Ophthalmic lens production coming online from March 2018. And production capacity scalable to 3 times based on market response.

OF capacity - 4mn FKM per annum coming online from Feb 2018 in Dubai (roughly guessing because it must have been commissioned at the end of Jan according to post-q3 press release). This will take the OF capacity from 3mn FKM to 7mn FKM. 133% capacity expansion.

OFC capacity – 0.7mn FKM per annum in Mauritius, 1mn FKM OFC capacity in Silvassa must be coming online in few months (most probably in the beginning of Q1 2019).

FRP - 0.8mn Km per annum FRP in China (must be coming online in few months). This will take the overall FRP capacity from 2.6mn Km (1.2 mn Km in India + 1.4 mn Km in Dubai) to 3.4mn Km. That’s 30% expansion in capacity.

Historic analysis of all fraud and chore management are testimony to my apprehensions-low (bellow 30%) holding.See what is happening to Sintex Plastic/Sintex industries. .

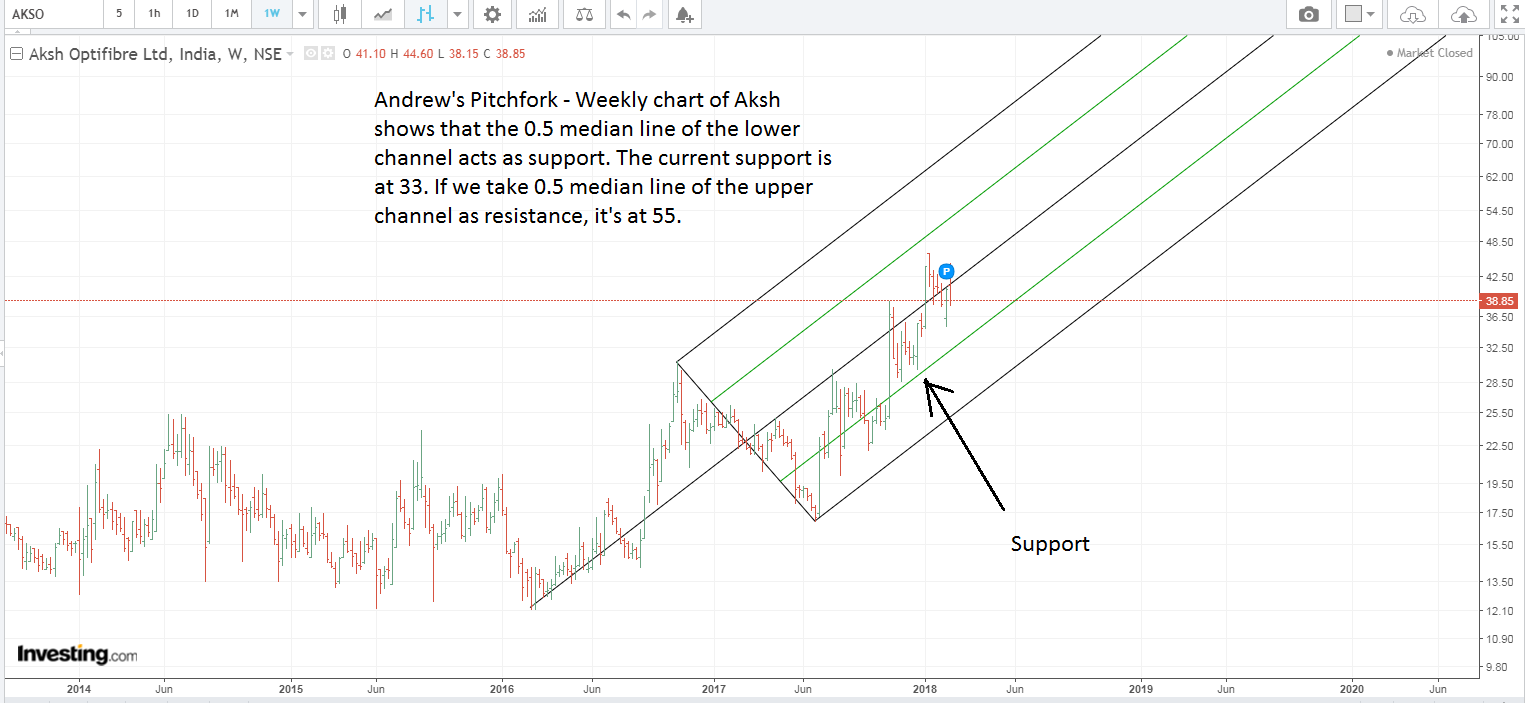

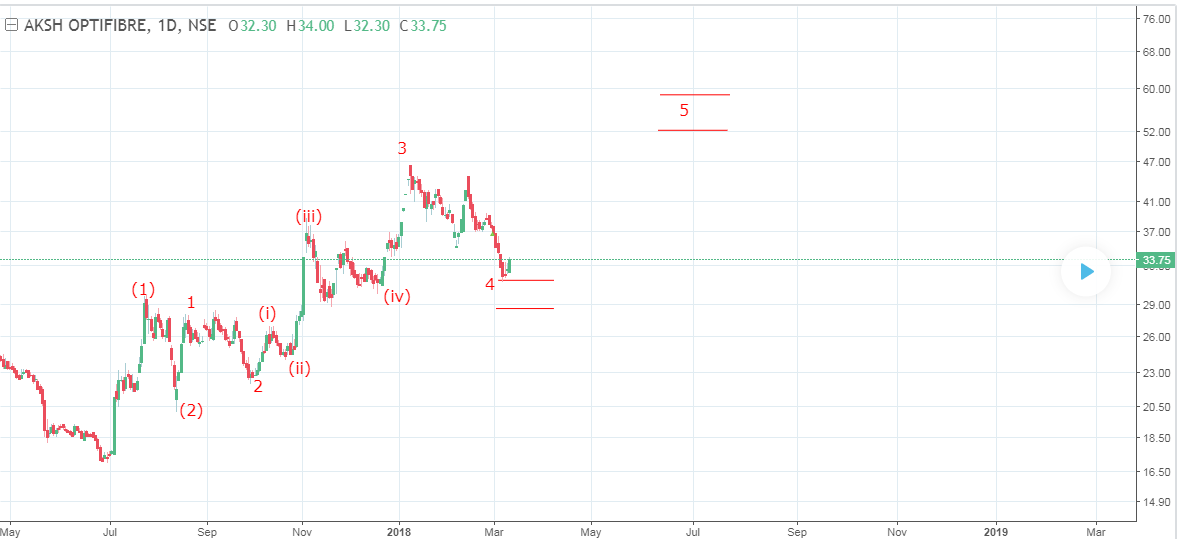

Aksh is following a pattern. It gave breakout the last 2 times when it formed symmetric triangle pattern. Now it’s forming another symmetric triangle. Will it again give another breakout? We should keep monitoring the daily chart.

Has the result date being announced yet for Q4? I think the Q4 results will be slightly mooted because of expenses from capacity expansion going on,would appreciate the views of forum members on the same.

Aksh has been a promising stock since quite a few years. Now it’s for the mngt to deliver on the promise. If the mngt wants, the company can definitely show a good eps. It’s as simple as that.

The mngt has been meeting institutional investors in Mumbai and Pune. The promoters too have got warrants for 1 crore shares @42. All these give me hope that Q1 or Q2 onwards, the eps will show a good / big jump.

I too have positive views for the management and their clean past records. After the recent correction, I might add more of Aksh to my portfolio. Happy investing.

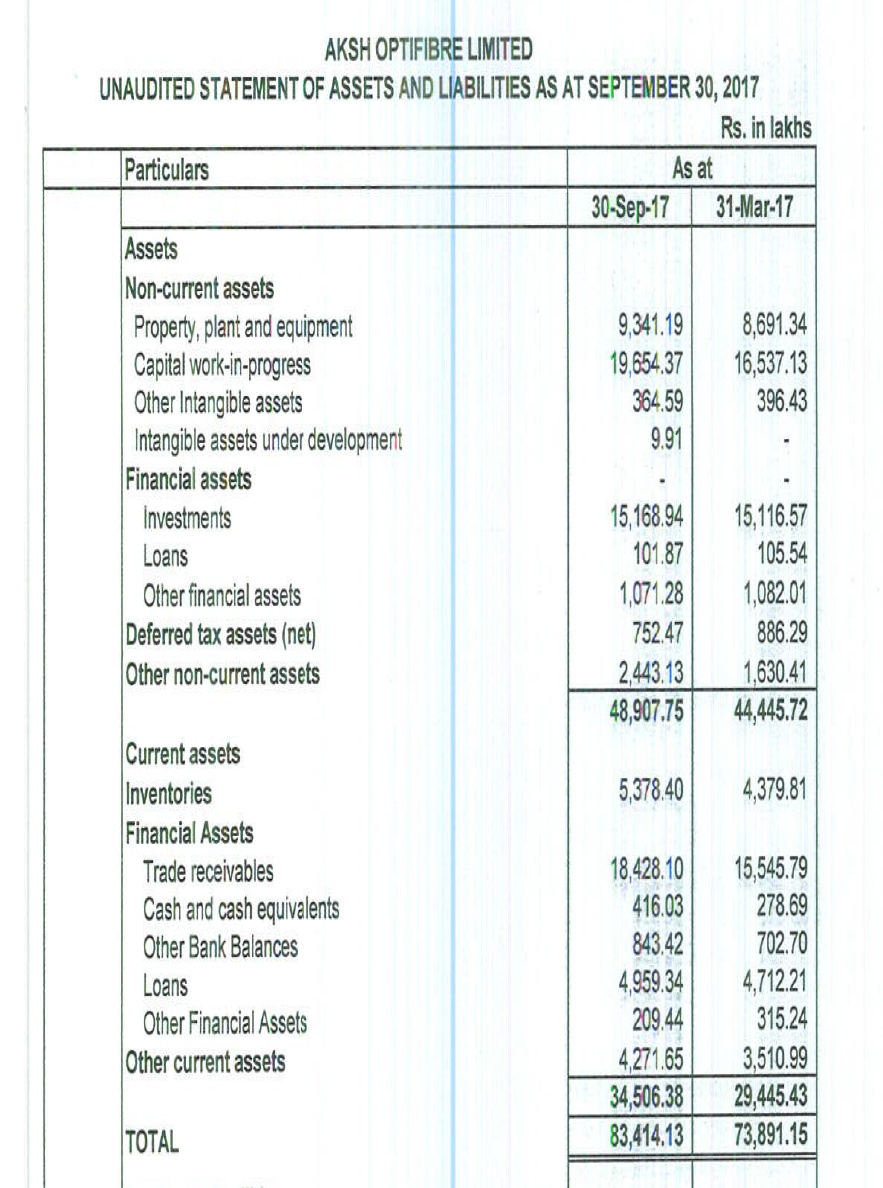

I went through last few months of posts on this thread. There seems to be great enthusiasm about the stock’s future prospects. Nevertheless I am troubled by high receivables of the company. Particularly troublesome is increase in receivables on Sep 17, as compared to March 17.

Thanks @Agarwala for pointing it out. I checked ARs from 2012. Receivables keeps increasing - from 66 cr to 184 cr. It never went down even for one year. It sure is a red sign.

Sterlite and HFCL have come out with very good Q4 numbers…they have shown an increase in both topline and bottomline…Birla cables has shown a turnaround in Q3 itself and has nearly doubled …now its for the Aksh mngt to come out with good Q4 numbers…minimum eps expected in Q4 is around 50 pasie but in the present environment that may not be enough to excite the market players…a better eps would be above 75 paise for Q4 and a positive commentary by the mngt with regards to topline for fy19 and fy20…

Aksh has disappointed the investors for too long…if the mngt presents a not so good result, then the investors may dump it in favour of any of the other three fibre optic cable makers which have come out with good results…

Looks like Aksh is now at an “inflection point”…it has to perform now or be left behind in this bull market…AKSH mngt pl stop playing your games and wake up!!!

All data points suggest that Aksh Q4 numbers should be blockbuster and Q1 FY19 numbers will put the company in a completely different orbit all-together. All the data points regarding capacity expansion and insatiable demand for OFC are in public domain. In my humble estimate, this sector is going to be the market favourite over the next 2 years as no other sector can boast of such strong tailwinds globally as well as in India. I don’t see any better way to play the data and internet boom in the listed space. The conference call of Sterlite Technologies was extremely insightful and gives a clear indication of the strong runway in this sector thanks to 5G.

However, in this sector, Sterlite Technologies has clearly positioned itself as the most innovative company (and more importantly as a one stop shop) and is beautifully positioning itself to capitalize on this boom. So, Sterlite Technologies valuation will always command at least 40% premium to other companies in the same sector.

Like you right said, the management has to get its act together really fast. Q3 numbers were satisfactory, to be fair to the management. However, Q4 and Q1,FY19 numbers will reveal more about the trajectory of the company. In my humble estimate, with all the capacity expansion coming onstream and the X-Factor in terms of the Lens facility, the company should end FY19 with at least Rs. 40 Crore.I for one, wont be surprised, if it commands a market cap of at least Rs.1600 Crore post q1 results, when the dense fog lifts from its story. Keeping my fingers crossed and hope the management delivers.

You will be amazed if you know how much EPS Ophthalmic lens vertical can generate (Tip by Abhishek from MMB)

Aksh’s plan is to start off with producing 2.5cr pairs of lenses per annum. Based on market response, they can scale the production to 7cr pairs of lenses from the current capacity itself.

Aksh’s lenses are of grade A, which is better than what India is importing from China, but still planning to sell these at affordable prices to grab the market.

A pair of lens may cost more than 1000rs. But taking a conservative price 500rs per pair.

Total revenue = 2.5cr * 500 = 1250cr.

At 20% margin, PBT will be 250cr.

Assuming 30% tax, PAT will be 175cr.

For PAT 175cr, EPS for an year will be 10.76.

If we calculate P/E for Aksh at CMP using the EPS from the Ophthalmic lens vertical alone, it stands at 3 point something.

The above calculation is for production of 2.5 cr pairs of lens. What if the market response is good and Aksh starts producing 7cr pairs of lens per annum.

Then EPS will be 30rs per year. And P/E will be 1 point something.

Now imagine what will happen when EPS from OF, OFC, FRP, e-Mitra adds up.

Aksh started commercial production of Ophthalmic lens from the beginning of March. So, Q4 result should have 1 month of revenue from this vertical.

Q4 results should indicate how well this vertical is doing. If it goes as per the above calculation, then sky is the limit for Aksh’s market price.

Fingers crossed.

I believe taking 2.5 cr in to consideration for calculation implies 100% utilization. Is there any figure available about the market size for this product. Probably, in the beginning - the utilization of the capacity might remain below 50 odd %…This is just my personal opinion.

I work in Telecom and have been hearing for more than 1 yr. that 5G network relies heavily on optic fibre

All the best!

I will be quite satisfied if they make a profit of 15-20 rupees per pair of opthalmic blank…That itself would give Aksh around 50 crores of profit in the first year

How did you come up with the Rs.1000 for a pair of lens? Are you sure a supplier can sell it at that price? Am seeing Rs.100/piece sort of prices on Indiamart

Who are the competitors for the lens product? I see lot of unorganised manufacturers doing this? Is this a commodity anyone can manufacture with machines imported from Germany? What margins can you expect in that case?

What is the current OFC and OF capacity and utilisation of Aksh? Sterlite tech has 30million km which will be 50million km of OFC capacity next year and 15million km of OF capacity. Sterlite Tech’s utilisation is around 70% levels and is expected to go up to 85-100% next year.How does Aksh compare?

Trying to understand if the bullishness on this counter is due to technical indicators alone or if its fundamental as well.

Disc: Invested in Sterlite Tech during demonetisation

Look it up in Alibaba for the wholesale price. Most of the Chinese suppliers sell a pair for $0.50 to $10. That’s roughly 34rs to 670rs.

I took the higher range since the quality of lenses produced by Aksh are A grade (as per the corporate presentation and AR2017).

According to the corporate presentation, 95% of the Indian demand is met by Chinese imports. China exports AB, B grade lenses to Indian market.

Aksh’s plan is to shift Indian market to A grade lens at competitive price.

Indian Optical lens market is estimated at 7 lac lens pair per day with no significant organized player in Indian market.

That’s 25.5cr pairs per year. Aksh’s plan is to start with 2.5cr pairs per annum. Roughly 10% of the Indian demand.

Not sure about the competitors. I also see a lot of unorganized players. Even according to Aksh’s AR2017 and corporate presentation, the demand is mostly met by unorganized players and Chinese imports.

OF capacity

Bhiwadi, India - 3Mn FKM

Jafza, Dubai - 4Mn FKM (commissioned in Feb 2018) will reflect in Q4 results.

Total OF capacity = 7 Mn FKM vs 15Mn FKM of Sterlite Tech.

Total number of shares outstanding of Aksh is 16.26cr, whereas for Sterlite, it’s 39.83cr.

So, 7 Mn FKM of Aksh is equivalent to 17.5 Mn FKM (vs 15 Mn FKM of Sterlite) if you take Sterlite’s total no. of shares outstanding.

OFC Capacity

Bhiwadi, India - 9Mn FKM

Silvassa, India - 1 Mn FKM (should have been commissioned in April 2018 according to Q3 press release)

Mauritius - 0.7 FKM (April 2018)

Total OFC capacity = 10.7 Mn FKM vs 30 Mn FKM of Sterlite Tech.

So, 10.7 Mn FKM of Aksh is equivalent to 26.25 Mn FKM (vs 30 Mn FKM of Sterlite) if you take Sterlite’s total number of shares outstanding.

FRP Capacity

Jafza, Dubai - 1.4 Mn FKM

Silvassa, India - 0.4 Mn FKM

Reengus India - 2 Mn FKM

Jiangsu, China - 0.4 Mn FKM (April 2018)

Total FRP capacity = 4.2 Mn FKM

Margins from FRP is much higher than margins from OF and OFC.

No, it’s not only due to technical indicators. You can see that huge additional capacity coming online in Q4 and in Q12019. Plus entering into new line of business (Ophthalmic lens). So, it’s fundamental development as well.

Disc: Invested in Aksh and waiting for Sterlite to reach my buying range.

@PE_Ratio

I agree that they have started production in March but do you think that they have enough order book in advance to generate revenue from this vertical?