A good primer on how to apply the Percentage of Completion Method to recognize revenue.

4 Likes

came across this interesting tweet and following replies

2 Likes

The June 2018 report is also out and can be accessed at

“http://www.gera.in/media-room/pune-residential-real-estate-reports”

We believe that the Pune residential real estate market as a whole is at a cyclical bottom. The access to capital that used to be easy earlier and also cheap has been severely curtailed with the 70% rule and new project launch guidelines under RERA. There are many projects which are struggling to complete construction leading to stress in a significant portion of the unsold inventory - hence the addressable market for new customers has shrunk even further. The % of unsold inventory is at 4.5 year low - a level that was last seen in Dec’13.

Best

Bheeshma

Disc - Me and my team collect and collate the data which goes into the making of this report

5 Likes

But, the Real estate mkt was high in Dec 13 I guess- overall. Last time real estate prices were down was 2003-04. Can you pls compare with that data.

In Pune, residential real estate prices peaked at some point in 2014-2015 due to over supply. I dont have data going as far back at 2003-2004. As of now, the trend that we are seeing in pune is that of small sized apts being launched at lower prices. The volume in this segment is good with 40-50% + inventory being liquidated in the first 4-5 weeks of launch and the remaining being liquidated in the next 5.

The total value of unsold inventory in Pune is roughly ~40k cr and every year we have 75k-80k units being sold - so currently Pune has about 12 - 13 mths of inventory left on an average.

This doesn’t take into account lakhs of middle class who own 2 apartments but have 1 family. The extra apartment doesn’t count in inventory but is available for sale in many cases.

Hence the right figure should be actual demand supply in the real estate brokers office!

These numbers are not for projects on resale , but ongoing under construction projects. The report only tracks the ongoing construction activity and not the secondary market. 12 - 13 mths stock left is only for the current under construction projects in various stages of construction.

Over time however, as units get constructed, sold and put on rent - to that extent the supply of homes will always be on a rise and there will be pressure on prices if population employed doesn’t not keep up pace with the overall growth rate in inventory.

The last one year has been very volatile for the real estate industry esp residential. Some of the changes that i have seen are as follows

-

Focus more on collections rather than volumes across the board. Cash flow from operations has increased sequentially for most real estate developers and changes in working capital have reduced coupled with paying down of debt. This suggests that developers are strengthening their balance sheets and are more concerned with their basic survival rather than growth.

-

Loading has increased. Developers are producing smaller apartments with more loading. This increases the construction cost as more walls need to be built. The avg apartments per floor has gone up from 4 to 6 per floor.

-

Newer Societies now have more residents than before. This has created demand for small shops and offices in the local area to serve these increased catchement size.

-

The more number of residents has created the need to give more amenities as maintenance costs can now be distributed better.

-

Construction cycle times have reduced as ticket sizes have come down due to smaller apts leading to faster collections. As a result, customers dependence on home loans has reduced dramatically. This a big change.

-

Developers are moving to annuity models to derisk their business as part of the product mix. This gives stability to the business as regular cash keeps flowing in.

-

Liasoning and compliance costs increased and are at par with marketing costs.

-

Developers have been forced to share some margins with contractors but not customers. Its more important for developers to exit the project after recovering the investment rather than sell it. Sharing margins with customers is not viewed as good business sense.

-

Tremendous focus on brand building. Some developers with good local brands are renting out their brand name to trusted sub developers. In future this may be a revenue stream.

-

Rise of pan india brokers like anarock.

Thanks

Bheeshma

13 Likes

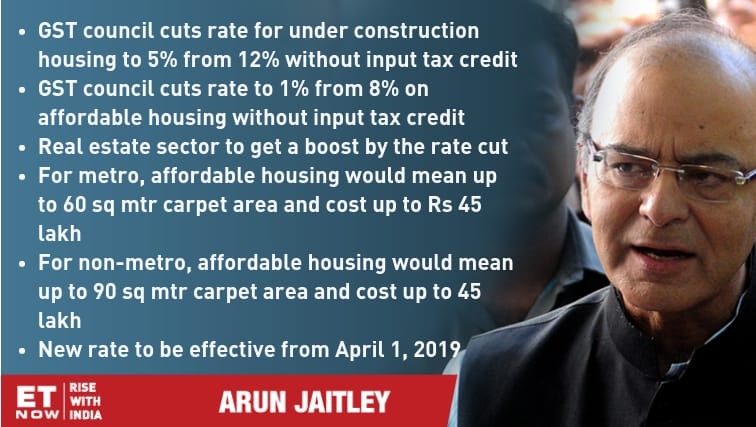

Relief for home buyers: GST rate for houses under construction reduced to 5%

https://timesofindia.indiatimes.com/business/india-business/relief-for-homebuyers-gst-for-houses-under-construction-reduced-to-5/articleshow/68138782.cms?utm_campaign=andapp&utm_medium=referral&utm_source=native_share_tray

Download the TOI app now:

https://timesofindia.onelink.me/efRt/installtoi

Pl note applicability is from 1st April 2019 . It means delay in sales closure by one month .

Also since this is flat 5% for luxury housing even after one month - people get straight 5% discount on buying completed flat …

On affordable housing 1% difference is not much and hence it is +ve … This can be temporary benefit so be careful in paying up for stocks

Affordable Housing will be benefitted

- Govt push for Housing for all

- RERA separated calfs and Wheats

- Interest Rates Cycle indicates lower rates in future

- Stagnant Property prices forced out artificial High Prices

- Inventory level coming down each passing qtr

Does it mean the change in GST rate is applicable only for affordable housing flats ?

But on the ground reality is very bad & in-spite of these changes the sector is not picking up. May be something big change need to happen.

Thanks,

Kumar

1 Like

Please listen to Q3FY18 concall of Ashiana Housing, generally they were very cautious/pessimistic in the last many quarters, but in Q3FY18 concall they are very optimistic/sound bullish and planning for new launches and new land deals.

If you see last couple of lines in what you posted has good details, both developers & supply side are consolidating which gives indication. Also we cannot complete go by management.

Finance companies are in stress due to liquidity crunch & big drop in black money and not great rental income from real estate income.

If market pick up we will get to know even if little late its fine. Also what i noticed these real estate brokers started Siggy delivery & Uber/ola etc.

Just go through below article good one.

2 Likes

I personally believe RERA proved to be Game Changer for the Industry…

Currently each one of us know challenges, headwinds and difficulties faced by Real Estate Sector…

RERA bringing up lots of transperancy, Accountability, Responsibilities which is Great for professional Builders…

Home Buyers are always there for homes available Right Product at Right Prices…

Real Estate Sector is one of the biggest employer & it directly & indirectly affect over 200 Industries.

Real Estate Contributions significantly to State Govts Revenue.

Best thing with this Sector is we all know the risks but unable to evaluate opportunities

RERA is not implemented in full spirit . Even in places like Bangalore is very much diluted .

Real estate is increasing having adverse industry structure …

-

On supply side industry structure was always unfavourable because of Government intervention , licences and corruption - Even best player cannot give a service delivery promise and create differentiation . Look at projects stuck for Mahindras , Godrej , Kolte of the world… This also create high uncertainty in business planning , working capital management and manpower management … Now this was true is past too so what has changed - some advantage has come to organised players by exit of smaller players … But big issues remain

-

On Demand side – Things have changed from Favourable to unfavourable … Earlier customers were less aware , used to finance builders even in pre approval stage , This financing was free of cost as builders did not have pay any interest on the same . So imagine a project was delayed by 7 years + 3 years of normal construction time … builder got free financing for 10 years . So even if Govt had created any problems builder could pass down the cost to consumers . Now this pricing power has been withdrawn from builders + NBFC who entered charged high interest rates … THIS IS HUGE SHIFT in industry structure .

Second issue on demand side is price transparency … With rise of online portals - customers can view price trends and also see what resale properties quoting and what new properties are quoting at same locations . This further reduces bargaining power of builders…

In all this GOVT has thrown in new devil … HOUSING FOR ALL plan is to construct 2 crore houses by 2022 . If if this is partially successful … this will create HUGE SUPPLY esp in affordable segment .

We need to aware of the above before investing in real estate stocks

3 Likes