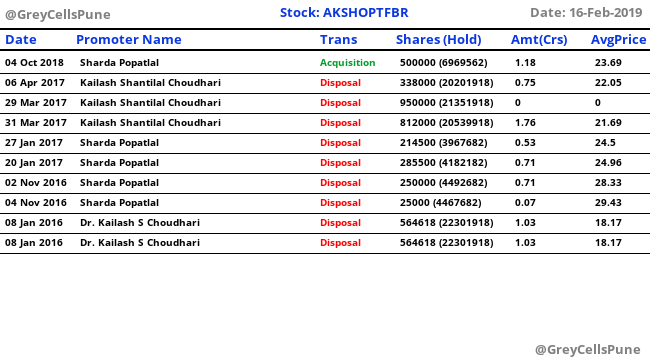

Had a heated discussion with Aksh optofiber mngt…liquidity is the main problem it seems.

They are not getting payments from buyers…and working capital crunch is hindering growth.

BSNL is giving huge contracts for FIBER cable, but no bank is willing to discount the bills of BSNL…so a small company like Aksh Optofiber is forced to forego orders…

There is a severe cash / liquidity crunch going on…NBFC / banks…kisi ke paas paisa hi nahi hai

BSNL and Bharat broadband Nigam are under severe pressure to speed up broadband network…it was also reported in Business line newspaper that the telecom secretary has issued memo to the heads of both these organisations for slow execution…

They are also under huge pressure from PMO to roll out quickly…

Thus they are releasing orders left right and centre…but they are not in a position to release payment…

Payment terms are 12+ months…for small companies no bank is willing to discount these BSNL bills…for larger guys they are charging 12-14%…

Ebidta margin is 19%…out of that 12-14% is taken away by banks…so no margin left for these orders…the bigger companies which are showing good profits now will not be able to show the same next year…once the BSNL bill discounting charges are taken into account.

Hence the Aksh mngt says they are adopting a prudent approach by refusing orders where payments are delayed and going for orders where payment is received in reasonable time.

My personal back of envelope calculations show that for Q4 too they may have a topline of around 150-155 crores…and EPs of around 60-70 paise…the FY19 EPs then would be around 3.10 rupees…not good enough to propel Aksh into a long rally but good enough to provide downside support

During AGM…when the shareholders chided the mngt for not being able to stabilize production of Opthalmic blanks vertical…the promoter Dr Chaudhary asked for time till 31st March…if they fail to make a headway by then, they are willing to sell off the Opthalmic blanks plant and utilize the amount for expansion of FRP rods capacity @Reengus plant.

In the present environment of severe cash crunch, I think the best thing would be to sell off that Opthalmic blanks plant and use the money to immediately ease the cash crunch or to go for capacity expansion for FRP rods

Data SET Mar 2016 ->Mar 2017->Mar 2018->Sep 2018

continuous increasing of Inventories 2016 onwards 24.02 -> 43.8->47.53->64.69

continuous increasing Trade receivables 141.51-> 155.65->212.67->227.07

continuous increasing Loans n Advances (except in 2018 )95.61->101.78->120.44->109.58

continuous increasing Borrowings 88.21->131.20->230.01->213.97

Occasional Dividend Payout

high cost raw material Data SET Mar 2014 ->Mar 2015->Mar 2016->Mar 2017->Mar 2018

Material Cost % 58.27% ->62.24%->59.72%->66.69%->65.25%

inconsistent and varied Sales growth -> -5.56% ->58.28%->24.82%->5.31%->27.4%

Disc : Not holding watching from couple of Quarters but Still not convinced about the Numbers and story

It appears that the company has some issues in terms of cash flow mismatch during March 2019. This period also coincides with the change in rating agency from ICRA to CARE. There is a significant possibility that there were genuine concerns which the company did not address to the rating agency and hence the potential downgrade by ICRA was avoided by not cooperating with them.

CARE ratings also downgraded the ratings to D. I think the company needs to be watched carefully to see how their investments pan out and if they manage to pull out of the mess.

Note that they had also invested in the optical lenses part, whose performance is till unknown.

If two rating agencies are calling it quit, there got to be significant risk. For anyone intending to bottom-fish, I think the potential for capital loss is significant. Trade with caution. On the flip side, the rating agencies seem to do their work

Disc: I have a tracking position in Aksh and a significant position in Sterlite tech. Prepared to have a write off on Aksh.

All the independent directors have resigned from the board…the MD of Aksh Stayendra Gupta resigned on the day of AGM…a few senior people have left… promoters are under penalty by sebi and promoters and aksh banned by sebi from accessing the stock market…severe working capital crunch in indian operations…dubai operations not upto the mark, continue to make losses…mngt still not able to appoint independent directors…opthalmic blanks plant is non functional…and finally stock price is down at the last support of 5-7 rupees…and it looks like it may go lower and lower with no near term prospects of recovery…

I exited in March 2019…from 21/22 rupees price onwards…average exit price is around 20 rupees. Buy call was @14.20…stock went up to 46 but i continued to stay invested…forced to exit at a marginal profit or almost no profit…and thank God i did not hold the stock all the way down to 5 rupees…its always better to exit at the final / strong exit signal.

Thanks @phreakv6! It was one of the counters that I had some nominal investment (from 2016-17 times when everything was booming and brokers used to peddle stock recos). I remember reading your comment in this thread and exiting after a few months after booking loss. Just goes to show investment in small caps is a risky bet and need to be extra cautious if there are some signs of red flags.