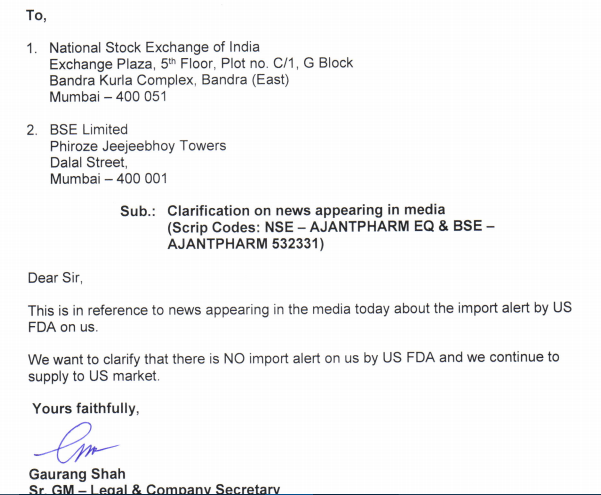

Unlike Divi, good to see company’s officials coming out to defend the FDA news -

“Speaking to BloombergQuint a company official said the import alert has been made for its sildenafil citrate tablets, which is the generic version of Viagra. “We do not sell the product in U.S. at all. It is only sold in India and emerging markets,” the spokesperson said.”

You’re probably curious what are these names doing on the Ajanta thread. Well, all these products have received Import Alert of 66-41 type (i.e. Detention Without Physical Examination of Unapproved New Drugs Promoted In The U.S.) at one or other point in time. One such product is Kamagra from Ajanta (and Ajanta is not even selling it in the U.S.).

Comparing the above with Wockhardt Ankeskleswar/Aurangabad plants and/or IPCA Patlampur/Ratlam/Silvassa plants Import Alerts of 66-40 type (i.e. Detention Without Physical Examination of Drugs From Firms Which Have Not Met Drug GMPs) is an irresponsible reporting. Wrong and grossly exaggerated.

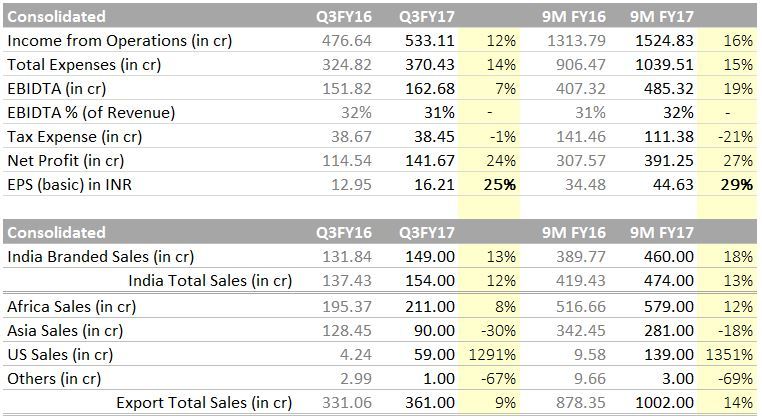

6 ANDA filed in FY17 till 31st Dec 2016 (was 3 till 26th October 2016)

US - 12 Products commercialized (was 9 in Q2FY17)

Team size of 800+ scientists (was 750+ in Q2FY17)

Guwahati (Assam) – First phase commissioned, 2nd phase by Q4 FY18

Dahej (Gujarat) - Commercial operation from April '17

R&D spending increased to 8% of operating revenue (with the objective of increasing the ANDA filing pace in US)

De-growth in Asia and lower growth in Africa was mainly due to currency devaluations and forex scarcity in select geographies, which continue to pose challenges and resulted into suboptimal business.

Commenting on the results, Mr. Rajesh, Joint Managing Director said:

“… The external factors in emerging markets continue to pose challenges resulting into sub-optimal business. However we are pleased with the remarkable ramp up of our US business which has posted great results for the quarter.

Going forward, we continue to focus on our key markets and therapeutic segments to drive the growth.”

Reduced growth in Asia and Africa ? Currency issue.

Domestic sales growth might have affected due to reduced hospitalisation and postponement of elective cases . My scuttlebut shows almost 10% reduced hospitalisation during last quarter after demonetisation.

US showing good growth from last 2 quarters.

Total ANDA approvals 16.

Commercialised 3 more products .total commercialised: 12 ( 9 till q2fy 17)

Filled 3 more ANDA.Total ANDA filled till q3:6.

Target is to file 8 to 12ANDA /yr.

Increased focus on R&D:

Added 50 more scientists during last quarter. Total scientists 800+.

R& D spend during q3: 45 crs.(8.5%) @lustkills your expert comments please.

US business is growing rapidly but it is still too small and unlikely to be as profitable as EM business going by the margins that other US centric pharma companies are earning. EM business is having some growth issues now. Overall, I feel growth in US may not be enough to offset slowdown (in growth) in EM causing overall growth to come in at mid teens over the next 2-3 years. While that’s a decent number, at over 30 times earnings, market is expecting more. IMO should sell for about 20-22 times earnings.

this Q, if you exclude other income and exchange gains, profit growth is at 12%.

For USA growth to happen…one is needed to start investing heavily in R&D . All Generics in USA have started struggling. Only way to show growth is in specialties and that will take time.I agree it is overvalued

All good things have to come to an end. There are good signals that growth is slowing down. Again for some strange reason 52 week low for Ajanta happens to be in Jan/Feb time frame for the last 4 odd years. Can the management pull off another daredevil feat-not sure. market expectation is clearly very high. EBIDTA is still good around 25%-30% growth. I guess need to pare down my holdings.

Thats correct. Also, the high base effect will come into play for any company.

I have a general question (not necessarily related to ajantha) for senior investors here. Its easy to say buy right and sit tight. But most of the times, you are forced to sell due to overvaluation and in some cases due to growth slowing down. How does one handle such a situation ?. Its not easy to completely exit and reinvest the sale proceeds in a different company. ( especially in a market like this where everything is overvalued/priced for perfection). So would it make sense to stay invested if the company is at least growing. ( not necessarily at the old growth rate)?

You can sit tight only if you buy right. Most of the time that’s not the case. If you think your portfolio is overvalued then just sell and park your money in liquid funds. Keep looking for opportunities so you will be in a position to buy when you find one. Quiet often, after you sell, market will keep going up and that’s when your fear of losing money can turn into fear of losing out on making money. That’s also when your valuation model and your discipline will be tested. If you can sit tight (this time on cash), an opportunity will come where you can get back into market. Returns on such moves will be very high. Sometimes the same stock you sold will drop under its own weight without any apparent reason…

Excellent point Yogesh.Even if you buy right when the correction happens due to overvaluation or otherwise you tend to lose chunk of your profit. The point about liquid funds- do not understand. Is there anything we can park for a short period?

Stock slowing down due to slowing growth -classic example Page. I agree that sitting tight on cash will definitely give us those 52w low opportunities or any sudden negative developments.

I am referring to liquid debt funds that provide you fixed returns and do not drop in value in most cases. You can use debt mutual funds to park your money while you wait for stocks to correct. There is one ETF called LIQUIDBEE that trades like stock so you can buy and sell that on the same day you sell/buy your stock and both transactions will settle in the same settlement cycle. As an exception LIQUIDBEE attract no STT and other fees and many brokers charge no or low commission for this ETF. It always trades at 1000 and you earn returns as dividend units. since returns are paid as dividends, these are tax free and overall you earn about 4-5% tax free.

Thanks for your response. I shouldn’t have used buy right phrase. I meant to say, buying something that has a great past track record and has some sort of a earning visibility. And what to do when earning growth slows down…If one looks at some great companies like asian paints, they have had some bad phases at some point in time. But eventually they came back. ( But again asian paints may be a bad example considering the nature of the business).

Yes liquid debt fund is always an option and I am already using it. But its very difficult deploy money in a new stock idea especially when the portfolio is large.