGM, he said that you all shareholders are my partners and have the same right as I do except for the fact that I have an additional duty to run the company

• This year owing to an experiment in Ginning process he is foregoing his annual commission, because he thinks this experiment is critical to safeguard the success of the company. This cost is approx INR 1 crore (last year his commission was ~1.2 crore)

• He doesn’t like debt on his balance sheet. He claims he sleeps peacefully at night if he has no debt

• He is fan of Warren Buffet, gave several one liners of the legendary investor during a candid chat

On the 30,000 new spindles

• This is work in progress for the company. They require some govt approvals for this to install this. He candidly admitted there is slowdown in the approval process, but he won’t use any measure other than the actual process to take approvals from the govt. That speaks volume of his integrity and honesty

• Once the approval is sought, it won’t take much time to ramp up production. He claims he has man/skill/scale/orders

• New 30k spindles will have knitting facility, but the process of installing it would depend on the mkt conditions and demand from his buyers. He said he can’t just install the spindles and start manufacturing yarns. He needs to see and check if the additional spindles would be a net positive for the company, EBITDA/spindle is favourable (explained below)

• These 30k additional spindles would be most probably the last spindle capacity addition. In future, fabric manufacturing and garment manufacturing could be the possible, but would depend on the mkt condition then

• When asked if fabrication and garmenting would be outside his circle off competence, he said that fabric/garment manufacturing is easy because quality of the yarn is the most important --> Sounds like Never ask the barber whether you need a haircut or no!

• Fabrication cost is just INR 6/metre and packing cost is INR 4/metre. Garmenting involves some skill; he said we can do it.

• Any additional task like adding spindles or improving a process he always check if there is net +ve for Ambika

• Ambika’s customers were pushing for capacity addition since a long time, but he said owing to the nature of the industry, one should carefully assess the mkt and then take the leap

• New spindles will be provided to the same set of customers, no new customers for now

On customers

• Customers and the qty supplied are an extreme secret owing to the nature of the industry

• Decline to comment on the customers names and their % share in total revenues

• Long lasting customer relationships (some for the last 17-18 yrs)

• He said that the industry is such that you have to be very mindful of the P&Ls. You have to ‘rob’ the profits (yes, rob!) from other stakeholders, else it’s difficult to be successful and profitable in the long run

On Suppliers (Domestic)

• Procures cotton locally through brokers with v v long lasting relationships

• Met one of the brokers, who said that this man is like a God to them. Never cheats them, never directly crosses them and procures directly

• Thinks like a pure gentlemen and gives reasonable profits to his suppliers

• His domestic suppliers are shareholders since its IPO --> Huge positive. One man claimed he will never sell their shares

On Suppliers (International)

• He claims the global supplier for Supima cotton has said that Ambika is his most trusted and favorite customer

• He claims he will always get Supima from them at good terms

On the future

• Sounded extremely confident on his company future

• No comments on growth and profitability in 5-10 yrs down the lines questions, but he said that we can keep doing the right thing and keep everything else to God!

On decline in Pima and Giza Cotton production decline

• He said ppl look at the textile spinning companies at the wrong way, it should be looked at EBITDA/spindle rather than top line growth since raw material cost as % sales is high. Gave the example of Gold manufacturing companies’ vs silver manufacturing companies.

• EBITDA/Spindle is the highest in the industry and nobody comes even close. Growth of Ambika should be measured by this metric rather than absolute growth. There are companies in India which do INR 300 crs of turnover with 150-200k spindles (vs INR 500 crs of Ambika with 110k spindles), this is lower because yarn spinning is extremely skilful and not everybody can do it

• They manufacture only if they have an order. The buyer knows about the availability of the raw materials. He will undertake an order only if he thinks there is a profit

• In future, if there is a shortage of Supima/Giza, the buyer will understand and Ambika can blend other cotton varieties as per the requirement of the client.

• He in fact admitted that he will be happy if there is a shortage of Supima and Giza Cotton because spinning these cottons is very very skilful and very few ppl in the world (even fewer in India) can do it.

• My opinion: I wasn’t convinced by his explanation on above points especially the decline in Supima and Giza cotton production

On the yarn and cotton industry in India

• He admitted that the cotton/yarn industry in India, especially in TN, is in a mess.

• Dr. Venkatachalam (Independent director on Ambika’s board) who is an advisor to 600+ yarn companies in India, said there will be many mills (~30%) that be insolvent by the end of the year. He had mighty praises for Mr. Chandran and Ambika. He said that this is one of the best managed companies in India in this industry.

• India is closely watching China, since its steps to tackle a slowdown could affect yarn companies in India

• Chinese companies could possibly start operating at prices below cost to eliminate competition from India. For now, its wait and watch

• Power shortage is a critical problem for the industry in TN. However, the TN govt is committed to this problem and by next year TN will be a power surplus state. The industry is negotiating very hard with the discoms for a better rate and claim that they are on the verge of a solution. Starting next year, power situation would not be an issue for the industry

On Local competition

• Hardly any players in India who makes what Ambika does. He admitted that he is facing stiff competition from Gujarat based spinning companies (not sure which companies he was referring to)

• His view is that their business model isn’t sustainable because they supply to yarn traders (and not the end customers like Ambika does) which operate on 1-3% margins. Given how wildly yarn prices fluctuate, one swing and they will out of the mkt.

• He said that Guj based companies have access to cheaper power (~INR 5/unit) because Guj state govt grants them power subsidy (~INR 1/unit), but with the improving power situation in TN plus the windmills of Ambika has, this advantage isn’t material enough for the Guj based companies vs Ambika

• Additionally, companies in Gujarat work for 330 days a year vs 362 days for Ambika (Not sure how he arrived at 362 a year figure). This additional 32 days of operation in year covers a good proportion of cost of Ambika vs the Guj based companies

On debt

• He reiterated that he doesn’t like debt for two reasons. 1) He can sleep well at night if he is BS is debt free. 2) The T&Cs under which banks give loans in India isn’t what he likes. He would like to take loans under much favourable conditions than that they presently do

• One of the shareholders asked why he is repaying debt when the TUFS loan can be availed at 5%. He countered by saying that he would be happy to place surplus money in deposit at 8-9% vs the 5% loan cost and would continue to that in future

• By the end of FY16, Ambika will be almost debt free (LT debt of only INR 3 crs by end of FY16)

On Spindle life

• I asked him, what is avg life of the spindle of the new 30k spindles and existing spindles? He said that the actual life is 22-23 yrs but they take a conservative view and depreciate it over ~19 yrs (stated in AR)

On succession plans

• Frankly, this is one of the concerns which I have and unfortunately, I have no good news. There wasn’t a talk of a succession plan

• He has 3 daughters (incl. 2 twins) and the eldest one is actively playing a role in company. She is with Mr. Chandran from 10am to 6pm day in and day out. Other 2 twin daughters have no interest in running the company.

• I spoke with one of his suppliers, he said that Mr. Chandran is in the pink of his health and for now we shouldn’t worry

NOTE: The above information is for INFORMATION PURPOSE ONLY. This is my first attempt at writing detailed notes for a AGM. Other members who have attended pls add points which I may have missed.

Views/Critics most welcome!

71 Likes