There is a possibility that they have recognised sales at cost. And profits will be recognised in next qtr when partner shares the final sales data. Similar thing happened with Cipla-Nexium in last qtr.

3 Likes

Alembic Pharma Investor Presentation…

http://www.alembic-india.com/upload/05Investor%20Presentation%20Q1_15-16.pdf

Q1FY16 conf call (quick highlights)

Pranav Amin - “Q1FY16 does not reflect any of the profit share of Aripiprazole (gAbilify), as we do with any of our partner products.”

Key Takeaways -

- Q1FY16 revenue reflects cost of the gAbilify shipped

- Q1FY16 does not reflect profit; it will be reflected a quarter later

- Q2FY16 number is when we will see effect of gAbilify profit (which is major component)

Cheers!

12 Likes

Alembic Pharma Q1FY16 CONCALL

05Transcript-APL-Jul31-2015.pdf (127.3 KB)

Highlights

Aripiprazole launch

The Q1 numbers do not reflect any profit share of Aripiprazole. These will show up only in Q2. This was a limited competition day #1 launch which off late you do not see very often. So we are happy that we could successfully supply product and launchthe product on day #1 itself. Our partner has also got a decent market share in the market.

Only player with the ODT( Orally Disintegrating Tablets) version on Aripiprazole

Launching in this quarter, though its not a big market.

Increase in R&D expense

-R&D revenue expenses were Rs. 48 crores during the quarter versus 30 crores in the previous quarter, increase of 60%.

- More emphasis on injectables and dermatologicals

-R&D is going to be the most important driver for future and hence getting more aggressive with the R&D projects

On track on The US front

-On-boarded Mr. Craig Salmon(Sandoz) as Head of US business also two other people in the US.

- Celebrex launch probably in December and Pristiq in 2017.

3 Likes

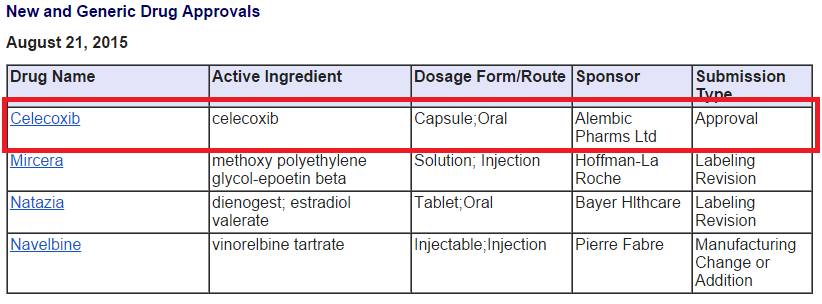

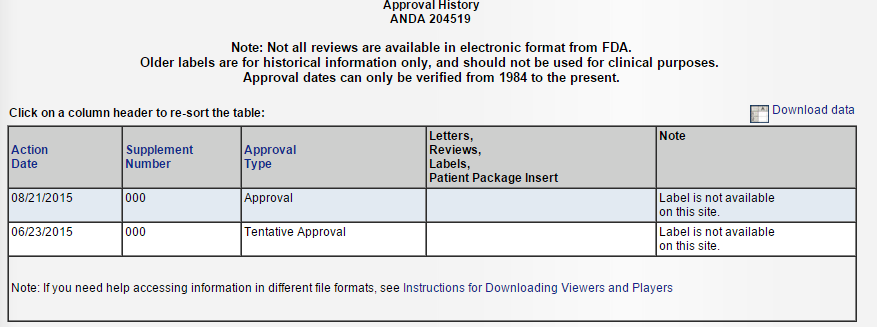

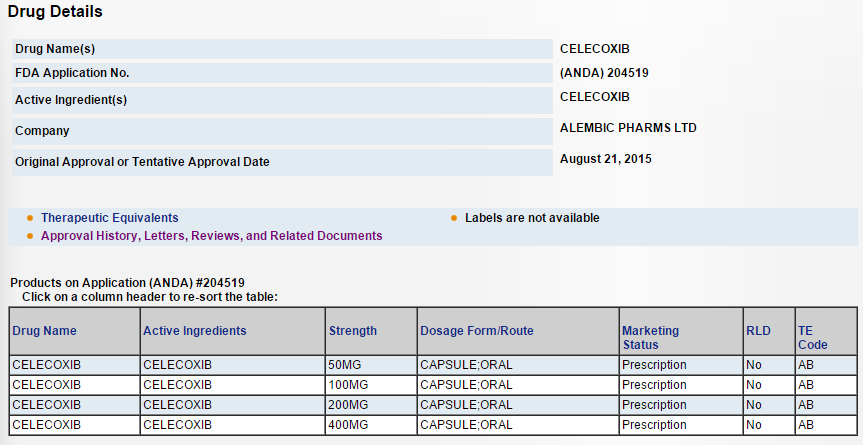

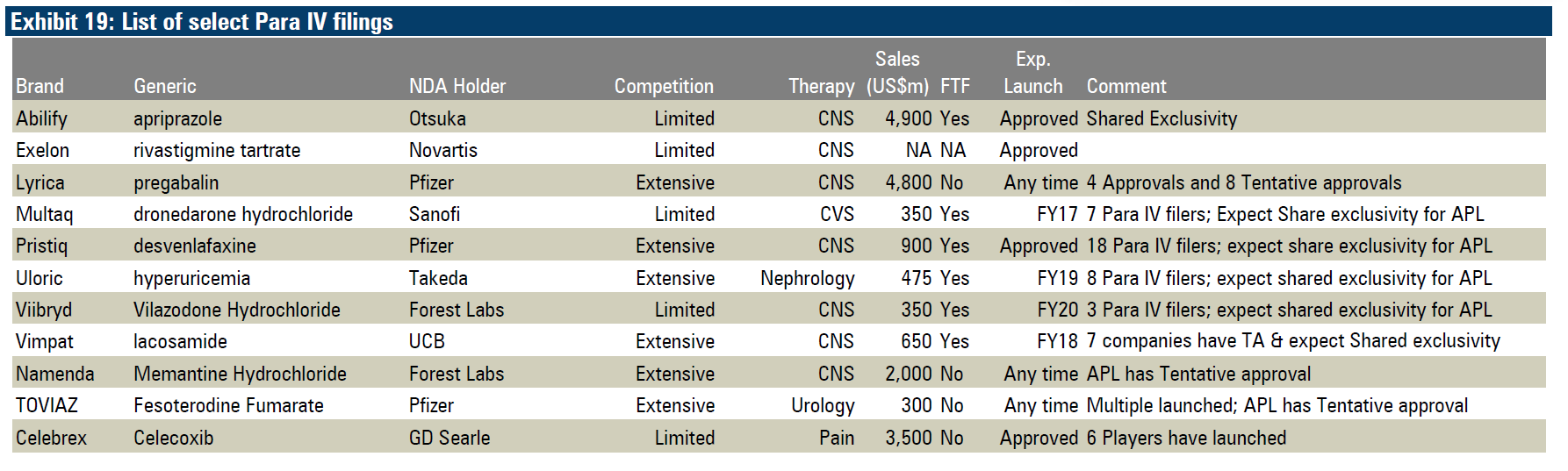

ALEMBIC PHARMA got final approval for Celecoxib(Celebrex) on 21st Aug 2015.

It has already received tentative approval for the same on 23 June 2015.

There are already 5 big generic players available for the same.

4 Likes

Celebrex sales of Pfizer before patent expiry were 2.9 Billion USD. So on the back of Abilify, Alembic gets another big molecule with competition from 5 players. Looks like a good year for Alembic is getting better.

Only fly in the ointment I find is that Alembic does not yet have a functional US front end and hence will have to share profits with its US marketing partner. But even with those restrictions Alembic should reap handsome rewards from both Abilify and Celebrex. Abilify figures will be reflected in q2 figures as per their guidance. Accordingly I think Celebrex will get reflected in q3 figures.

6 Likes

Thanks Hitesh for a lucid explanation of the impact of the latest approval.

The market seems to be considering abilify as an one time earning. Now another big approval in their fold the earnings should grow more homogeneous way.

Only thing left now is their own front end team in US, which they are already building. So their margins will improve going forward. This will ensure that the lumpiness in earnings due to the nature of generic business will reduce to certain extent.

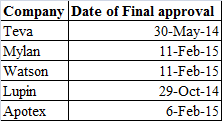

I saw on Pharmacompass that Mylan and Teva had an exclusivity period on this which expired on 2nd June. So Alembic is a late entrant in the game. This was not the case in Abilify, which was a day 1 launch. So it may be difficult to take market share. What do you think?

Other players are

Teva

Mylan

Lupin

Apotex

Watson

Looks like Lupin has already been exporting to US

Hi Rohit,

Please find below the date of approval for the generic players for gCelebrex:

The good thing about gCelebrex is its a pretty big molecule and still there are limited players in the market for it. I am not sure on the price erosion front but given limited competition, I dont think it would be more than 40 - 50%. May be we can go through Lupin concall and get the data if available.

2 Likes

On celebrex patent search, i got this on wiki

It is legally available in many jurisdictions as a generic under several brand names.

In the US, celecoxib was covered by three patents, two of which expired May 30, 2014, and one of which (US RE44048) was due to expire December 2, 2015.

On March 13, 2014, that patent was found to be invalid for double patenting.

Upon the patent expiry on May 30, 2014, FDA approved the first versions of celecoxib generic.

As per there recent concall, management was talking about launch of celebrex in December this year, [he was like we will be there on day 1 though he was not sure of date]

So he might be talking about this patent expiration.

US RE44048 patent

Issued: March 5, 2013

Assignee(s): G.D. Searle LLC

Patent expiration dates:

o June 2, 2015

TREATMENT OF PRIMARY DYSMENORRHEA, JUVENILE RHEUMATOID ARTHRITIS, ACUTE PAIN, ANKYLOSING SPONDYLITIS, RHEUMATOID ARTHRITIS

o December 2, 2015

Pediatric exclusivity

I think alembic will be targeting pediatric population.

I may be wrong at arriving this conclusion, seniors n fellow VPs ur views needed

Disc-invested from lower levels.

1 Like

Thanks Ankit.

As per this news article, pegs the generic market for Celebrex at $400 million.

“Lupin currently holds 14 per cent market share for Celebrex and expect $58 million sales from the drug with a 15 per cent market share”

However, off late, there are reports of adverse effects from generic Celebrex, read here. So it is debatable how easy it will be for Alembic to garner market share.

5 Likes

Hello drrakesh,

the newer patent was a mere extension sought by Pfizer. Refer this article for the full context of this.

Judge Allen invalidated the reissue patent for the same reason the Federal Circuit invalidated the original one — “double-patenting.” Pfizer had argued that, as part of the reissue, it had reclassified the patent in a way that made it eligible for a safe harbor that protects patents from invalidation on “double-patenting” grounds. But Judge Allen found that the reissuance process could not be used for that purpose, and the flaw was therefore “not correctable.”

4 Likes

Hi Rudra,

Price erosion is always a very debatable topic and except for the pharma companies, I doubt anyone else knows about it accurately (it’s an area where we should work on).

If you go through the article, it says ‘Currently there is a limited competition for the product and the company can conservatively garner sales of US $50-60 million in sales for the 50 mg capsules’ (would rather ignore what the journalists are writing and give more weightage to the analysts). The analyst is talking about 50 mg capsule while it is also availabe in 100 mg, 200 mg and 400 mg (http://www.accessdata.fda.gov/scripts/cder/drugsatfda/index.cfm?fuseaction=Search.Generics&Mkt=1). I still dont know how to interpret it.

You will always find reports on negative reports on generics (may be propagated by the innovators themselves). Not exactly sure how serious they are about gCelebrex.

1 Like

Interesting to see the Promoter Group of Alembic acquiring aggressively almost 20 crores worth of shares in the last month…price should be between 650 - 700…

“Pharma company Alembic’s promoter company Nirayu acquired 2.81 lakh shares of the company between August 20 and September 3. The mode of acquisition again was through the stock markets.”

Read more at:

http://economictimes.indiatimes.com/articleshow/48892616.cms?utm_source=contentofinterest&utm_medium=text&utm_campaign=cppst

3 Likes

In all possibility the news article refers to Alembic Ltd and not Pharma…they wrongly mention Pharma in the article. There are no insider transaction in Pharma (as per BSE/NSE) whereas there is some transaction in Alembic ltd (that too most likely inter transfer of holdings)

1 Like

Yes no insider buying in Alembic Pharma as per media reports.

Some info from ICICI direct report published recently. They give a target of 790 in 12-18 months

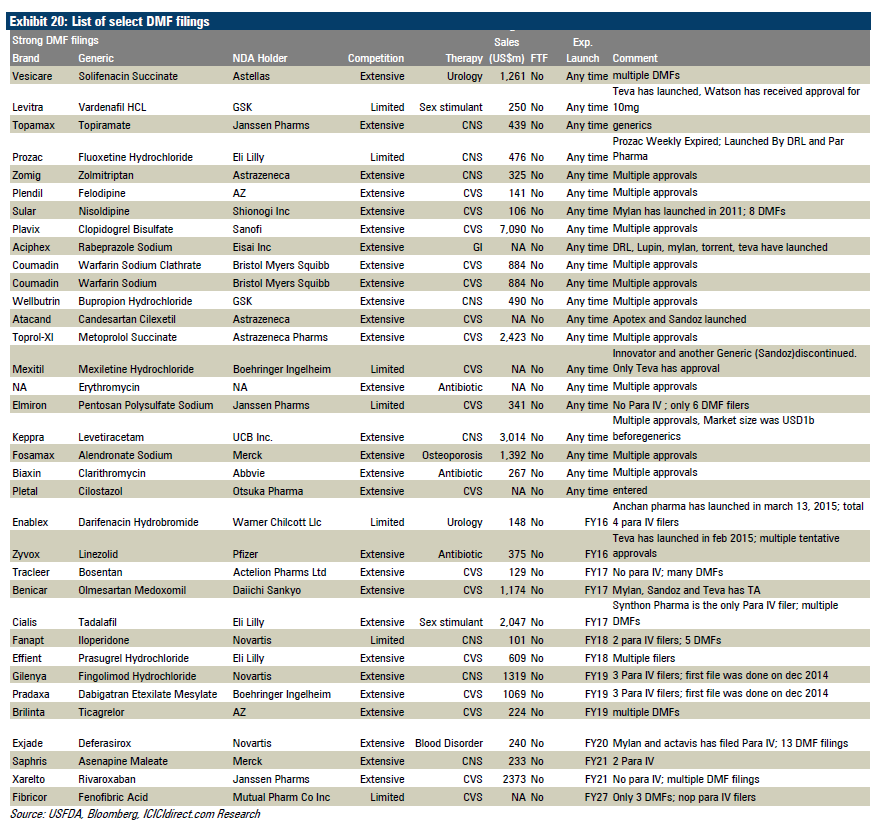

Below info on DMFs is something I had not come across.

3 Likes

Rohit,

I had put it in the excel which is there in the previous post. I have analysed all the DMFs filed by the company upto March 2015. Most of the time the company also files ANDAs for the filed DMFs. Their expected launches for FY16 and FY17 are also put in that excel.

5 Likes

Hi Ankit,

Yes, thanks for the awesome compilation. Its the most comprehensive work I have come across. I saw the file only few days back. To me Alembic pipeline looks to be the strongest among companies of this size, maybe better than many bigger companies too. I have made a mind map of Alembic pharma. Will upload it once I am done.

The valuations on trailing basis (46x) appear high compared to the fair PE band of 25-30 assigned to Alembic in the VP public PF thread earlier. Assuming a 30% growth for 1 yr, it comes to 35 times 1 year forward PE. This is definitely pricey but there is a good visibility for next 3 years.

Does anyone have an idea about the bioequivalence activities of Alembic? As per my understanding, one success here can be a blockbuster.

3 Likes

Hi Rohit,

We should also look at the company from forward valuation perspective and not just trailing. On trailing basis, yes it does look expensive but on forward basis it might not  . I think Q2 results will give us a fair idea about how the earnings will look like in FY16. For FY17, it all depends on the product approvals and off course how the competition pans out in Abilify. I am banking on two things in Alembic:

. I think Q2 results will give us a fair idea about how the earnings will look like in FY16. For FY17, it all depends on the product approvals and off course how the competition pans out in Abilify. I am banking on two things in Alembic:

- Their superior pipeline and R&D: I think the kind of R&D spent company has been doing is really commendable given its size.

- Establishment of front end in US markets: I think we can clearly see how Torrent has been able to leverage more from Abilify as compared to Alembic as it doesnt share its profits with the partners. Front end gives you more leverage on supply chain, pricing etc. They have hired three very experienced pharma executives for the US markets. Lets see how the execution is on that front.

6 Likes