Although it’s related to an IT case, it does mention there was a dispute in between the promoters.

Maybe it was resolved with UTI’s intervention and there’s nothing to worry about.

Record cotton yarn imports by China have resulted from policies that have supported domestic cotton prices above

market-clearing levels, due to which spinning cotton locally is less attractive than importing yarn.

This could be a boost to Ambika.

Source: http://www.thehindu.com

To attract more investments ahead of the Global Investors Meet, the Tamil Nadu government will come up with a new textile policy in the next few days. Minister for Handlooms and Textiles S. Gokula Indira said the government was planning to introduce suitable tax concessions and the single window system for the approval of the investment proposals.

1 Like

Was going through entire thread, what a fantastic discussion and research.

So, what is the expectation from Q1 on 8th Aug

Only this textile gem has not moved in last few weeks in this textile rally ?

Q1 Results out. Seem disappointing.

Total Income up from 121.36cr (Jun-2014) to 124.22cr (Jun-2015)

PBT down from 18.09cr (Jun-2014) to 16.03cr (Jun-2015)

PAT down from 13.20cr (Jun-2014) to 12.07cr (Jun-2015)

Discl: Not invested

Q1 Result is out

Other income is decreased from 4Cr to 2Cr and Other Expense is increased from 14 Cr to 19 Cr.

We can see capital employed is increased from 330 Cr to 380 Cr any clue ??

Even the tiny textiles companies are posting strong results, any idea wat went wrong?? RM cost and other expenses went up? some unfavorable base effect i can see- Q1FY15 was exceptionally good,

Disclosure- invested

I think majorly the unfavorable impact is due to rise in “Other expenses”…this has reduced the operating income by almost 4 Cr., otherwise the financials look ok.

The nos. at first look, looks okay … while the business remains high quality, I personally feel,there are not enough tailwinds to support the Industry.

1 Like

IMO, Ambika is more of a stable long term bet in textile industry. Its fortunes will not go too much up and down like other textile companies. One reason is that the raw material used by Ambika is Supima cotton, whose prices dont move in line with the regular cotton.

Capacities constraints may have had an effect on the Q1 results. We will have to go for new capacity to go onstream.

3 Likes

Hi Everyone,

New to the group. Intrigued by the detailed evaluation of Ambika. I was looking at some of the data posted by you all. Looks like Ambika operational revenue seems to be increasing YoY but the capacity has not seen an expansion since 2009.

Two possibilities

- They were under utilized since 2009, if so at what was their capacity utilization

- They improved working efficiency of the machines.

I would think 1 & 2. Does anyone have a breakup? What is the utilization now?

After addition of 30K spindles one could see an addition of 120-140 cr to the top line. This is assuming the fact that they will see 90-100% utilization of additional capacity and currently they are operating in that range.

Thanks

Isn’t this a buying opportunity - A 18-20% RoE growing company with strong moats quoting at just 1.7 times book value?

1 Like

Hi,

It will be great to understand the current capacity of spindle’s which Ambika is operating and operational utilization and expansion being planned. Any timelines are expected for them to be operational. Thanks.

although Ambika is down 16 % on bad results but results weren’t that bad esp year 31 March 2015. Sales in KG went up by 22% but average per KG price realization went down from RS 319 per KG to 278 KG in 2015.

One thing which came out from my analysis is somehow raw material per kg used is always 53 % of sales price , which might lead to conclusion that they are able to vary pricing as per input material.

Still need to check on Q1 results though.

Dis : invested at 1008

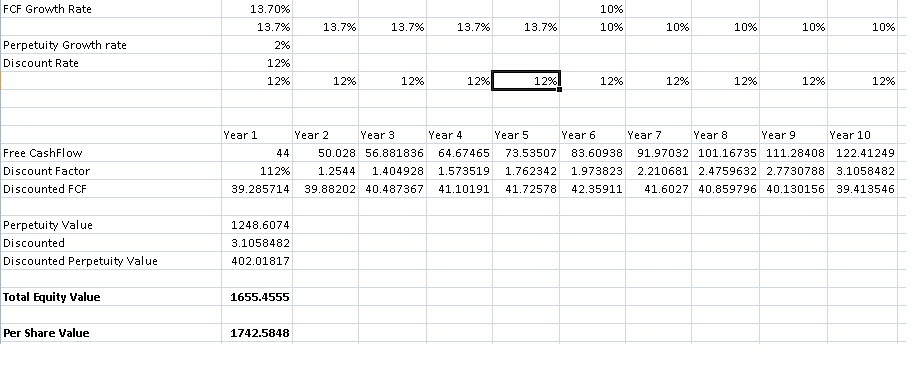

My valuation was based on DC F though with less margin of safety . Iam not able to paste my calculation as i am new user.

Initial cash flow : RS 44 Million

Discount rate : 12 %

FCF growth rate for first 5 years = 13.7 % ( taking FCF growth rate for last 10 years and dividing by 2) and next 5 years at 10 %

Terminal growth = 2%

Gives = Rs 1436 As fair value

Ideally should have taken 50 % MOS to wait for Rs 718 ( this is wat Prof paid ) but anyways got carried way by moat story in this forum and that stock may not fall  went against my usually style and put money together …

went against my usually style and put money together …

1 Like

@vinamrachaware - good effort.

Couple of questions:

- How did you arrive at the FCF figure of 44 million?

- Assuming the initial cashflow as 44 million, what is the logic behind growing it by 13.7%?

I am raising this question because textile industry by nature is very high capex intensive i.e. in simple terms it needs frequent upgradation of technology, machinery etc to compete with other players

If you see the historical FCF generation of Ambika, I think it has generated positive cash flow in only 4 out of last 9 years which includes major capex in 2007, 2008, 2011 and 2014. If you apply negative FCF every alternate year based on historical trend, I guess the fair value will go below CMP.

1 Like

1…I have carried forward Amit’s assumption of 44 million

Nt sure how he arrived @ 44 million

But my excel giving different values

2…FCF growth rate for first 5 years = 13.7 % ( taking FCF growth rate for last 10 years and dividing by 2) ???

I am also not able to get How Amit get it?

@ amitverma21

Calculating FCF for textile business is merely optical illusion.

This industry requires huge capex and you never know a single capex can eat up 3 years of FCF.

Newbie here. I think the core question is - why are the results bad? Without knowing much I have jumped to the assumption that it could be because of global slowdown and therefore reduction in demand for Cotton…does anyone know what is the true reason? Thanks.

Hi, please note that a lot of capex in past has been for setting up windmills and thus not on core plant machinery. Capex in windmill besides providing low cost power on LCOE basis, also provided tax savings (accelerated depreciation of 80% in one full FY in the year of investment).

I am not much conversant with balance sheets, but someone into it can perhaps explore how much capex has been in windmills and plant machinery. This should provide a better view on FCF. Infact, it will be helpful if such an analysis can be posted here. Many thanks