Utmost thanks to the founding members(Mr Hitesh,Ayush,Abhishek,Donald,Manish and others) for this excellent platform to learn and attain financial independence.

I too have a dream of being financially independent and building my portfolio which can give me 18 to 20% CAGR till 2021( almost 3 yrs from now). If I am able to do so, then I can look for some other aspects of life and career.

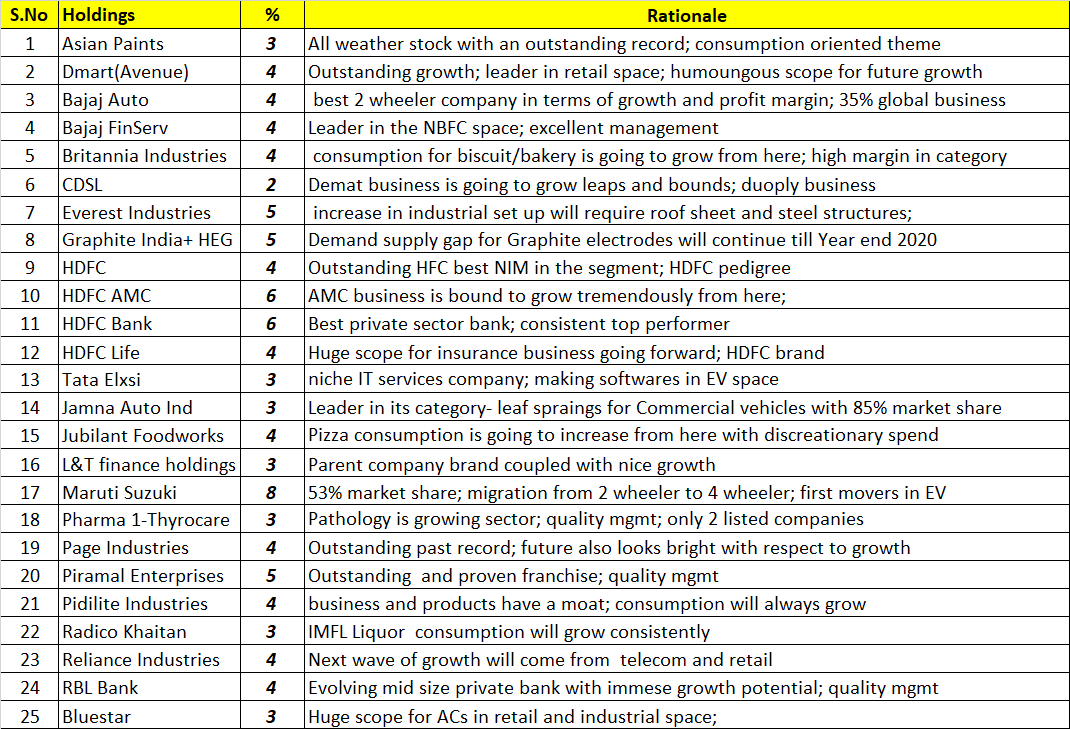

With an objective of returns mentioned above, here is my portfolio, with % allocation.I have invested a good amount in the recent drawdown of sept/October and thus average buy of most of the scripts is quite fair.

Request your review and guidance. I will be grateful:

Your portfolio looks very good it contains all the great names of Indian corporates, well diversified which is essential for a beginners and it’s well aligned with the index given your exposure to financials.

I’m just curious to know if you had employed any valuation criteria before buying these stocks.

Your portfolio looks great which includes sector leading companies.

As you expecting 18 to 20% CAGR till 2021, want to know whether you have deployed your capital 100% into equities or you have maintained sufficient debt to equity allocation. Though we have seen a correction still the large cap index looks overvalued so there are chances that we can see Time Correction or further correction.

Tata Elaxi - This company seems to be getting merged with TCS and TCS is overvalued so there are less chances that Tata Elaxi will provide similar returns.

I own few common stocks HDFC, HDFC Life, Maruti, Britannia, Pidilite. Rationale is also similar. But 25 stocks is a big list. If you can manage its OK, but I suggest 10-15 should be sufficient diversification.

Have u considered the fact that the overall environment is a heated one, the general environment is of exuberance, hence, the overall PE is high? The purchase prices are high in general.

If you had said that you wanted to hold for a longer period of time, then you have selected a good set of companies, which Hitesh Sir has approved too, you’d have no problem.

But, by 2021, I feel you won’t get the results you want. It’s too short term. It is not advisable to start a portfolio now. Seasoned investors on vp are getting into cash.

Thanks a lot, sir; your validation has boosted confidence and will enable me not to venture into new opportunities, rather watch the progress and exercise patience(which is a highly abused word these days- people talk about patience but look at their portfolio every 2 hours .

Regarding your feedback on reducing NBFCs, I have 4 currently - Bajaj FinServ, HDFC,L&T Finance holdings and Piramal Enterprises: agreed it can be reduced to 2; L&T FH for sure can be toned down, I will look into their valuations again and take a call. May I ask you what’s your preference?

Regarding your advice on increasing exposure to private sector banks, what would be your picks in Private sector banks? I have HDFC Bank and RBL

Thanks a lot Nitin.

Regarding the valuation criterion, I don’t follow complex DCF or any other tool, but follow simple avg PE of the company and how is it currently in comparison? I believe quality comes at a cost, thus slight PE expansion is fine as long as top line and the bottom line is growing 15% plus QoQ,YoY.

If the horizon is long, I can afford to pay 15 to 20% extra from the correct valuation, as Peter Lynch says “Far more money has been lost by investors preparing for corrections or trying to anticipate corrections than has been lost in the corrections themselves”.

Thanks a lot.

Considering all the assets, My portfolio allocation as of today is as follows:

Equity : 48%

Gold: 12%

Real Estate: 12%

Debt instrument (PF/PPF/NPS etc): 12%

Cash+Liquid Funds : 16%

So, effectively equity is less than 50% of overall PF.

Tata Elxsi: this news is for a long time but have not been done yet.IMO, Tata will not dilute a niche brand

Good advice! Wanted to know if it is because of time horizon till 2021 or because of current hostile environment against NBFCs or have you lost trust in NBFC business model in long term? Thanks

Great picks Abhishek. On Radico, and assuming that you constructed this portfolio recently, did you ever try to choose between Radico, United Spirits and United Breweries?. Specifically asking since, a lot of junk has now been cleaned at Spirits and Breweries - And results have finally started showing some promise at these two companies. (Notwithstanding Demo and Highway ban, which was more of a industry wide issue).

Thanks, Amit for your reply

I don’t agree with you fully; however, point taken that we need to be prudent.

My equity allocation is 48% of overall PF, so its a balanced one.

Moreover, if at all there is a major crash( which I doubt) quality companies with stable earnings will also fall, but they are the ones to rebound strongly unlike small caps and low-quality mid-caps.

Conversely, everyone is thinking volatility due to elections; what if NDA comes with a sound majority, it might be in your favour.

2021 doesn’t mean I will pull out all my equity money and retire, its just a roadmap, I might continue for the next 15-20 yrs with these companies if they continue to provide expected returns.

Lastly, as Peter Lynch says “Far more money has been lost by investors preparing for corrections or trying to anticipate corrections than has been lost in the corrections themselves”

So better to stay rather than anticipating; only God and Liars know the market timing

valuation wise Radico Khaitan is much better; USL and UBL with a bad mgmt and high valuations , I skipped them

Radico: Magic moments vodka is 50% plus market share in vodka ; take the market share of smirnoff and romonov

8pm whiskey,Contessa rum,old Admiral brandy- all are great brands.

Peter Lynch said it in a certain context. He is a master investor in growth stocks. Whereas, the list you have has a bias towards large caps.

Your selection is great. Shows that you are not new to the markets. You think like a seasoned investor too, that if a good stock corrects it will rebound.

However, my intention was to bring your attention not only to the notable draw-down your portfolio may go through if any serious correction should happen, but also to opportunity that you may lose; opportunity of investing in absolutely stellar companies and mouth-watering valuations, which the ebbing tide will bring.

Hitesh Sir too agrees that this may not be the best time to start a portfolio.

In these times, at Nifty PE 25.45, a sensible thing to do would be to sell whats expensive and get partly into cash and partly into what may appear good quality and cheap, like in Pharma or NBFCs.

Timing the market is different from having a fixed set of criteria for making investments. For example If someone insists on investing (or adding) only when Nifty PE is below 22 that is different from someone shorting the Index in the futures market because of his research on “historical data”.

Just discussing. It would benefit if I had the link in handy which tabulates the bell curve of Nifty PE over the long term.

PS: I have made a strong note of the excellent mix of companies you have chosen Jain-sab.

Management of USL is now under Diageo’s control. In my opinion it is better to stick to a perceived better governance company with brands (USL) in this space. USL had gone sub 500 levels during the recent crash which is a great entry price in my opinion.

You may want to add a few of the evergreen FMCG companies slowly, maybe even an ITC.

All the best.

disc - invested in USL, ITC, HUL etc from some time

Just curious to know, why USL share price and profits are like a shape of W. Kind of cyclical. Also FY 13, 14 made heavy losses, thereafter steadily profit growing. However common sense says liquor consumption has been steadily increasing. Isnt it. Why such volatility ?

.

.