In the face of the carnage/correction, does Coffee Can investing makes sense if one has entered the market in the last one year???

2018 has been a very interesting year so far.Late 2017 and very early 2018 saw a lot of excesses on the price side.Any good news and stock would run up 30-50%,any management’s word was taken on face value,SME companies with a very limited track record were able to raise money at decent valuations and still gave good returns for a short period! Also,2017 was an unbelievably low volatility year.In the US,some Funds had even shorted the VIX!! And that kind of market sustained for a few months.This had to correct.LTCG and rising bond yields became an excuse and markets started their slide.IT stocks had started rising already and became the leaders of this market.The whole backdrop changed…from being a mid-cap,small-cap heavy market to a moderate market and a violent mean reversion in volatility ensued.In March,most people were of the view that the selling pertains to LTCG and it would be back to ‘normal’ in April.However,that move proved to be a bull trap and now the broader markets have taken a decent drubbing with accidents in large to semi-large companies becoming a norm.Seeing the stocks that are still strong,it’s clear that this is a very risk-averse market.Now,the situation is the exact reverse of Jan. 2018…good news and stocks fall less or fall later while on bad news,the stock gets hammered.Every part of the B/S is being scrutinized,management assurances are failing to make an impact,volumes have dried up…smallcap is a bad word now.

Investors who have been around for a while would recall that this is a bit similar to what was happening in 2013.2013 was also a pre-election year,macros were worsening,economic data was weak,NPA issues had just started surfacing.There would be a lot of accidents in the broader market at regular intervals.Stocks like Core Education,construction names,realty stocks had taken the biggest hit.You would switch to CNBC half-anticipating what stock has bad news today while the other half would be praying that it’s not your own portfolio stock.This all when stocks like Avanti Feeds were available at 4x trailing earnings at 4% dividend yield and would still stay in a narrow price range.Volumes were wafer thin.Similarly,good parentage,good growth and quality companies like Swaraj Engines were available at single-digit multiples.2018 is not as bad as that.However,there has been a sharp change in the tone of the market in just 4 months.High bullishness to bearishness now.Lot of people have lost a lot of paper profits and want to stay away from equities.

IMHO there are two ways to play this.Either hide in strong names like Asian Paints,HUL,HDFC twins,some strong midcap names like Hikal,GMM Pfaudler,Garware and wait it out.A second way would be to really dive into researching names with a strong earnings track record,good outlook,good managements whose stocks have fallen inspite of good numbers.Best part is,market is now giving enough time to study and pick up decent allocation in names you like.Not all microcaps have issues and not all smallcaps are useless,shady companies.There is no need to hurry to buy if you find a good name…buy slowly.2018 being a pre-election year,there will be usual uncertainty leading upto 2019 and we could have small corrections or big ones depending on how markets perceive it.

Good quote to remember this year: “Perception of risk is the highest when it is actually the least”

Disc.: I am almost fully invested so maybe I am being irrationally optimistic.

19 Likes

I hate this logic … Price is what you pay value is what you get .

Its still foolish to buy something at 60 PE (very quality stuff ) and see it correcting to 30 PE and saying in a long run i will do better .

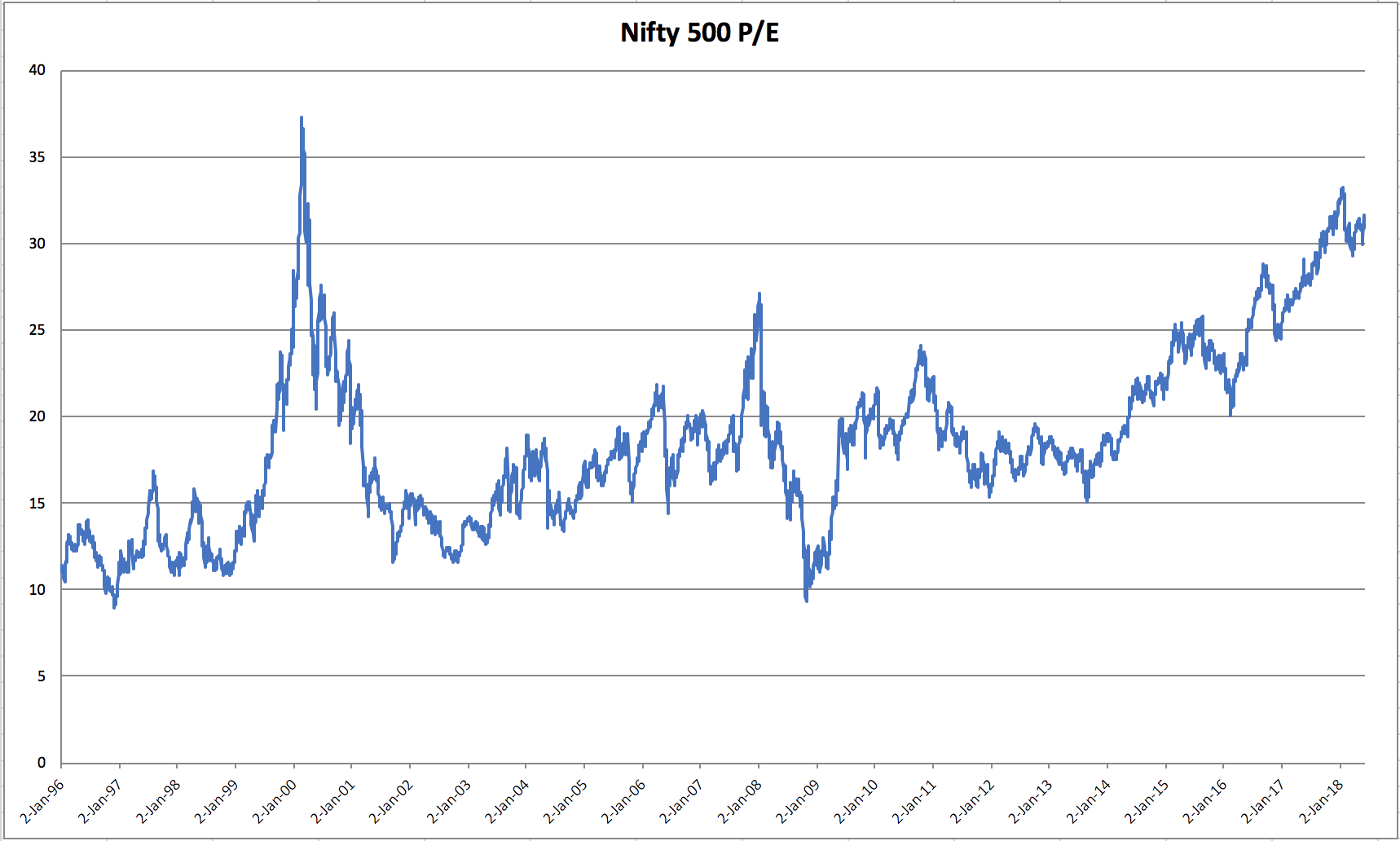

No you will not and above chart shows that.

guys who will buy your quality stuff @ 30 PE after -50 % correction will do far superior than you.

CRISIL , Wonderla etc all quality businesses but some people preferred to pay 60+ PE for them in 2015 , unperformed the market terribly bad since then.

Not only you hurt yourself by paying this high for quality business but make life hard for all fellow value investors as they have no option but to park cash in liquid funds till you decide to sell it at 30 PE (the same 60PE stuff )

Chart from -

9 Likes

I think its useless to get stuck on the PE ratio in isolation. One needs to know about the company’s strengths before paying a high PE.

Not all high PE companies are risky. Similarly not all low PE companies are safe.

One cannot generalise these things in isolation. When markets correct it becomes fashionable to talk about buying low PE and selling high PE and so on.

The actual truth is usually a bit deeper.

High quality companies which are dominant in their sector/niche (even though they maybe small/midcaps) will remain expensive unless there is a 2008 kind of meltdown which is once in a blue moon phenomenon. Market participants have the perception about these companies that they have a very very long run way for growth and they can afford to sit out periods of high PE till earnings catch up.

e.g Gruh finance with what many perceive to be having very expensive valuations one year back has doubled in 12 months and become even more expensive while sceptics have watched on. And all this while the other housing finance companies were receiving a drubbing. Similar could be the example of dmart.

I think the key to investing in small/midcaps (and even large caps although these are very closely tracked by analyst community) is to have a detailed focus on the company itself and analyse its prospects and strengths and weaknesses and then take a call.

51 Likes

Dear @hitesh2710 Bhai.

Here is the one and only reason I am actually fearful. Rest everything is all secondary but actually everything I am worried about is coming from this one fact.

The Nifty 500 Price to Earning from 1996 to date.

This says to me (thus I am hoping you might have an opinion to share) that buddy; this is the top 500 companies of India. This is not Nifty’s 50 or Sensex’s 30 stocks. This is more than 90% (I think actually maybe 93%) of India’s market cap.

And it seems to be at a place where as a market as a whole we have put such high valuations on our entire country’s listed business universe. It is way higher than even before the 2008 carnage and at level with the carnage before that in 2000. Whatever I can see is data, I have no direct experience of going through them.

And because of where our entire country’s listed PE ratio is; thus I feel a crash may come is more probable than earnings will come at such warp speed to make up for it.

I am in fact surprised that till today it has not course corrected (I guess due to the amount of liquidity than came in last year) and thus the more time that passes by the more I feel it is becoming imminent. It is like WB said, every year we go without a nuclear attack, the probability of it happening increases ![]()

Honestly I feel, that when it does really course correct, it will take everything with it in the ensuing tsunami, small, large, mid, nano, honda, maruti and anything that is invested ![]() Thus I feel whatever good quality or whatever, it will be blown in the ensuing mess so why take a chance even on quality, it is not rational times when I see this.

Thus I feel whatever good quality or whatever, it will be blown in the ensuing mess so why take a chance even on quality, it is not rational times when I see this.

Where am I going wrong?

Or am I at least justified in my fear?

Chart attached: 1996-2018.xlsx (224.4 KB)

15 Likes

Off course there will be exceptions in the market where high PE stocks will consistently give high returns but majority will underperform.

1 Like

MY 2 bits

I ask myself with my limited knowledge & some understanding of the companies i hold a few fundamental question most of the time when i invest

1- are they debt free 2- is the company making money 3) are there favourable/unfavorable head/tail winds 4) the market size of the industry & the opportunity size of the company , no PSU, Regulated business, if cyclical/Commodity-i will try to understand where am i in the cycle

After the carnage of 2008- the markets went up 70% plus- so those who beleive in “this shall pass too” is a reminder that its true.

Are we in a 2008 kind of situation- i dont know- i dont understand macros that well- so most of my investments are stock & industry specific. if i have followed some discipline (Not always-but mostly yes) & if the market falls like it did this month or like mentioned above the markets might fall even more because of high PE i will reconfirm with my above fundamental points to guide me- wether i should stay the course or bail out.

There is so much noise out there & since 2017 the liquidty related bull has managed to snare a lot of people (Me too- in some buys done mid 2017 which i didnt get out of completely). So its ok to have made some mistakes.

Its only in times like these we begin to see things clearly & realize some of those mistakes.

So if you have not bet your house on the markets & are not super leveraged- then you can be afraid as much as you want but to no avail- you will be just fine

Fear is good- in a limit beyond that the effect of the fear is wasted, It should galvanize you to clear up your portfolio not paralyse you into inaction.

I have had a few ‘aha’ moments lately after the falls & like @hitesh2710 & @ayushmit mentioned, will use this time to evaluate ways to get my capital out of the duds .

I am rather glad, this happened, because the tension that markets are heated & bound to fall in some ways worse than knowing it has fallen & acessing the damage.Chances that it may fall further is there- how much -again i dont know. But we all know that it wont go to zero(PUN intended).

Duds deserve to fall , but many of the good ones have fallen too- & they will not stay there for long.

8 Likes

Latest news on ASM:

Looking at the frequency of posts in this topic, it seems that the midcap/smallcap carnage has subsided for now.

9 Likes

I don’t care what anyone has to say. I am a bear and all of you can laugh at me all you want. This is DEAD CAT BOUNCING  . Everyone has a right to be wrong, and I also reserve the right to be right. I will not change my view. Humph.

. Everyone has a right to be wrong, and I also reserve the right to be right. I will not change my view. Humph.

7 Likes

I think the experienced and seasoned investors in the forum have shared their views on the current situation. At this point more effort is needed on generating ideas and opening new threads on companies not covered by the VP community or adding quality content to existing ones.

I am sure all of us like to market muse once in a while but if we can simultaneously also contribute to existing company threads and provide qualitative & quantitative insights it would be really useful. Our collective job is to unearth ideas and provide insights that will help all take informed decisions.

If we do not do our homework properly we will all lose money over time.

32 Likes

I agree with Bheeshma and I understand the rage I could face for writing what I am writing below but then nothing wrong in getting some beatings from colleagues

If we see volume of posts in last 2-3 months, I could categorize in following manner

- Lot of theoretical learning

- Lot of price based discussion

- Lot of discussion based on what THE BIG INVESTOR did

- Few few discussions on doing valuations of a company and related stuff

I believe point no 2 and 3 should never be entertained unless it is backed by supportive content on research and valuation rationale, point no 1, I have no apprehension over point no 1 but too much of point no 1 but missing point no 4 is like Indian education system with lot of theory but no practicals

This is just my feeling of last 1-2 months and pardon me if feelings are hurt and its just a qualitative feel (and I consider myself equally responsible).

Glad that bheeshma pointed out. I will be doing my bit soon. Working on an interesting opportunity and will write about it soon. Mostly this weekend. Lets get back to what the forum stands for - “separating wheat from chaff”. Lets do some more company focused research and valuation. Cheers No hard feelings

42 Likes

One learning that i had was -

- Its good to have a flexible mind

- Stocks go down but not to an extent but not neccesarily entire market goes on sale

- Its good to always have some cash on hand

- Keep adding if market corrects by let’s say 10% everytime no one know bottom, so in a bid to wait for better prices, stock may go up. Good stocks eventually do go up.

- Its always better to do own study to realise which stocks to keep and which stock to sell out in case of steep decline.

- Good stocks do not remain on sale zone for very long

- Its much easier to add when one is up 2X -3X on a stock and I am still in profit despite fall, then to. Most of my portfolio if very new and last 7-8 months have been tough and I am net net negative at portfolio level and all the theoretical knowledge fails when one sees negative returns.

1 Like

Looking at some of the posts in this thread, I find there are two types of investors with distinct investing styles

Type 1 - Graham style cigar-butt investing

- Buy a stock at a price so low that it is likely to produce a one-time return as the gap between price and value closes.

- Focus on margin of safety

- Sell when your holdings become overvalued

Type 2 - Munger-Buffett style Moat based investing

- Buy stocks of high quality businesses (at a fair price) which are protected by unbreachable ‘economic moats’.

- Focus on the performance of the company; not on the performance of the stock. If the business does well, the stock eventually follows.

- Don’t try to ‘time’ the market. Buy right and sit tight.

“I think Ben Graham wasn’t nearly as good an investor as Warren Buffett is or even as good as I am. Buying those cheap, cigar-butt stocks was a snare and a delusion, and it would never work with the kinds of sums of money we have. You can’t do it with billions of dollars or even many millions of dollars. But he was a very good writer and a very good teacher and a brilliant man, one of the only intellectuals – probably the only intellectual – in the investing business at the time.” – Charlie Munger, The Wall Street Journal September 2014

While cigar-butt investing might not work for Buffett because of the huge cash pile that Berkshire has, it might still prove to be a good strategy for small investors. But the question is, in today’s age, is Graham’s style of investing more profitable than the Munger-Buffett style, for small investors?

5 Likes

Great post.

But the basis of the post says that Warren Buffet was famous for Value Investing, which may or may not have been his fault. He himself never believed in the concept of ‘Value’ in the traditional sense. Hear it from the horse’s mouth:

We view that as fuzzy thinking (in which, it must be confessed, I myself engaged some years ago). In our opinion, the two approaches are joined at the hip: Growth is always a component in the calculation of value, constituting a variable whose importance can range from negligible to enormous and whose impact can be negative as well as positive.

In addition, we think the very term “value investing” is redundant. What is “investing” if it is not the act of seeking value at least sufficient to justify the amount paid? Consciously paying more for a stock than its calculated value – in the hope that it can soon be sold for a still-higher price – should be labeled speculation (which is neither illegal, immoral nor – in our view – financially fattening).

Just a small nitpick from an avid WB follower.

1 Like

Pardon if I am deviating from the topic as the latest posts in the thread have been a bit towards the investment philosophy rather than the recent fall.I would think the recent fall would be a good learning(To me its looks very normal if one looks at the history ) for the every one into the world of investing as I am sure some would have made good money in these small/midcaps in past few years and think they have found their niche.

I have been having thinking for quite some time on what will be the right investing strategy for me going forward and this has been a tough one with my views fluctuating periodically(been influenced by books ,successful investor talks,articles and even market returns).

To have an analogy with cricketing batsman,I believe whatever may be the type of investing, one need to identify the style which suits depending on your temperament and behaviour after acquiring decent knowledge.

You could be a Dravid or Pujara,develop a sound technique,be patient, spend time on crease(market) and waiting for the right time to score of the easy deliveries and accumulate runs(wealth )over a period of time.

You could be a Sehwag or Warner,trust your game ,be aggressive ,don’t mind losing the wicket a few times and also could be successful

Or you could be a Sachin or Kohli,combing both the aggression and defense depending on the pitch and match conditions and be successful.

You could even be a lesser batsman like a first class cricketer who is contend with the returns he is getting from the game

I agree its not easy to identify the right fit quickly as only after doing actual investing and going through several up and down turns ,you tend to have an idea of whats working for your and whats not.

The reason why value investing finds mention a lot of times is that the literature which is built around it goes beyond the world of investing.Its basic tenant could be applied to any walk of life .It may not be the most successful way of investing but it provides a lot of wisdom to the new comers on behaviour,protecting one’s capital and doing the right things irreseptive of market conditions.Once you develop that sound base you could take into any type of investing and be fairly successful.

4 Likes

This post could be a digression and if Mods think so, please delete.

This brought more than a chuckle to me. I feel I know exactly what you are talking about. Though I hope I am never vain enough to say I know it all, I am a Buffett aficionado and really don’t know how to make money otherwise.

But I am certain that there was, there is and there will always be one other way, that you obliquely referred to ![]()

Many many years ago when I was naive and wanting to make money, my eyes were full of love and romance listening to the Dalal Street-ers and fund managers who would tell us on TV and print, how they used their wisdom and intelligence to make outlandish returns. They were real celebrities for me. They would make it appear that they could analyze any situation to make money, they seemed to have the canniness to size up any industry or promoter. They would speak with such confidence that you feel you stand no chance against them!

Yet as time passed and events unfolded, hearsay reached you, and as facts presented themselves, you realize a good bit of it was to know beforehand what was up, by talking to management (now called Insider Trading). In fact (as is usually the case) in an uncontrollably overweening moment one hero-worshipped fund manager said that he speaks to management every three months, and their fund is in constant touch with every management whose shares they hold. Of course how it could it be otherwise. This was before the now stricter insider trading rules.

It was not one or two managers, I felt it was probably the norm.

I know exactly the manager you are talking about here and the case with SEBI (I had some grounds to believe that was the reason for relocation), though I think he was exonerated. But you can see him pouting wise cracks every now and then - he can afford to ![]() . Likewise I often find that after people get rich and become celebs, they suddenly find their lost conscience and start touting honesty and good governance, with stark memory loss of their own past behavior!

. Likewise I often find that after people get rich and become celebs, they suddenly find their lost conscience and start touting honesty and good governance, with stark memory loss of their own past behavior!

It happens again and again with old stars fading out and new ones coming in. And even as the then novice investors wisen up with time, the younger ones queue up; now with new star managers. What Munger said, a German quote I believe, - you are too soon old and too late smart, occurs unfailingly every cycle

Sooner or later many of the stars in this cycle will fade and will be replaced by new ones. Very few are enduring. Buffett is one of them!

10 Likes

Hii learning…i have ventured into stock market since last year october…earlier i had this theoretical policy of adding at every 5%…but with past two months experience i have decided to add up at every 10% since 5% movement is quite frequent…i would like to share few points with you -

-

One needs to be convinced of the growth story in that particular company for adding up at dips but we need to continuously look for any piece of adverse info which can change our conviction…i frequently visit money control forum, screener.com and google alerts for such an info…

-

I like to follow the theory of maintaining my reserves as military commanders do in a war…so i keep around 40% amount of reserve cash in debt funds and higher rate saving accounts…as ill grow more confident in the market this amount may reduce…as a salaried person this seems to be more suitable for me…

-

But with the educative words of many seniors i realize that at some point of time we need to learn technical analysis as it will help us to broadly recognize the stock movement…for example KEC international went steeply southwards after posting superb result…if we could identify the broad extent of its southern move we could have deployed our cash more judiciously…i remember an investor on its moneycontrol forum quite accurately predicted its movement by judging the technical aspects…

Im still quite far away from learning technical analysis as im learning fundamentals of preferred industries initially…i have learnt basics of aviation, insurance and banks till now and now im working upon pharma sector…so im working gradually upon building knowledge base first…with a tuition fees paid to market by investing money in vakrangee, i feel a top down approach is suitable if one has adequate time to read…

Please share some of your views on your strategy for my purpose of learning…

regards

2 Likes

I am cautiously optimistic on quality midcaps where Q4 results have been good , valuations are reasonable and one should buy on dips.Earnings are catching up and stock prices will catch up eventually if earnings are good. I don’t think that large caps are at juicy levels and money would flow back into midcaps once we get clarity on Modi coming into power in 2019 or not. One should look into sectors like chemical where corrections has been deep, building materials and hotels. Today’s scenario is not like 2008 where world economy is doing good and i see 10000 levels for nifty as strong support but caveat is nobody can predict correctly.

2 Likes

Ah a very good discussion is going on…and apparently by quite knowledgeable investors. But what if someone (yours truly) has done a bit of reading AND comes to the conclusion that he / she is not a good investor, and can never be even a fraction of the Stalwart investors and is at most a person with mediocre intelligence and knowledge.

Even the mediocre investor wants to make money in stock market…so how should such an investor go about this investing thing?

In the last two steep corrections of feb 2015 and dec 2016 (or for that matter every deep market correction)…every time a different set of stocks became multibaggers…and every time it is stocks which the retail investors considered as laggards… stocks such as escorts, venkeys, jayant agro, sudarshan chem, edelweiss, action construction, heg, graphite, goa carbon, rain, tirumalai, tinplate etc …all had only one common charaterristic…they were in a rangebound price movement for a looong long time and had not participated much in the bull run earlier…

everybody is saying that this fall is a good opportunity to buy your favourite stocks / good stocks at a lower price…i too used to think on similar lines…but have realized after a lot of missed chances that…the most appropriate behaviour for investors is …NOT TO BUY INTO THE FALL…but to buy into the upside breakouts after the fall…

Buying into the fall is mostly like still fighting the previous battle…or betting an a aged and tiring bull or a wounded bull…buying the breakout is like betting on a fresh and young bull…

So a mediocre investor would suggest that we should keep a watch on stocks which have been under consolidation for a long time…and stocks which are the ones to have an upside breakout after this round of market fall is done with…among such stocks select a few with reasonable valuations/ good mngt and some sectoral tailwind…and invest in such stocks…

This may be the way to making money in a bull market and profit from sector rotation in market.

while we may have a list of stocks after the end of June…a few stocks which look to fulfil the above criteria are…SAIL…HIND COPPER…AKSH OPTIFIBRE

21 Likes