As capex is over FCF will improve with increasing profits… e-governance business is also at break even…whole opthalmic lense story is still to play out which is a very high margin business with less competition in india…

2 Likes

Import duty hike on Temecom equipment, how this can affect on Aksh opti. Any view?

1 Like

Aksh declared results today -

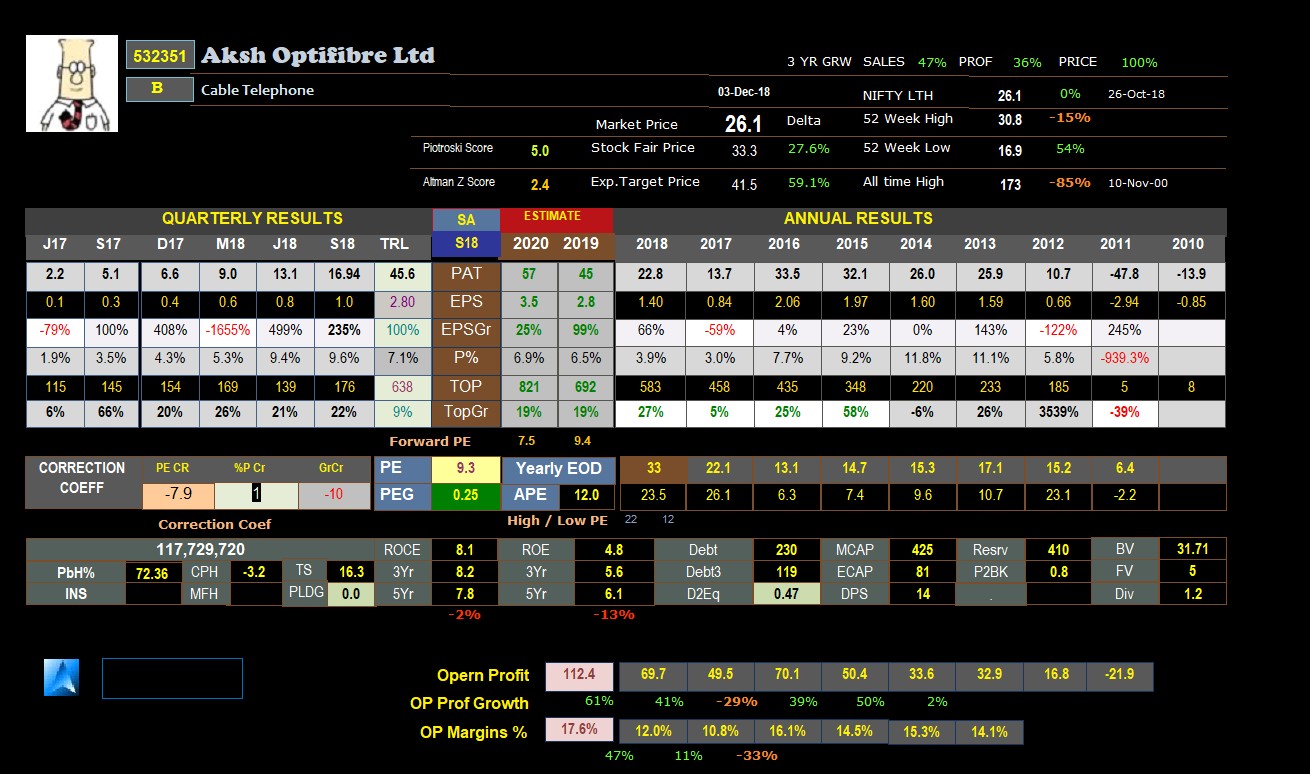

Revenue - Rs. 178 Cr. vs 141 Cr. in Q1 & 145 Cr. in Q2’18

EBITA - Rs. 40 Cr. vs 32 Cr. in Q1 & 16 Cr. in Q2’18

EBITA Margin - 23% vs 23% in Q1 & 11% in Q2’18

PAT - Rs. 17 Cr. vs 13 Cr. in Q1 & 5 Cr in Q2’18

PAT Margin - 10% vs 9% in Q1 & 3% in Q2’18

Improvement in performance is quite easily visible in these numbers. Key would be - with majority of capex behind, sustenance of such numbers for subsequent quarters. Growth drivers seems to be in place (5G, etc.), the key question is - can the management deliver with transparency. If there is going to be a concall, pls. suggest

Views on negative risks and alerts would be great to hear about.

Disc - Invested

3 Likes

Let me just recount the positives of Aksh

-

Topline and bottom line have improved…the company is set to do a turnover of around 800 crores in fy 19

-

the operating profit margin is now @22%…which is quite good.

-

the input prices are going down while the demand for optical fiber cables is going up…hence the operating margins may go up further

-

the services sector losses which were eating up the yearly eps by around 50 pasie are almost gone.

-

having a substantial export component and almost half of manufacturing capacity outside India, the company benefits from rupee depreciation…for H1 the unrealized forex gains have been around 8.5 crores…if the rupee stays down till march, then the forex gains itself can add around 50 pasie to the yearly eps

-

the china capex too has been completed on time…now only the dubai capex is left. Dubai may be completed by end of December and after 3 months of trial run, the full impact of massive dubai capex will be felt from Q1 of fy20 onwards.

-

The Q3 eps may be around 1.3 to 1.4 rupees as the mngt has told that Q3 is the best quarter fortheir sector. That sets Aksh on course towards 4.2-4.5 rupees eps for fy19…and maybe 6 rupees eps for fy20 once the massive dubai capex kicks in. Thus Aksh is now a value buy, the improving earnings reduce the downside risk.

-

In the AGM, the investors requested the promoters not to subscribe to warrants but to buy the stock from open market below 30 rupees…the promoters have started making purchase as per the declaration filed with exchanges…as and when the buying by the promoters goes up, the float will decrease and stock becomes more bullish. Till significant promoter buying comes in, Aksh may continue to be range bound in a weak market.

5 Likes

while coming to the negatives…

the recievables continue to be very high as the mngt has said that historically this has been a feature of the sector. The mngt has taken certain initiatives (reorienting the business model0 which may bring down the recievables …they have said that as and when the improvement is reflected in the numbers, they will make an investor presentation.

I think, the recievables position will improve from Fy20 onwards…as business model chages take time to get reflected in numbers…

2 Likes

Check out @MoneylifeIndia’s Tweet: https://twitter.com/MoneylifeIndia/status/1059724822421426176?s=09

Aksh is slowly getting the attention that it deserves. There is very clear earnings visibility and uptrend…this stock will not stay ignored for long…sooner or later, it’s bound to fly… EPS for fy19 is expected to be 4-4.5₹…next year around 6 ₹ EPS…@27 ₹ stock price, it’s a steal…a very good deal for value investors, growth investors and momentum players…

Good fundamentals and bullish technicals…

Aksh claims that 70% of the raw material cost is in-house manufactured. but looking at the financials between peer to peer comparsion ( Aksh and Sterlite tech gives me a different story).

Sterlite tech RM cost is between 35-40% where Aksh RM cost is minimum of 58%.

source: screener.

Dics. Invested with minimum tracking position.

Do anyone have any insights on why Aksh RM cost is very high.

Do anyone has any visibility of Order book of Aksh for each of its product lines. I was reading the Sterlite tech investor presentation and it does cover extensively and the status of its order book. wonder why Aksh hasn’t published anything about its order book in its investor presentation.

Mehnazfatima,

Pleasant surprise to bump into you here, as I benefited a lot from you about sugar in the last cycle. While I’m bullish about optical fiber’s potential, going through this thread fully, Aksh really worries me on the corporate ethics front and if us retail investors could really benefit, especially after @phreakv6’s insights.

I’ve decided to not even have a tracking position, but do my due diligence for now, think till Lok Sabha elections there’ll be enough buying opportunities.

Thanks a lot for the great thread.

1 Like

sir could please tell What is the source for this ??? Thanks

This is my stencil I have designed mainly taking data from Screener.in . It is an access database linked with many external excel files … for EOD, 52W high Low etc

Nice comparative study.

Issue with Aksh

- High receivables

- Low return ratios

- Very low Promoter holding

I consider #1 & #2 transient in nature. They can be temporary and be improved.But #3 is a huge red-flag. Every one knows that this industry has lots of potential, then why not the owners who have the insider info not hiking their stake, why they want to give away 73% of the pie away?

Q3 Highlights !

The good :

On Year To Date Basis Company achieved a Total Income of Rs 458 crore, as compared to Rs 423 Crore in the corresponding period previous year.

Company maintained healthy EBITDA margins of 22% on YTD basis, as compared to 11% previous year.

Higher PAT recorded with YoY 184% increase on YTD basis.

During the quarter gone by the Company achieved quarterly Total Income of Rs 140 Crore and EBITDA of Rs 26 Crore.

EBITDA margins for the Company stood at 19%, as against 13% in the corresponding quarter of previous year.

Profit after Tax at Rs 9 Crore reported an increase of 35% as against Rs 7 Crore in the corresponding quarter in the previous year

Promoter holding increased from 27.64% to 27.95% in the quarter gone by.

The Bad :

Increase in inventory by about 22cr QoQ.

From MD : " We are focussing on improving the overall operational efficiencies

and consequently improving the cash flow cycle with lower inventory level. However, due to postponement of deliveries of few orders in hand by few customers and temporary slowdown in the industry, there has been a momentary decline in the quarterly turnover"

Is there a slow down in the industry ?? - As per MD.

Can we trust their words on future optimism.

The press release says that the fall in topline was on account of clients not taking delivery of goods before 31st December. And hence the increase in inventory by 22 crores. If this gets added to Q4 turnover, then Aksh should be doing 180-200 crores topline in Q4…hence an EPS of 3.2+ rupees for FY 19 is within reach.

1 Like

As per news item in Bloomberg, China has started the optical cable procurement for 105 million fibre kilometres. And if China is into 5G, the US, Europe and Japan too cannot afford to be behind China in 5G.

I think this will spark the next bull run in optical fibre cables sector.

But as of now it looks like the Aksh mngt may not be able to capitalise on the bull run in FIBER optics cables. They just do not have the required drive and energy and skills for that.

This year Aksh may again do a topline of around 620-630 crores, which is not such a big deal considering that we have incurred such heavy CapEx. In the AGM we were promised a topline of 700-800 crores for this year and again the MD Mr Gupta has a ready set of excuses for not meeting the targets. This is the routine they follow everytime…fob off some excuse or the other to the investors. This sort of thing never happens in case of other optical cable manufacturers.

The next thing is that …as per the Q1 press release, the next round of CapEx in Dubai for 4 million kilometres of fibre was supposed to be over by January 2019. In the AGM, the promoter Dr Chaudhary assured that the CapEx will be completed as per schedule and after a trial run and production stabilization till March 2019, Dubai CapEx will start adding to the EPs from Q1 of fy20…but now it seems the CapEx will be completed only at end of Q1 of fy20…and we don’t know how long they need for trial run and production stabilization. Again, this is the pattern followed by Aksh which has not completed any CapEx in time.

Then there is the issue of CapEx already completed…the Daman plant…the Mauritius plant…the China plant and the Opthalmic blanks plant. Apparently, all these have not contributed much to topline. So is the CapEx really undertaken or has the money been siphoned off?

The promoter who looks after the Dubai operations has disappointed time and again. So far Dubai has not contributed anything to the earnings. It continues to be a drain on consolidated earnings. Even the CapEx is getting delayed and delayed. It makes one wonder as to whats going on in Dubai.

And finally, the board of directors have decided to promote Satyendra Gupta as MD…as a reward for his non performance and failure to ramp up the production…failure to win good orders…failure to ensure timely completion of CapEx…failure to operationalize opthalmic blanks plant…failure to communicate with the investors and keep them informed…failure to make the services sector profitable…etc etc.

In conclusion I can only say that the combination of a medical doctor as promoter and a accountant as MD is just not able to steer Aksh well in these competitive times. While all other optical fibre cables makes are coming out of fantastic results, Aksh doctor - accountant combo only comes out with pathetic excuse of a performance.

This is one company where nobody does anything positive…neither the promoters…not the MD…and the spineless directors just rubber stamp their approval to anything. The shareholders should first get rid of the MD and kick out the directors…and get a new aggressive mngt

This is a company where the promoters have no skin in the game…they are just not interested enough to run it properly…they have a very low holding of around 28%…they keep selling their shares…they announce 2 crore warrants @ 42 rupees but fail to subscribe to the warrants …they do not heed to the repeated pleas from the investors to buy shares from open market to increase their holding and show confidence in their own company…no wonder the market does not like Aksh Optifibre.

The rally started in June 2016 from 14…and after two and a half years, the share price is again headed towards from where it all started. The next downside target for Aksh is 15 and then 12…

7 Likes

What happened to their opthalmic lense vertical? Management hasn’t uttered any single word regarding this…

I agree. This is a serious issue. Do such expansion plans come only during bull phase of the market?