I see that many of us have doubts about long term benefits for minority shareholders. It maybe that some decisions not in favour of minority but if we look at returns of Grasim over longer period of time, it is good. Idea is in wrong business but can we just look at long term shareholder value created by Grasim or even the earlier holding company of Aditya birla nuvo? Also, I feel that groups which go for demergers create more minority shareholder value than those which go for IPO? Please correct me if I am wrong here…because in case of IPO, holding discount comes for parent plus we do not get he new business (unless we buy in secondary market) but in case of demerger, the management shares the new company in same proportion with minority shareholders.

If anyone can give more details on when and why company go for demerger or IPO (except in IPO they get new capital)…and which benefits the minority shareholder more in long term?

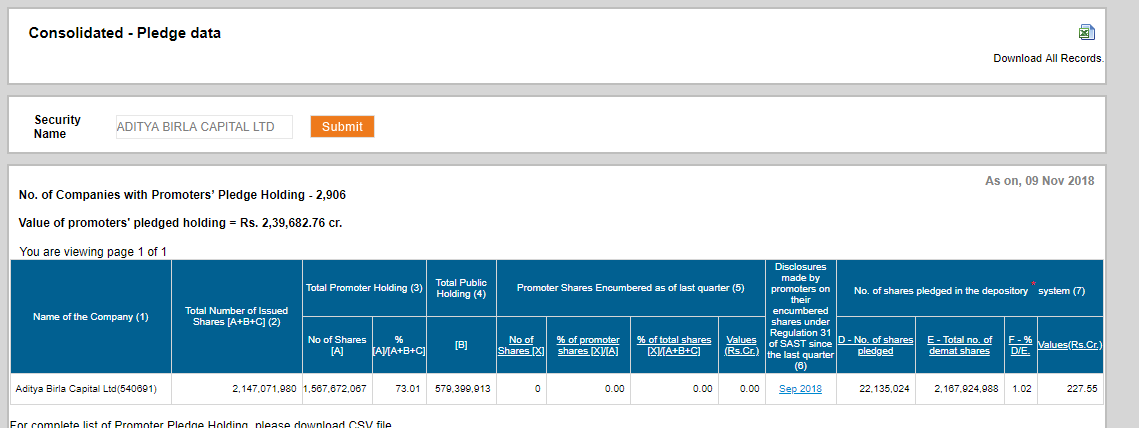

To all who like Aditya Birla Capital,just give it a thought why share price is subdued after demerger. When Aditya Birla Capital was listed , Grasim Industry was part of the MSCi India Index which has weightage of around 8% odd in MSCI emering market index. Foreign Portfolio invester/Mutual fund wiedly follow this index.After demerger this entities also alloted Aditya Birla Capital due to the holding they maintained in Grasim.As those funds mandate is based on Msci index FPI/MF are forced to sell Aditya Birla Capital because AB Capital still not part of Index.This bit of news was very wiedly published on media.Now I tried to gone through the shareholding pattern disclouser company published to exchanges.Three of them came out till last quarter,March 2018.

73% odd is promoter holding in the company , as per Sept 2017 release non promoter FPI holding was at 7.87% ,Euro Pacific Growth Fund (still they are holding at Grasim Industry)was holding another 1.1% , Citi Bank NA is holding ADR(again due to Grasim and they holding Grasim till date ) amounting to 1.26%.

March 2018 shareholder disclosure is showing FPI holding came down to 5.27% both Euro Pacific and Citi Bank has sold the position. Interesting…this sort of supply of scrip may put more pressure.FPI inflow to equity in India only weakend starting from Feb-March 2018.Looking forward for June 2018 release. What do you think.Is it natural phenomenon does it justify slide in price?

Aditya Birla Capital has big name associated with it. Leaving apart Birla from name though their topline is rising however bottom line is still sluggish due to expansion taking place. Lot of hype had been built up due to insurance, AMC arm. Still it trades at P/B of 4.2 which is little expensive. It will take long time to recover however will give good returns in 5 year horizon. It is fairly valued right now don’t see any further downside until some negative surprise in results

Agreed. Limited downside risk from hereon, but in next 3-5 year there is a high degree of possibility of making decent return, given high growth visibility.

However on your point of little expensive, i feel if you compare all the large sized NBFC including bajaj finserve, this seems to be much fairly valued.

Aditya Birla Capital Credit Suisse maintains outperform with target Rs 175

The research house has remained positive given its good growth potential and improving profitability across business.

Why is this stock trading at a such high P/E and P/B multiple? Q on Q growth has been flat since last few quarters and many of the businesses are mediocre or at initial stages.

AB Capital combines business of different kind…pe pb valuation may not be good idea.AMC business ,Life insurance has performed well.AMC business can get a pe multiple of 30 easily. 1k cr month sip book.36% equity book and growing. Banca tie up has turnaround the life insurance also insurance book has largly traditional product and 9% comprise of risk product of NB.newly started health insurance business is draging the profit ,arc business also newly started, insurance broking fees gets reduced and a drag on the company. Major business AB Financial service has shown detoriation of asset quality.But NIM is quite healthy.

On separate note canda based pension funds are interested in nbfc business.

AB Capital subsidiaries has started to report result. AB housing Finance reported its H1.

Revenue at 460.72 cr for H1 FY 19 vs 245.93 cr H1 Fy 18

Pre tax profit at 34.26 cr for H1 Fy 19 vs 11.06 cr H1 Fy 18

Net Profit at 21.85 cr vs 20.27

Asset quality and all detail will be known when AB Capital publish its result.Posting this No from Business Standard. Not sure when Aditya Birla Finance will repot the No

Aditya Birla Finance reported its halfyearly No. Few metrics from result

net profit up 29.60% h1 fy19 yoy h1 fy18.

asset quality is mostly stable at end of sept 2019 GNPA is .93% vs .91% March 2018. Higer level of Npa is due to increasing share of unsecured retail lending which have high margin also.

NNPA 0.40% vs .42% sept 2018 vs March 2018.

Provision contingencies at 78.87 cr vs 137.71 cr at h1 fy18

Gearing position is very conservative at 5.87 times. Management has stated again and again gearing will be at kept this level if required capital will be infused.

One more point is networth at 6903 cr h1 fy 19 vs 6228 cr mar 2018. Good 10.82% increase.

Other metrics will be available mostly on 6th Nov with AB capital result.ABFL_UFR_Sept_2018.pdf (764.3 KB)

Rather than AB Capital, HDFC Ltd can be looked as good investment for complete financial inclusion. You get all the financials (Bank, Insurance, AMC) + the mortgage business trades at < 2 times BV

Looks really undervalued. What are your views on this?

Interesting … HDFC has Bank as well. Two things that would bother me is (a) Cost to Income ratio is just 9 (it has come down to single digits over the decades) … any pressure on cost will impact profitability and returns in a big way. (b) 75% is held by Foreign institutions. We can learn from IL&FS where the promoters were big and/or foreign institutions and the professional management nicely played with the Balance sheet until everything went dry and the main guy Ravi vanished quoting ill health. And then the skeletons tumbled out of the cupboards.

HDFC also has had the same set of guys at the top for decades and so that is also very similar to IL&FS.

In short the two concerns are :

AB Capital … Promoter Holding is 72% versus HDFC (0%) …

Cost to Income Ratio of 9

So, I personally I would not replace AB Capital with HDFC but may add both to the portfolio.

Disc: Invested in both and accumulating AB Capital in small quantities.

That is the dilemma even i am facing…Certainly, HDFC has an excellent management pedigree at present, but with uncertain future. Recent shifting of one to Axis and another resignation has added to uncertainty…

Axis Bank (Under Shikha Shrama) and ICICI Bank (Under Chanda) had a lost decade or so after management change…And both dont have strong promoter groups enabling senior managements to show pathetic results year after year till RBI acted to boot them out…

HDFC group also lack any promoter group and investor activism is still to take birth in India…

Thanks to all for their analysis and opinion on this scrip. Amidst the above highlighted corp governance issues the only silver lining I see is that Premji still holding 2.54% at 145 a share. I have averaged down and pegged myself close to Premji at 146 a share.