Excerpt from rakesh-jhunjhunwala.in

Adani Transmission – ideal combo of security and growth

Mudar Patherya has given ten cogent reasons why Adani Transmission is the ideal stock with the security of a fixed deposit (assured returns) and the excitement of growth (higher incentives). These are as follows:(i) Adani Transmission is the Power Grid of India’s private sector power transmission entity. It has achieved its 2020 capacity target three years ahead of schedule;

(ii) the returns on the assets — power transmission lines from one point to another — have been secured through long-term annuity revenue contracts with the government;

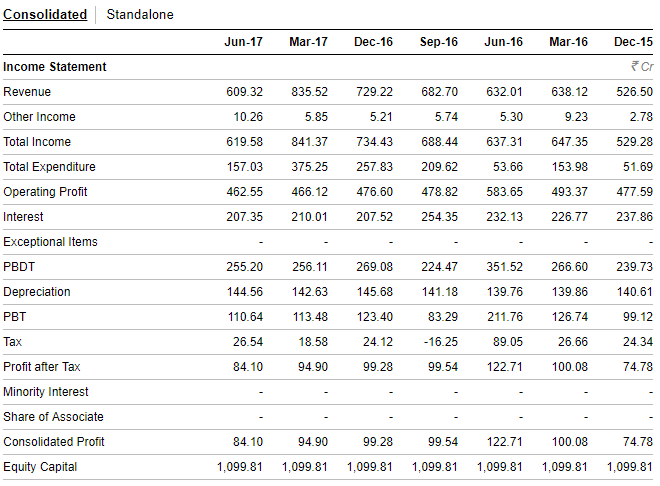

(iii) the business is marked by high profitability; the Ebitda (earnings before interest, taxes, depreciation and amortisation) margin was 92 per cent in the first quarter of this financial year;

(iv) the moment the company stops expanding, it can select to patiently draw debt down and become a cash cow — or keep expanding capacity, with a relatively stretched but secured balance sheet (which is what it is doing);

(v) it has reconciled two business models, the pass-through where the government provides a pre-agreed return of 18 per cent internal rate of return (IRR) equity, with all costs reimbursed (five projects) and a tariff-based competitive bidding (TBCB) model, where the lowest cost company wins (nine projects);

(vi) the business is largely de-risked the moment a transmission network is activated — a high penalty for delaying or defaulting customers ensures timely inflow for Adani Transmission;

(vii) as the government graduates an increasing number of projects to TBCB, Adani Transmission expects to flex its muscle, using cutting-edge HVDC lines that deliver network availability much higher than the mandated average;

(viii) the company has graduated to investment-grade rating, making it possible to raise low-cost global funds (the second biggest profitability driver). The company’s 10-year $500 million bond offering attracted ~35,000 crore of borrowing interest, translating into a premium;

(ix) the company possesses deep competence through senior managers who, in their previous jobs, commissioned an aggregate 25,000 circuit km, providing Adani Transmission with rich intellectual capital (in land aggregation and right of way), making it possible to commission faster and cheaper (huge edge in a TBCB environment), leading to a 18-19 per cent equity IRR return, around 400 basis points higher than what is assured by the government;

(x) the company has demonstrated it can acquire transmission networks with speed, which has helped eliminate risk and prepone revenue inflow.

Financials:

Triggers:

Reliance Infrastructure to buy the Mumbai city power business

Valuation:

This is Varinder Bansal’s valuation when it was trading around 40,

Another from stock Utiliities:

RISK :

- As of Oct 2017 , valuations look stretched. It has run up a lot ever since, currently at a PE of 63.46

- Cyclical nature of transmission business.

Here they gave target of 55.

Disclosure: Holding from 60 levels