Recently two important and interesting things happened with the company

Strategic alliance with Kronos ( Kronos is the global leader in workforce management and develops solutions that are used by more than 30,000 organisations and 40 million users daily)

Kronos is growing pretty well and reported revenue for the year at $1.3 billion. EBITDA at $390 million

Interestingly jagadish ( CEO of Allsec) mentioned that

“The tie-up wouldinitially be restricted to Indian operations. But going forward itwould be forged for other geographies also, Mr Jagadish said statingthat the company planned to be in operation in atleast 40 countriesby March next year”

Secondly, Carlyle (PE promoter of Allsec), Bought Visionary Revenue Cycle Management, a provider of healthcare solutions supposedly for 420Cr

The unlisted company’s revenue was about $25 million and operating profit was $14 million.

There is a buzz that Carlyle may look at merging VRCM with another business process outsourcing company that it owns, Allsec Technologies, to build scale and later exit.

Recent results were also strong and a strong PE like Carlyle backed company which has shown promising turn around is available at ~10 P/E and with ~100cr Cash and short term investments in the balance sheet

Looks like a very interesting counter to keep track of!

How will the Kronos tie-up affect their topline going ahead? Do they have a revenue share model and will they be servicing Kronos’ existing clients as well?

Also, I noticed that the assets and liabilities of AML have reduced significantly during the December quarter with no significant impact to the topline or bottomline (mostly affected by employee increase and taxes). Anybody knows why?

There were 2 investor nominee directors on the board. Both have resigned together citing “Personal Reasons”. Obviously this cannot be true. What can this mean? Can anyone throw some light on this ?

My imagination is since Carlyle has not sold any share. This could be an internal restructuring, let us wait and see if they appoint other directors. First Carlyle hold 30.86% in the company. This quite big holding.

My major worry here is about the AML business. They clearly said they cannot preempt if standard chartered contract will be renewed. And if it isn’t, there will be a major hit to rev and pat (more than 50% of the revenue and 1/3rd PAT is coming from AML division). Did they tell when is the ongoing contract going to end? They said they are pursuing other AML opportunities; any breakthroughs yet?

Again, AML division didn’t perform as well both qoq and yoy on either topline of bottomline. AML segment asset number also decreased considerably to half. What’s going on here?

Regarding tax - I see they have still not started paying full taxes. Any word on that?

Cash/Current investments - As per Q2 FY17-18, there was 35 cr cash and 65 cr current investment on consolidated Balance Sheet. What are these current investments? Are they generating any income?

Next leg of growth - Where do you think Allsec is going to attain its next leg of growth? They clearly said there is no scope of margin improvement, so it has to come through volume growth.

Disclaimer: Was invested earlier. Following the story.

Technical view -

Bearish divergence both at the last top and the current levels on weekly charts.

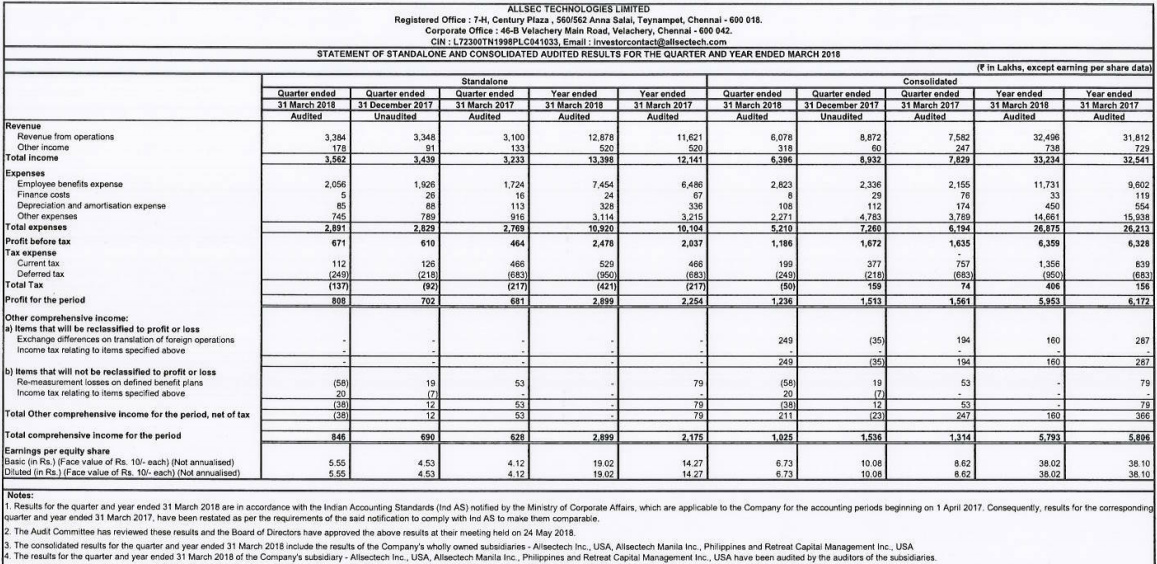

Allsec came out with Q4 results today. Good part is dividend of Rs 5. But, the performance of AML division has deteriorated. I guess the contract with StanC has come to an end and hasn’t been renewed yet.

Company has 66 crores of cash and 73 crores of investments. This implies that the business is available at roughly 200 crores (correct me if I am wrong).

Domestic Business -

8% growth in domestic revenues Y-o-Y but employee cost has also gone up and other expenses have come down. Overall good growth in profits for domestic business.

CLM - Revenues have grown quite considerably Y-o-Y and Q-o-Q but the profits have dipped. This can be attributed to the hiring activity which is happening in quite good numbers.

HRO - Revenues have grown by 20% Y-o-Y and also has decent Q-o-Q growth. The profit margins are also good and is the best performing business segment margin wise and profit wise for the current quarter.

AML - Reveues are down by nearly 69% Y-o-Y and 73% Q-o-Q. Profits are down a lot.

If the revenues dry up completely for AML, then we can have a huge loss and would lead to near zero profits for the overall business. Need to get clarification from the management on the same.

I had written to the CS of the company and received the replies -

In the recent quarter results, the AML division performance was dismal but the employee cost has increased. Why is it so?

This is on account of reduction in volumes from a large AML customer.>

Can we expect the AML division to perform better in next quarters?

The Company continues to make efforts in adding more customers to this segment which will help in managing fluctuations in volumes. The division performance will depend on the success of these efforts>

Have we on boarded any new clients in AML and other divisions?

We have not added any new clients in AML. We however do have normal client additions in our other businesses>

Can we expect the employee cost to go down? Considering that there hasn’t been significant increase in revenues from your other businesses also.

This will move in line with our revenues over the next year>

When can we have the investor presentation for q4 fy18?

The Company operates three segments globally viz., Human Resources Operation (HRO) covering HRMS, Statutory Compliances, payroll services, time and attendance management; Customer Lifecycle Management (CLM) which encompasses lead generation, customer retention and relationship management comprising both voice and non-voice processes and Anti Money Laundering and Compliance services (AML).

The HRO business unit has continued to grow steadily this year making inroads into the Asian, Middle-East and African markets.

The CLM-Domestic business has improved in volumes and in margins as compared to the previous year. The CLM-International business has remained stable over the last year.

The Company has delivery centers in India at Chennai, Bangalore & NCR locations. In the international front, Allsec has centers in Manila (Philippines) and Dallas (United States of America).

The HRO services and CLM services are delivered from India and the subsidiary in Philippines while AML services are provided by the US subsidiary.

Today, Allsec has a pan India presence and a capacity of over 2500 seats with facilities in 3 locations which are in NCR, Bengaluru, and Chennai. Apart from India, we also have a capacity of 600 seats in Manila and around 200 seats in USA.

Allsec, is in an industry where attrition is one of the major concern areas. Allsec has an annual attrition of 32% (marginally down from 33% last year) which is almost similar to the Industry average.

Major deterioration in financials of Retreat Capital Management Inc., USA. From a profit of Rs. 20.37 cr it gave a loss of Rs. 1.58 cr. Looks like AML business has taken a big hit. This subsidiary was doing AML business till fy2017. In FY18 company has shifted some AML business into other subsidiary Allsectech Inc., USA.

Cash and Mutual funds are of Rs. 139 cr. and current Mcap is Rs. 380 cr. How this cash will be utilised remains to be seen.

This was news to me (I don’t see this disclosure in last years AR) and as per Q4 FY 18 results which showed a dip in AML segment, not sure what the possibilities for the ALM business are next year.

Which customer can give this much revenue to ALLSEC? Are they referring to USA govt? Because, thru get most of the work from govt dept. If yes, then there is a risk of being blacklisted but not of loosing business because of no work. They get work from many different departments.

The customer was StanChart far as I know. The project has ended, now the AML business has no customers and will report 0 revenue from Q3 FY19. However, there will be some fixed cost for some more time. At the moment they are trying to find new customers.