I do not track both stocks closely, but I do track other very closely and sector in particular. Here are my two cents

1- Kelton Tech- Based on my limited understanding of the company, the management is keen on growth, but they have relied more on inorganic than organic. They have made few acquisitions lately, and it has boosted the sales number. Overall, growth is good, but the market does not like inorganic growth much. Inorganic growth can certainly make magic, and the acquisition certainly can pop the share price in the short term, but long term, market reward organic growth. When the expectations of high growth are built into the stocks, any disappointment leads to price correction.

2- 8k. I find it hard to imagine sustainable advantage company can have in implementing cloud solution. Agree, a company may have a head start in particular niche, and they would dominate the niche for some time. But implementing cloud solution is certainly not likely to be the sustainable niche in my view. Any big company having the decent budget would train few people- if not army- to implement cloud solution. This is another company which is growth focused (or obsessed?). Any disappointment in growth has a Lollapalooza effect, except in reverse- Small reduction in sales, caused more reduction in PAT, which in turn reduces the PE multiple further. The stock was also priced for perfection. Any disappointment could cause a severe correction.

We can discuss the merit and problem with the company. Do you have some data points or specific information as to why a company growing at around 100% yoy is trading at such a ridiculous price and going down by the day?

I am also looking forward for the same information. Not many investors or mutual funds are interested in buying it. There should be something which we don’t know but the market does.

Friends… IMV… It is just sector headwind…Re appreciation… And

dividend reduction and recent pledge has made matters worse… It is a

good opportunity for someone having no exposure to enter now… Or whoever

has it to average… When the sectors gets tailwinds, 8k will be the early

beneficiary…

These type of statement takes you no where. With this as the basis of thought process one will never be able to find a stock which is mis-priced by the market.

If you find something specifically wrong with the company, please bring it to fore and I am sure members will jump in to analyses and as sages say will separate wheat from chaff.

I don’t know much about the technical aspects as I am not of commerce background. However by going through the Moneycontrol board there are some red flags regarding intangible assets. One person there is saying that the company has 155 crores of intangible assets plus 20 cr under wip vs 15 cr of tangible assets. May be you can understand that and it’s implications

I can understand the Software, tools, Patents etc, How do you quantify Goodwill - ~ 22 Cr? ( If I am not mistaken Virinchi - the other share I bought during a distress selloff recently had also similar consideration - I could be wrong).

Entered below Rs400 recently, as I felt it is unique business with high growth visibility atleast for the next few years and the controversies and issues are not of long term nature.

I have written my queries ( pledging, receivable days, Borrowing vs Cash etc to their CS. Will update if I get a response.

I went through the thread at Moneycontrol. The company has lot of intangible assets, no denying from the facts. The reason for same are

The company is software company and software company is supposed to have lot of intangible assets. Software companies do not have plant and machinery.

Company has been doing lot of acquisitions along the way, the money paid to company acquired over and above its face value is shown as Goodwill and Intangible assets on the book of acquire company.

Acquisitions

Cornerstone Advisors

NextAge Techh

Cintel Systems

Mindprint

Serj Solutions

It is true that the company has not written-off the Intangible, but I do know of any reason why intangible assets should be written-off. I will be delighted if someone could through some light on the reasons for same.

Now the boarder has expressed concern that since company has lot of intangible assets company may be capitalizing its expenditure ( it is a fancy word for saying that instead of showing expenditure in profit & loss, company is showing the expenditure as assets and adding them to intangible assets). I do not think we will ever know this but as far as I can think we can do a comparative analysis of other similar companies and see if expenditure as percentage of revenue of 8K Miles differs substantially.

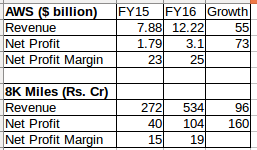

Here is a comparison of growth in Amazon Web Services and 8K Miles Software. The point I am trying to make here is - 8K miles is growing at such a frantic rate because the underlying business itself is growing at such a phenomenal rate.

These type of growth are not easily seen therefore it is obvious that some investors have raised red flags.

Additional growth in 8K Miles may be due to its

Smaller size than AWS.

Acquisition boost.

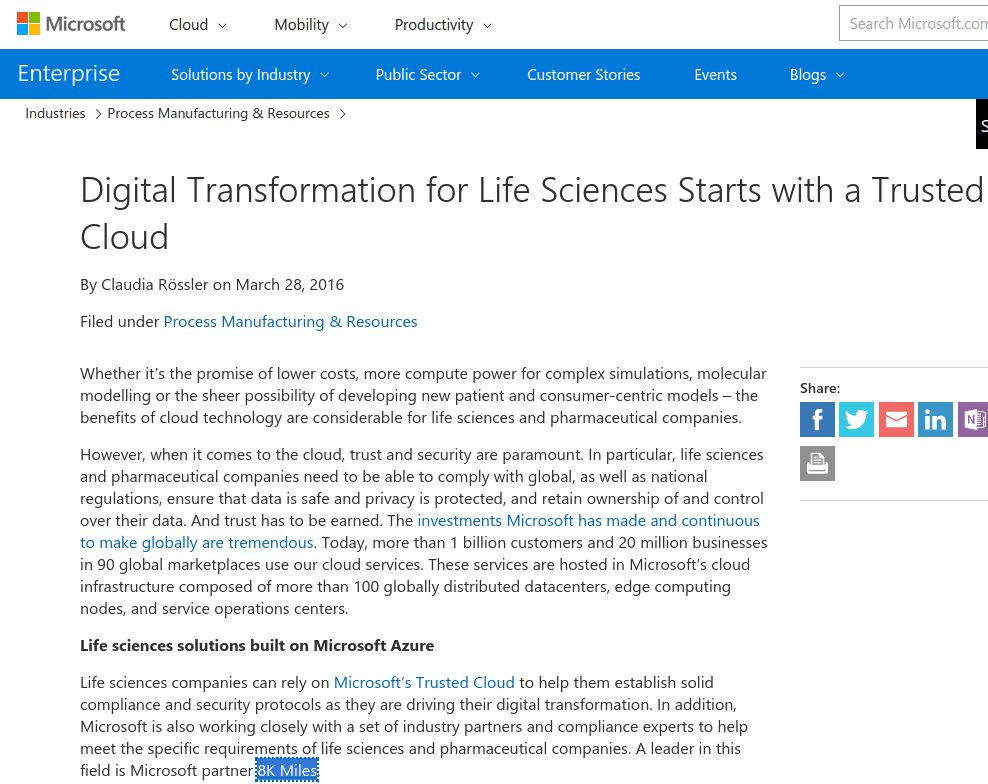

On a separate note Microsoft on its own website has mentioned 8K Miles as a leader in Life Sciences & pharmaceutical space for Microsoft Azure.

Yes, I saw that earlier as well. Amazon and Microsoft are prominent names and that makes me comfortable. However as a layman I just wonder why prominent funds and investors are not buying it. Also with such a rosy growth and outlook it should have shown strength and consolidate but it is going south everytime.

To me it seems they are doing too many acquisitions and very few of these eventually pay off. Could this be the reason that investors are keeping away?

That might be the reason but to me it seems market does not believe in such great results QoQ and believe that there is some kind of information which is hidden and numbers may be bloated. Also irresponsible management whether it was in dividend fiasco they don’t come up on screen and clarify.

A lot of funds would be dissuaded by how little Cash in CFO ends up in bank accounts rather than overseas subsidiaries. The company had revenues of 271 crores last financial year but only has 3 crores in bank balance and there were short-term borrowing of 2.5 crores.

Why exactly are profits being ploughed into overseas subsidiaries? Management hasn’t explained the benefit of this approach.