Ventura research report - Dec - 2018:

1 Like

Q1Fy20 PResentation: https://www.bseindia.com/xml-data/corpfiling/AttachLive/42a64782-a6be-445c-bed9-c7212025768c.pdf

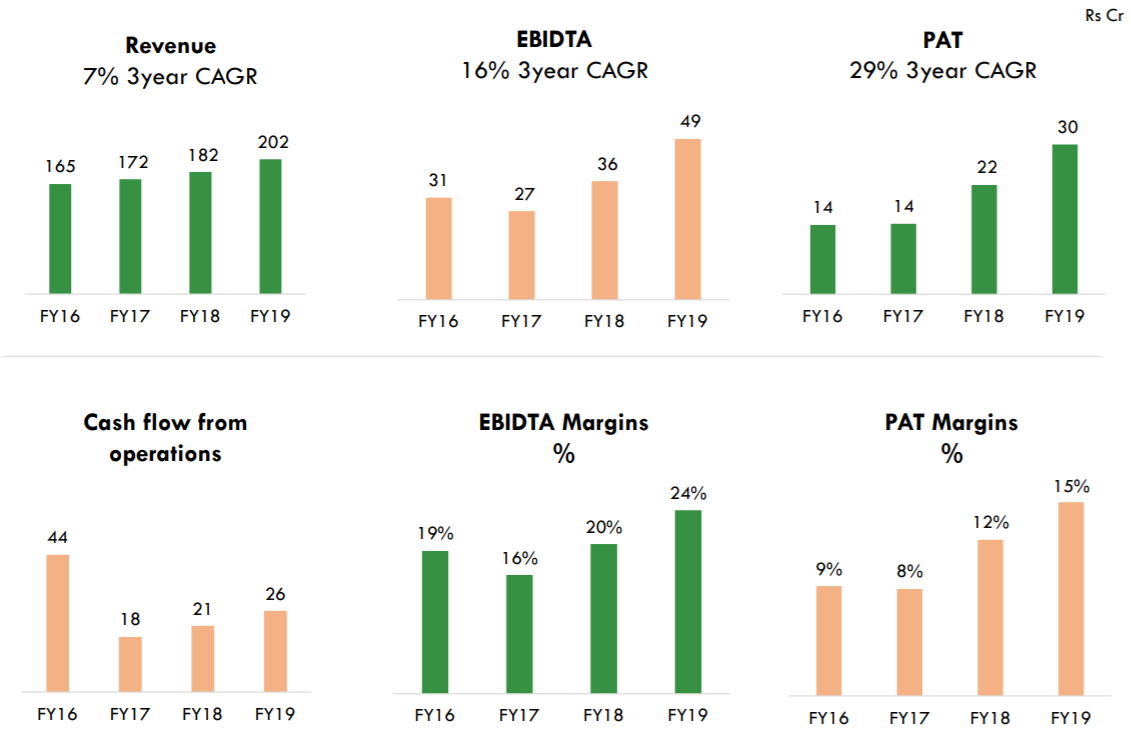

Good to see the good set of numbers from last 3 years…

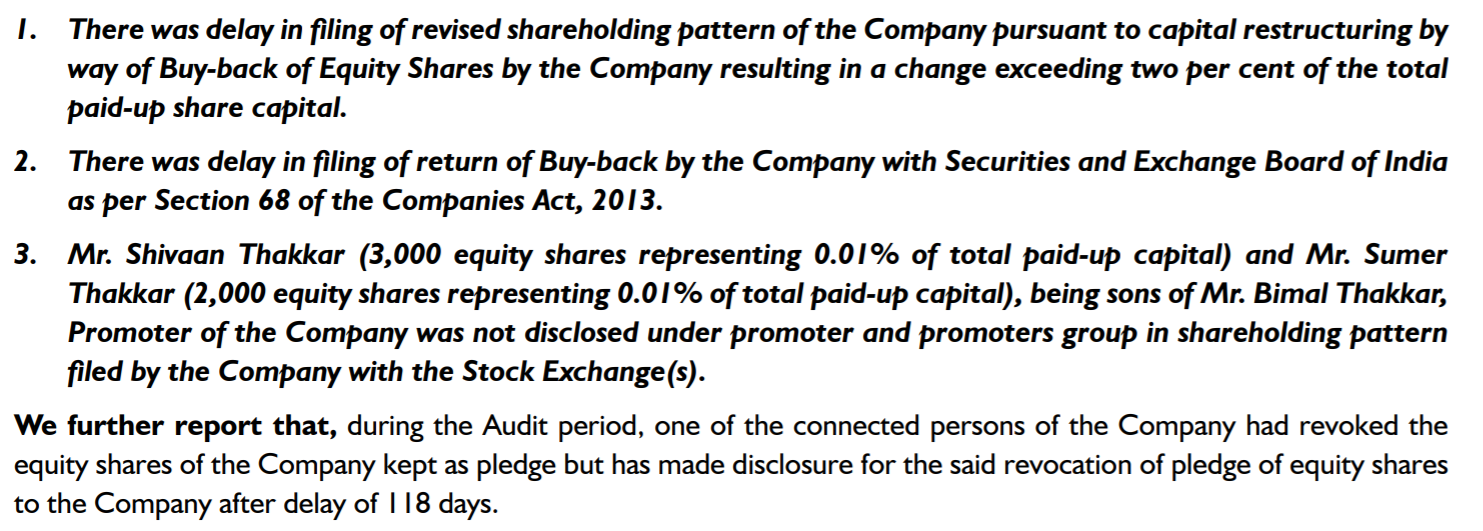

Few negatives from Audit report

3 Likes

Not sure why people still want to go through ratios even after SEBI fined the promoter. Is the business model really that good?

2 Likes

Q4 Results: https://www.bseindia.com/xml-data/corpfiling/AttachLive/6c816879-764a-4903-a6ca-5c4ac94929b9.pdf

ADF Foods has come up with a good set of results. What is interesting is the new line of business viz Agency Distribution to US and UK markets that they have gotten into in 2020. This line contributed 32cr or 12% to the total operating revenues of the co clocking EBIT margins of ~ 25% and is chiefly responsible for the good growth witnessed by the co. The facilities in Nasik and Nadiad have been partially reopened as they come under essential commodities. The co also remains net debt free. At a PE of 10 odd it seems like a good purchase with the usual caveats that the low PE could turn into high PE if earnings drop.

Its plan of focusing on export markets over its domestic focus gives its a wide range of options and geographies to target alleviating problems faced by domestic focused cos of scaling up profitably due to a small market size. Domestic market sizes have historically been small in this industry in general so a larger market to target is always a source of comfort.

5 Likes

Any comment on Raw material availability and prices of raw materiel? raw material could increase in future bcz of Covid-19 issue.

Precovid the gross margins were +/- 5% around the long term average of 50%. Even if gross margins are hit , that hit should be temporary in nature and margins should normalize.The co seems to have a done a good job of improving the margin profile and clocked a PAT margin of ~16%. 5 years ago frozen foods contributed to 15% of Sales and now in 2019 they contribute 33%. While i am still trying to get a hang of the business , whatever little i know suggests that the margins are quite high in the frozen food business. Since this is an export oriented business, rupee depreciation also helps.

4 Likes

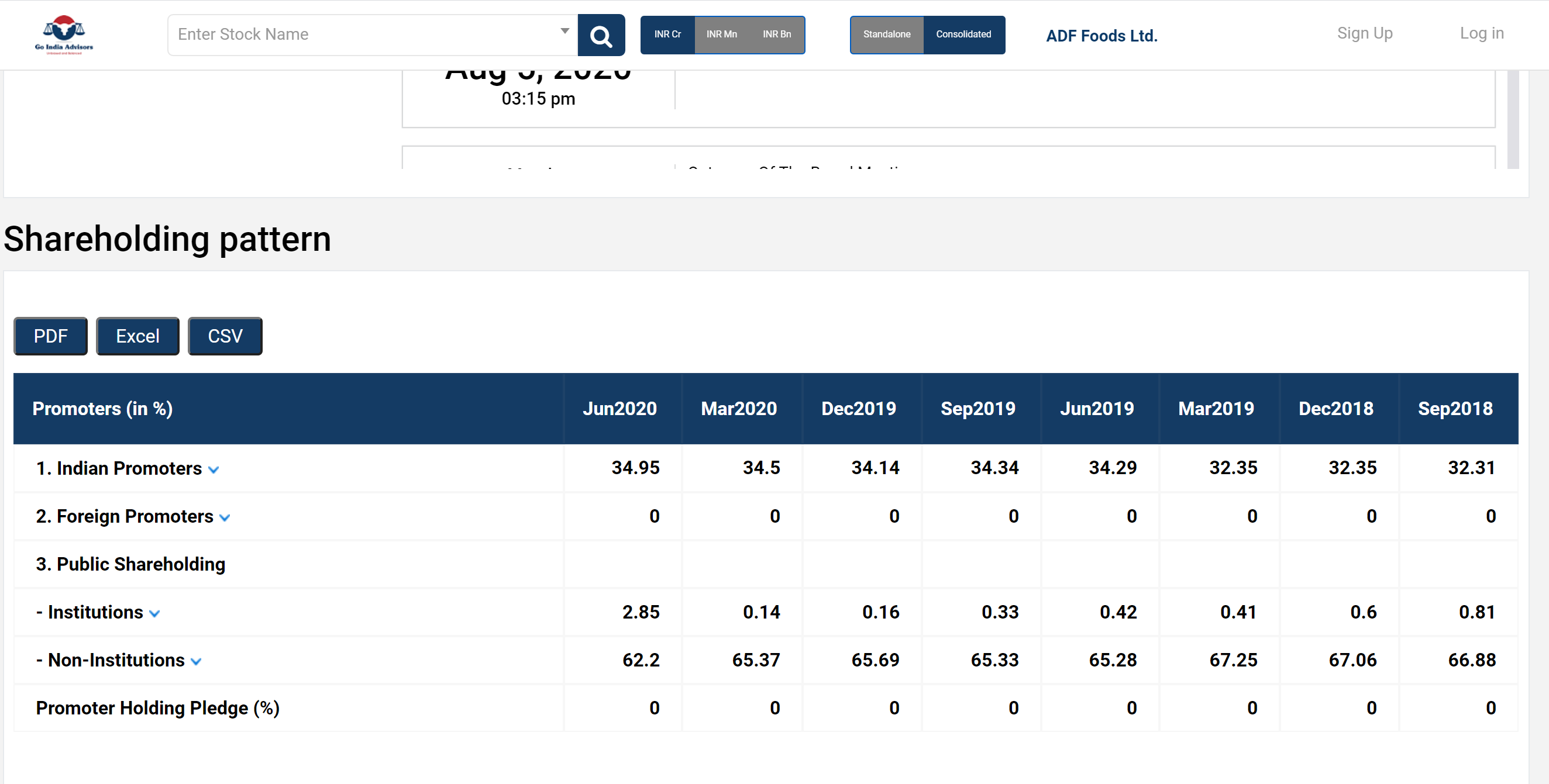

As per the latest shareholding pattern there is no pledging of shares.

But as per disclosure made on 18th March,2020 JM financial have released encumbrance on shares.

How can this be possible? can someone from the forum explain the deviation?

ADF Foods Any fresh views here.

I request the boarders to look at the new developments in this company.

- New business vertical - Agency distribution business with HUL.

This is new segment started last year did a 32 cr sales in the FY 2020.

The Company has also entered into a new business segment wherein it acts as a distribution agent of food products for a Fortune 500 FMCG global firm in the US and UK markets. This new vertical gives us a wider product portfolio to offer the retailers who stock our products as well as it enables us to use the retail network of the FMCG major for our own products. This vertical contributed 32 crores to revenues in FY20. We are confident that this business would supplement our core business very well going forward.

- . Fund infusion from Promoters/non promoters through convertible warrants . Company as per recent EGM meeting planning to raise funds worth 70 cr. This is a debt free company with free cash flow and cash holding of 50 cr.

What is the boarders view about this company are they going for a acquisitions ?

As per my understanding this is one of the cheapest stock in the FOOD-FMCG sector and it deserves premium valuation PE more than 30 plus as the all the peer food companies have been trading at PE 40-60 range . Please add your valuable comment .

4 Likes

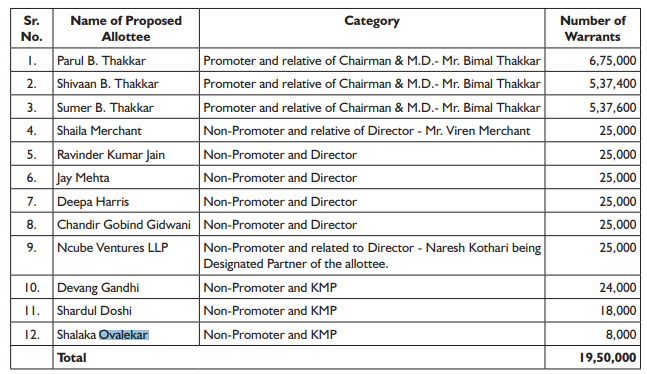

ADF food has convened EGM on 5th-Oct for raising upto 70.59 CR (almost 9.7% dilution) with issuing Warrents to Promoter, Company Director, Independent Director and KMP. Price is decided as per SEBI rulling at 362.

Viren Merchant,Ravinder Kumar Jain,Deepa Harris,Chandir Gidwani is independent Director.

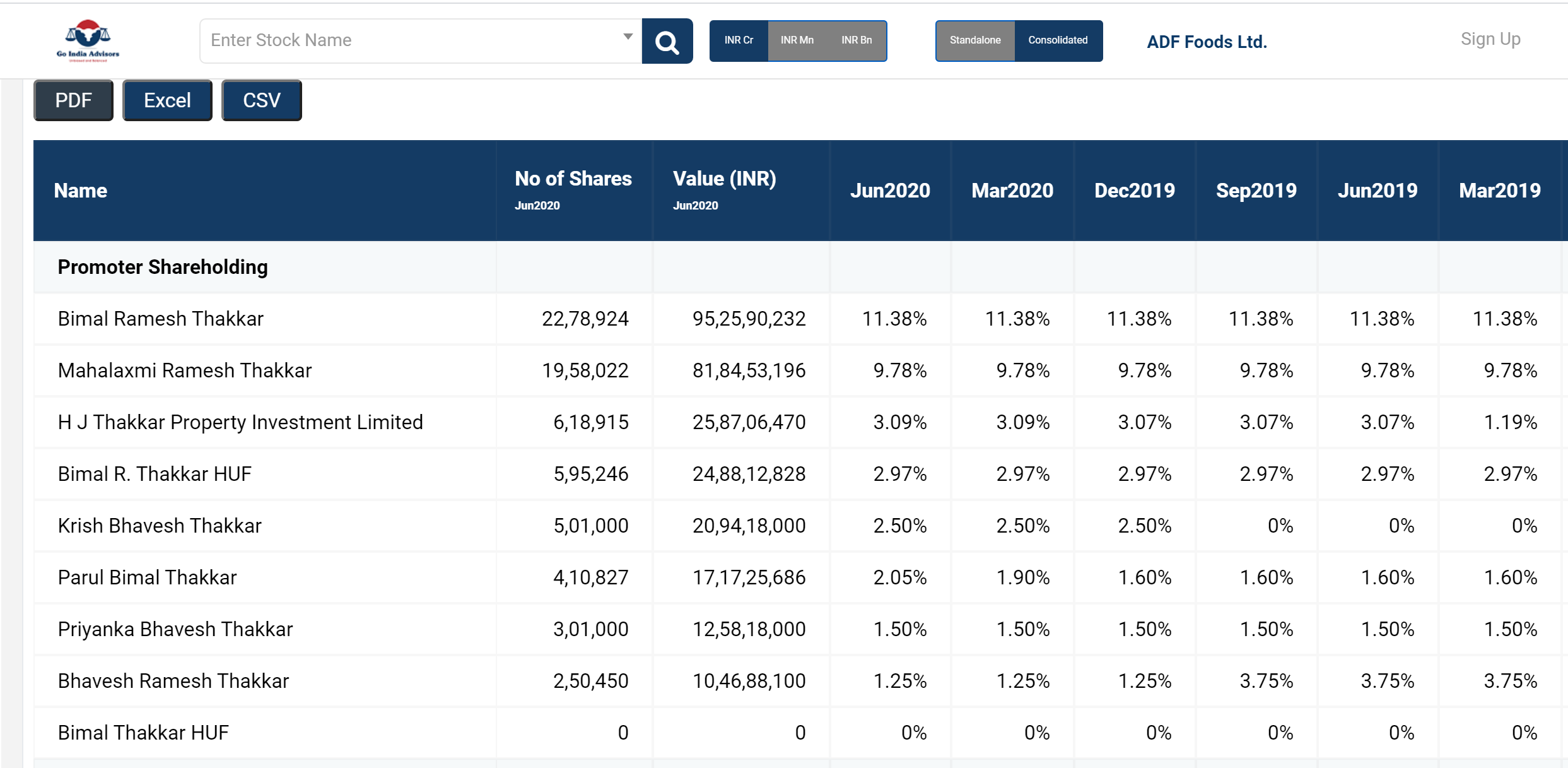

Devang Gandhi is COO,Shardul Doshi is VP - Finance, Shalaka is Company Secretary. With warrent converted to equity,Promoter Holding is going to increase from 34.95% to 39.82%

All,

If anyone can provide more inputs on following few items it will be helpful:

-

If the company is a cashrich company without any debt, why is it raising cash through warrants to promoters rater than promoters buying from the open market. Even this warrant price is below CMP.

-

What led to sudden increase in profitability in Q4’20 and then subsequent drop in Q1’20. Was it more because of stocking up easy to cook items before lockdown leading to higher sales in Q4 normalizing back in Q1.

-

What are top drivers of profitability and growth of the company. I am not sure if the underlying demand of their products is growing strong nor the market for indian storage food growing a lot (5-7%). On profitability side, other than outsourcing manufacturing (which was in the past) what will lead to future profits.

1 Like

-

The promoter stake is low and he has been trying to increase stake for long time. Warrants give time to pay in the funds over next 18 months. Though this is not the best corporate governance practice. Ideally he should have done creeping from market or should have come out with rights issue at much higher price to raise his stake.

-

I believe there was some supply disruptions in Q1, which led to lower sales.

-

The company doesn’t sell in India much, it’s large market is US and other export markets like Europe and Middle East. Should continue to do well in near term as more people eat at home.

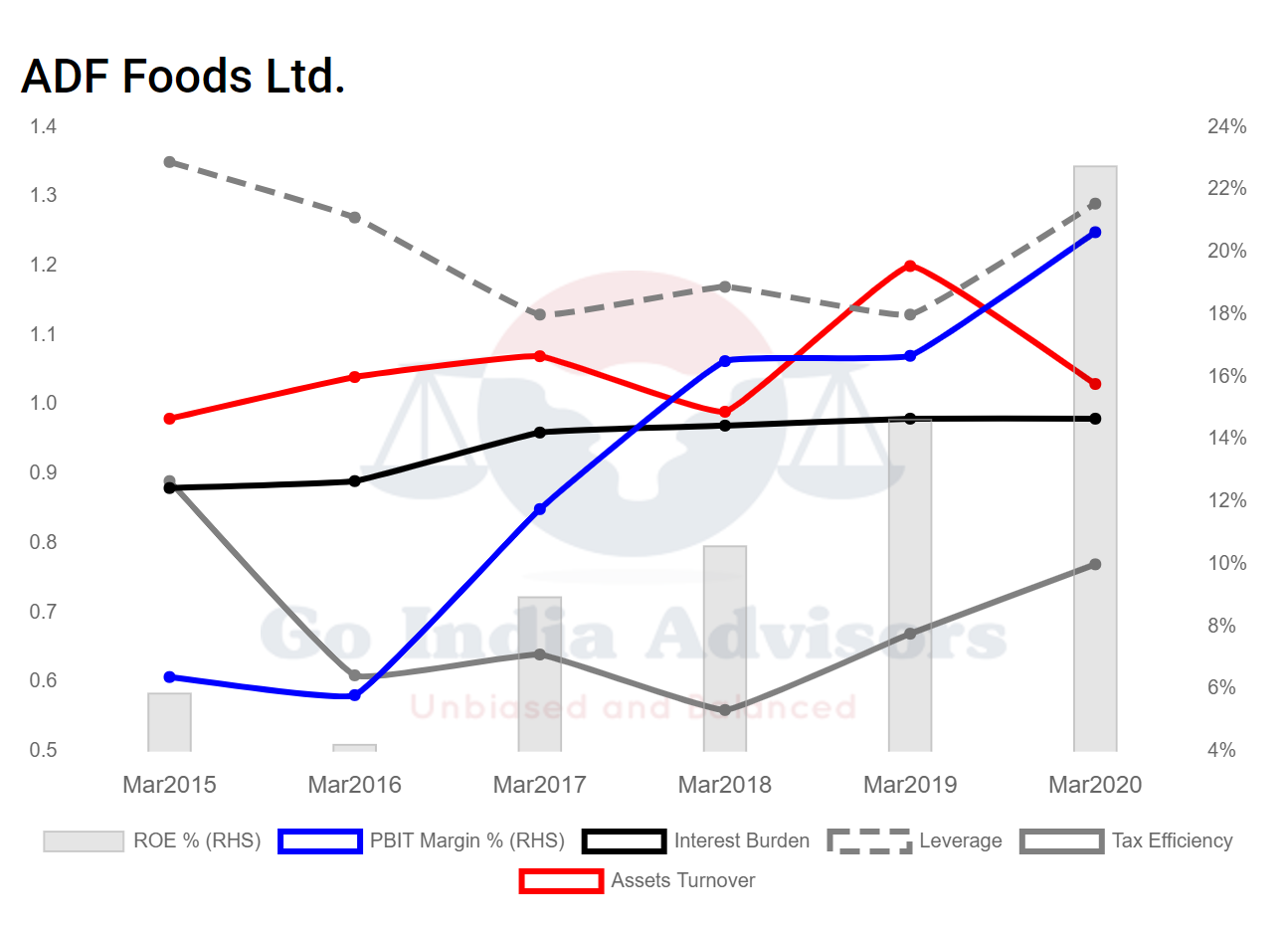

ADF Foods has improved ROEs strongly over the last 3years driven by sharp improvement in it’s PBIT Margin. Post the split between the brothers company seems to have become more focussed.

source: GIA Stocks

Disclosure - Am holder of the stock, since last 2 years.

1 Like

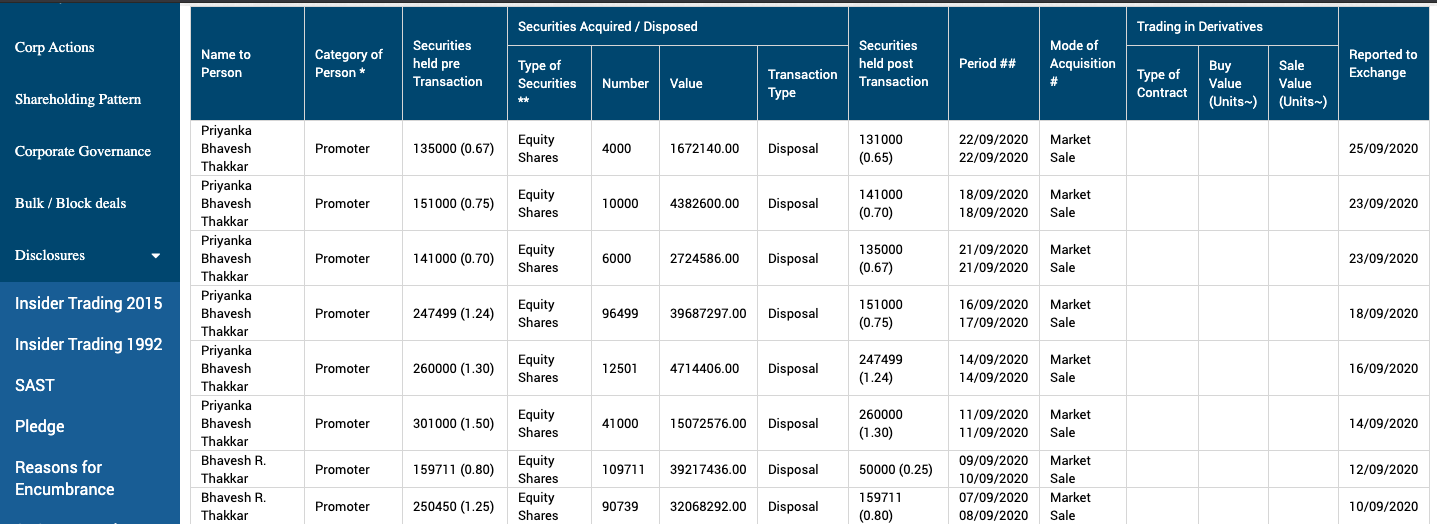

Any idea why the promoter are continuously selling their stake in open market

Sorry, Bhavesh is the brother who has separated and moved away, and has been selling for last few quarters. While he is counted in promoter, but now it is only Bimal who is the real promoter. Bimal’s holding is close to 25% + the warrants.

Source: GIA Stocks

2 Likes

Very good result posted by ADF foods. Cash flow from operation at 30 cr vs NP of 28 cr. Agency business has show great growth this half year.

Company bank balance increased to 74 cr. Company has also filed for 35 percent capacity expansion at the existing plant through internal accruals. Stock trading below 20 pe which is quiet cheap compare to peers.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/938d09fe-b0b8-48e5-9c28-09f2010bcd1e.pdf.

Invested .

Views invited

4 Likes

Notes from ADF concall

2 cr annual leased capacity will add to 20-25 cr top line.Will be operational in 4 months time.

This is a temporary set up until company comes up with new capacity organic or inorganic.

Govt stopped MEIS incentives company planning to migrate to PLI schemes and waiting for guidelines

Meis impacted ebitda margins (2-3%)

Indian plants were running at 80-90% utilisation rate in Q2 may add another 10-15 cr annually to topline at maximum utilisation.

Agency business have the potential to reach 40-50% of topline in 3-4 years.

US subsidiary outsource manufacturing does not require any growth capex.

5 Likes

Q2-FY21 concall notes

- Ready to eat, fruits, ready to cook, flavored milk, meal accompaniments. 55 countries.7 brands, 2 manufacturing units: 1 in gujarat and 1 in maharashtra, Both have

- Distribution network is key strength. 180 distributors globally.

- Products are sold under 4 brands: Ashoka, truly indian, Camel and aeroplane.

- 2nd vertical is US subsidiary: organic and natural foods: Mexican foods, meatless products. TJ’d and nates brand. Manufactured in US.,

- 3rd vertical is agency distribution business: under which we distribute products to fortune 500 FMCG companies: Distributing in US and UK: Mostly tea and coffee. Started in FY19. Growing very well for us.

- 4th vertical is India business: very small and insignificant. Have plans for the future, Pickles, sauces: brand Soul. Only available in Mumbai right now. Sold in Modern retail and sold online.

- Covid crisis brought changes in consumer behavior in health, hygiene etc. Baked snacks, meatless meatballs, olive oil based pickles are innovative products we have made.

- Growth based on 3 pronged approach:(i) Investing in increasing manufacturing capacities. Acquired Gujarat manufacturing unit on lease basis. Requires 2cr additional capex. Will be ready to operate in 4 months. Will manufacture Ready to eat and frozen food products. Looking at greenfield expansion 30-35cr in US. Will complete by FY22. (ii) Strengthening distribution network. Own depos. Continuous supplies to distributors. (iii) Distribution business with fortune 500 companies is doing well.

- [Financial performance] Revenues up 2% YoY. EBITDA was up 26% with margin of 19.2%. PAT up by 36%. PAT margin stood at 13%.

- [EBITDA growth was low]: (i) Uncertainty around Export incentives. Government is scrapping MEIS and introducing PLI linked incentives. PLI is 3x of MEIS. That scheme will start from Jan’2021. While we will continue to get MEIS during this CY, they didnt accept any claims due to some constraints on their end. This impacted EBITDA margin by 3%. EBITDA would have been 22%. (ii) Agency distribution business contribution is higher. Compared to standalone business it is lower EBITDA margin, lower gross margin. Export incentives will not be withdrawn. 19cr number from the agency distribution business is at a lower margin. Distribution business EBITDA margins are at 12-13%. Core business we are improving EBITDA margins. Even as distribution business percent improves in the topline, we feel confident that we can maintain 20% EBITDA at consolidated basis. US subsidiary EBITDA margin has also grown in H1FY21.

- [Lease facility] For the lease facility, 2cr annually is lease amount. Revenue potential is almost 25cr. Stop gap arrangement (for 2 years) until the greenfield project comes up. Probably goes up to 30cr in Year 2. Will make ready to eat and frozen foods.

- [Growth drivers]: This quarter we have seen growth in all our categories. Meal accompanies, sauces, ready to eat, frozen foods. Faster growth is seen in ready to eat and frozen foods. We’ve added some new products, distributors etc and that has helped us grow.

- [Greenfield expansion of 30-35cr]: Funded through Internal accrual. Why did we issue huge warrants to promoters and directors: We’re looking at some aggressive growth opportunities (including inorganic) so we wanted to have a war chest ready for any opportunities which come our way.

- [Gross margin]: Fell from 52% to 40%. Agency distribution is significant part. Gross margins are significantly low but there are negligible other expenses. Hence the most gross margins flow to the bottomline.

- [Asset turns for capex]: For the 30-35cr capex, typically revenue addition is 2.5 to 3x for topline. So 80-100cr.

- [Q1 difficulties]: We were working at 45-50% capacity utilization. That too starting in May and June. Currently the entire shipping industry is facing a container shortage. Being one of leading exporters out of India, we have been able to get our shipments out on time.

- [Stickiness of Sales growth]: 98% of revenues are from exports. Packaged foods is a way of life internationally. We see in some markets trends are shifting to packaged foods. We feel demand will not go down. We also have products which we sell to restaurants/Food services. It is 10% of total revenues. That part of our business has been currently impacted due to restaurant shut downs.

- [Inorganic growth statement]: Focus on core market for acquisitions.

- [Agency business]: We basically buy the goods stock in US and UK markets and sell these goods through our current network of shop distributors and retailers. It helps reduce our selling costs and it helps improve our position since retailers are more dependent on products from our company. It does involve working capital. So I have to have 3 months holding stock because of shipment and holding time. It is helping both the companies. Current company we are looking at adding more products. In 3 years it could account for 40-45% of topline.

- [Growth triggers]: We are seeing growth in demand in some categories and indian food is gaining popularity with non indians as well and that is why we are doing the capex. We feel confident about the investments. Good traction for products. Intend to double revenues in 3 years.

- [India strategy & Online]: Will Finalize India strategy next year. Internationally we do sell online, but overall online business is not very big for us. Base is low, we have had huge traction.

- [Competition with Haldiram’s]: Their strength lies in namkeen. Although they are into frozen foods, that is a strong point for us. We have built a strong distribution network which gives us an advantage.

- [Warrants]: Will increase promoter holding by 6%. Independent directors have subscribed for the warrants. Some key management personnel as well.

- [Fortune 500 company]: Unilever Canada: we distribute their assamese brand of teas in US and UK.

- [Private label]: Healthy Gross margins on private label business. 15% of revenues.

14 Likes