No body is guiding any one …we are just sharing thoughts on current situation. You are welcome to share your thoughts and do what u think is good for u

By the way what is a Bayesian updater?

Globally the movement is towards branch less virtual banks & wholesale lenders. So disruption is for real. How it impacts Indian Banking system which has its own set of problems is what you need to get in depth. Public banks / Pvt Banks/ NBFC. Is it going to be end of banking globally - Answer is No but the change is imminent…It will be slow to take shape in India and early adapters are going to benefit

Bayesian updating is just updating probability of future events as new information comes in. This way we will never stay too rigid to one stance and adapt to low-contrast events i.e small changes that trickle in that can slip us which we otherwise may have reacted to, if all the information came together. The marvel that is the human brain does this naturally as long as its not tied to an adverse stance or experience. Fear, greed, wanting to be right (ego) by choosing a side and sticking to it all come in the way though.

So allocations tied to probability (in this case asset allocations) should more or less reflect the new inputs that come in. Similar approach can also be used to allocations within an asset class like equity which has been discussed beautifully in this thread. Kelly’s formula as well is a wonderful tool for allocation within an asset class, similar to what’s discussed in this thread. In this context, applying Bayesian updating will require you to change stance i.e conviction as the thesis behind the conviction diverges from reality, requiring you to reduce allocation according to the probability/percentage of divergence.

All this involves costs though - both in terms of time spent and also cost of churning so it is very important to know the importance in terms of impact of new information that trickles in. This is something I have been practising recently and struggling with it to be honest, as it takes away both the highs and the lows. You never feel the highs of being right nor the lows of being wrong. It does get rid of the hubris of being right and the humbling of being wrong though.

4 Likes

I think P/E Ratios reaching a ‘new normal’ is just humbug.

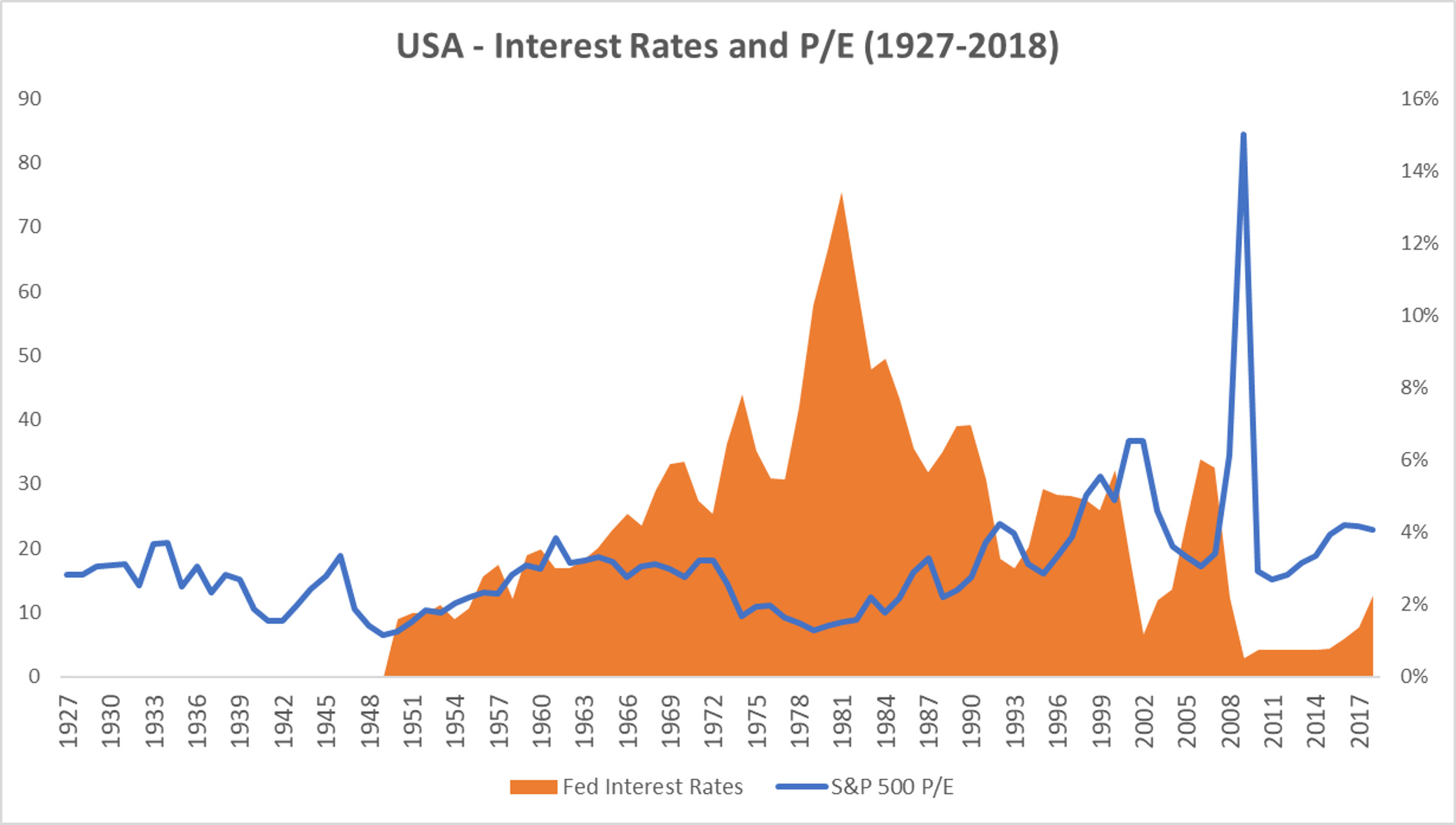

This is the US market-related data of S&P 500’s P/E Ratio (1927-2018) and Fed Rates (1950-2018). It appears to me like there’s a short term trend in the P/E when interest rates change a lot. But it always moves in and out of the long-term average, which is about 17.16.

The culprit then, is the Equity Market Risk Premium. As I’ve claimed elsewhere, Interest Rate can and will cause short term reactions in the markets (Well, literally any policy news can). But the absolute rate of interest matters very little in the long run. The ERP make sure of that.

What is the ‘P’ in the P/E Ratio? It’s Price, of course, which is proxy for the Value of a company. In the simplest form, the value of a company can be given as:

P = (1+g)/(r-g)

Where g = Growth in Earnings and r = Cost of Equity Capital.

‘g’ or Growth in Earnings is determined by Economic Development, which is aided by Interest Rates. In turn, ‘r’ or Cost of Equity Capital is also a function of Interest Rates, except it contains one more component: how much investors look forward to earn in excess of existing interest rates. I would ideally like to go into how the CAPM and the ERP help the market mean-revert, but I feel that would be overdoing a simple explanation.

In the end, everything is a function of Opportunity Cost. In the land of 2% interest rates, I will yearn to have 4% returns or more on my capital. In the land of 8% interest rates, I will yearn to have at least 10% or more. That’s the only truth I know and the rule with which I operate.

4 Likes

Sir @dumboinvestor . I am a novice who is leaning and with very limited knowledge. So please pardon any mistakes.

Sir here you said;

And then in the next line you said;

Sir. Just for learning, you are saying that you love how humans make farfetched and deluded predictions.

Then sir in next line you are predicting what will happen to Nestle at high PE.

Sir, how?

I understand sir you knowledge must be vast to inform us on this but sir, maybe you have some “hero” bias sir; where you feel you know everything sir?

I am just pointing out so you can point my mistake in understanding if any that we are not able to understand your vast knowledge.

I feel sir, you are some big investor like RJ or similar behind the dumbo id.

Please sir, if we did not feel humiliated we might learn more sir.

If sir, you don’t mind my having been little direct although I was little worried because I didn’t want to incur your wrath (because I am novice) but still thought of mentioning sir that please if you you spoke to us more kindly considering we don’t know anything then we may learn more from you. Sir, even @jamit05 how much I saw you told him like PEAmit and all other words, but he is talking back to you decently and trying to learn from you. Please help us sir, but please treat us with kid gloves. We may seem like children sir. But we do want to learn from your fountain of knowledge.

I apologize if I stepped out of my boundaries sir.

But if you treated us like little children and not as if we are total idiots ( although we are little idiots if not total, but somehow I think but you will assess us better) then we may have the blessing of learning more from you and it will feel more pleasant to us sir.

Yours humbly.

PS: Very sorry if I may have said anything that seems childish and silly sir.

26 Likes

I think it is a good point you are raising. No need to be so apologetic. With due respect to experienced forum members who contribute a lot, this forum is for everyone - to challenge each other on their view points and make the best use of information. By raising a question you are not offending anyone.

1 Like

With technology there is going to be disruption in banking no doubt. However the question is who are going to be the disruptors? My take is it is going to be the companies which are primarily classified as banks/nbfcs. Fintechs will have their place maybe in pockets where banks and NBFC’s might not be willing to cater like MSME lending, but to say that they are going to say win against banks like HDFC or NBFCs like Bajaj Finance to such an extent that it will make these investments unattractive is I think far fetched. The most successful NBFC company over the last 5 years that leveraged technology is Bajaj Finance and not some Fintech company that got into lending

Regarding the Wealth Creation study I think Infosys was trading at over 200 P/E during dotcom bubble of 2000 and not during 2008 as mentioned in the slide. The interesting thing for me is even if you had bought Infosys at 200 P/E you would have still made 8% plus dividends over a 18 year period, not great but still higher than tax-adjusted FD returns. In fact Infosys over the last 7-8 years has been plagued by issues with the management if you had sold that stock in 2010 you would have made around 12% plus dividends which I think is extraordinary considering that you invested at 200 P/E. This example makes a case for investing in quality even if its a little bit expensive (obviously not 200) but I can see why people think they can make decent double-digit returns over a long period of time by investing in companies like HDFC Bank, Asian Paints, Britannia, Bajaj Finance etc even at these levels

4 Likes

SIP strategy works well in top notch companies even when price is expensive at the beginning and the investment time horizon is 10+ years.

3 Likes

Also, where would one like to be

- a market where earnings are depressed at 3% of gdp, where currency has Already weakened n GDP growing at 7-8%. 1.3 billion young population…

Edit: and low oil prices again lending support.

OR

- A market having earnings of 11% of gdp? And Currency already at tops.

1 Like

Thoda detail me explain Kare, the repercussions of both the cases in our economy. Ty.

1st option is Indian stock market and the second is the US stock market.

Why is that, If you invest sensibly in quality companies. Didn’t you notice Vakrangee was top holding of a fund and manpasand very substantial in holding in few. They invest is all types of junk on your behalf and keep churning.

Substantial portion of revenues of S&P companies comes from overseas market, I think for S & P tech it is something like 60%. So a lot of US companies have access to the entire world not just a population of 1.3 billion, that is why you have trillion dollar US companies (by Mkt Cap) growing at over 20%. I am not favouring one market over the other just saying this top-down approach is too simplistic.

2 Likes

But don’t you think a second order question would be - what has changed in the energy market that crude has suddenly hit one year low after hitting multi year high? What has changed in last one month? It’s definitely not US shale supply gush like 2014. Was it due to speculative unwinding? Was it due to global slowdon? Was it due to demand destruction?

Except for 2014, other crude crashes like 2008, 2013 and 2015 are coincidental with equity underperformance. Crude crash is definitely positive for Indian macro. But is it positive for Indian equity market? I am not so sure as historical analysis suggests otherwise.

Just trying to process my incoherent thoughts.

3 Likes

Oil rallied in anticipation of supply crunch due to US sanctions on Iran taking effect in November. What actually has happened is that other OPEC members are pumping more to offset drop in Iran supply. US also granted short term concessions to few countries (including India and China) to continue Iranian oil imports. So supply crunch hasn’t materialized as expected and US oil inventories are growing indicating ample supply. All the scarcity premium built in oil price since June after announcement of sanctions is gone now.

5 Likes

Explaining every fall or rise with a headline is a journalist’s job. Oil price movements are purely speculative on geopolitics/trading but made to sound like its a supply-and-demand issue. Even if it is, these are more near-term than long-term. Long-term there are clear signs of oil glut. I don’t know if its good for Indian equities or not, as that’s not something I can base any decision on. I know however of what companies will benefit from lower crude and how their earnings can grow through margin expansion (Specialty Chemical companies with crude as a RM for eg.) and that’s what I intend to focus on.

4 Likes

No one is saying that banks will disappear … If the leaders are early adapters they will still be in game… More over Banks still need licence to do business in India it is very much protected but with new technology will usher some new challengers.