Although I have one question inspite of good results the stock has been sharply corrected from 52 weeks high.

Is that something Mr.Market knows that we are unable to figure out,

Since you are tracking (and everyone as well in the forum) very closely , any thoughts on this

Some of the vp members have addressed this question earlier on this forum itself, if you read this discussion thread from start to end. However, following are my thoughts, but I may be wrong:

Lack of awareness by investors about the potential of their business. My opinion is that, an IT professional may be able to understand it the best way.

Overall IT sector itself is not in limelight currently. Many investors, who do not really understand the Cloud business are anxious (rightly so), if 8k will be able to reproduce its past outstanding performance in the future also, especially when other established Indian IT players are currently struggling with their growth rates.

In the past, people had concerns about certain errors in their financial statements and corporate Governance. I do not know, if those concerns are still valid.

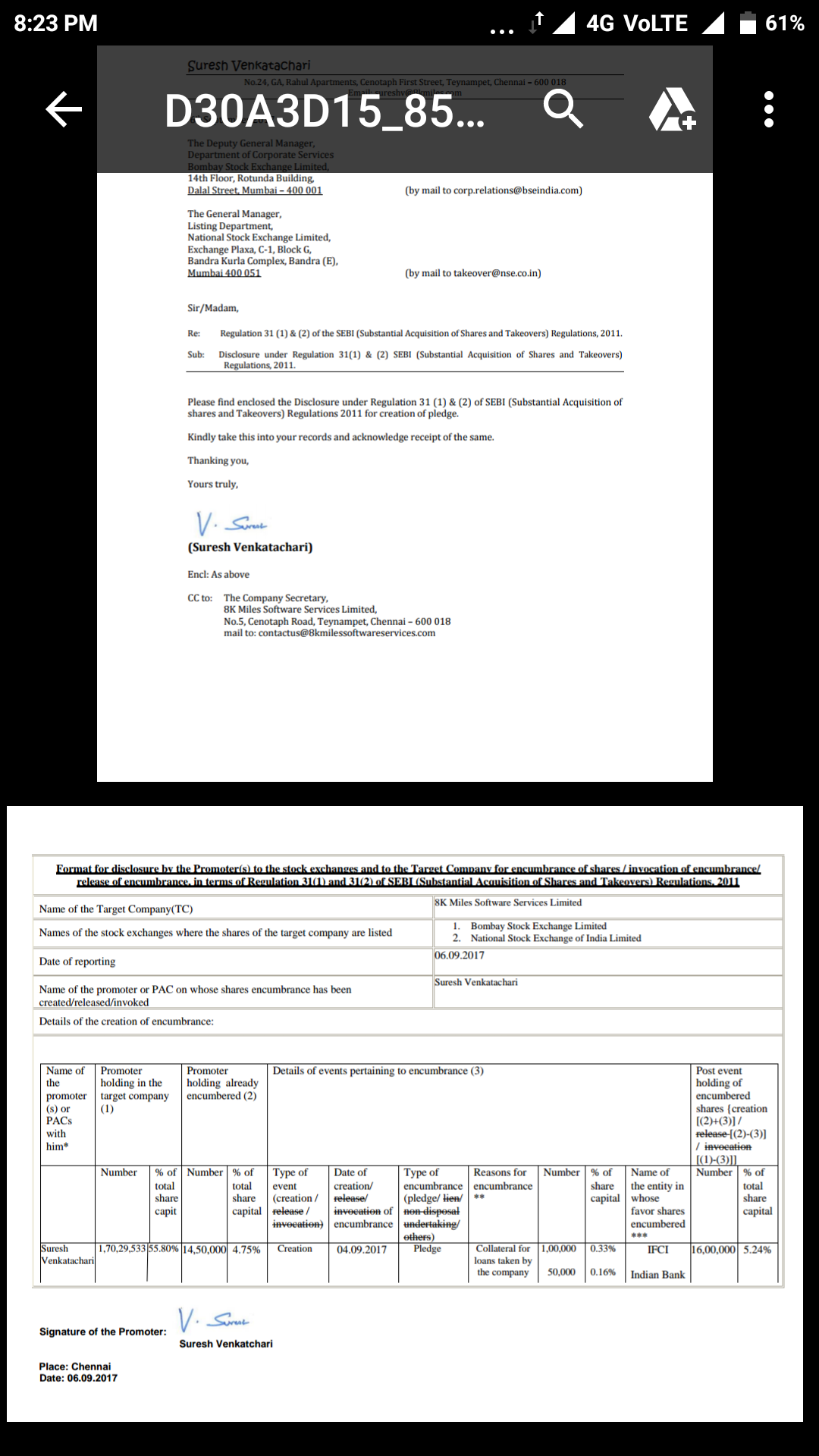

8k made an acquision in may17 for 66cr. How much of the PAT is from that aquisition this quarter? It made an acquision in Q3 last year too. What’s the contribution from that in PAT of this quarter? If we strip of PAT of acquired companies, is there growth? Easy to grow by paying for growth? where is the info to evaluate that the company did not overpay for these acquisitions. Current goodwill amount is over 200cr - more than half of its networth! an indication of what 8k is paying over and above the cost of assets acquired.

Regarding the Cornerstone acquisition, what I know is the following: As per the interview given by Suresh Venkatachari on 20-Dec-16 (http://www.moneycontrol.com/news/business/companies/8k-miles-chief-sees-cornerstones-eps-to-be-positiveyear-1-936878.html), Cornerstone revenue yearly approximately is USD 10 Million, hence let us assume that, out of the Rs. 167 crores revenue this quarter, Rs 17 crores are from Cornerstone. Cornerstone margins are close to 20 percent, hence let us assume that their share of profit is around Rs. 3 crores.

@madhavikkutti : I looked at ROE, ROCE, Past 5 years Sales and Profit growth of 8K Miles and wondering if there is sufficient analysis done on this company by investors.

If there are any analyst or investor reports or any detail analysis available, I am interested to have a deeper look on it. It seems that, its offerings are unique due to which it can grow almost at > 80% for past 4-5 years.

Being from IT industry with detail understanding of services and product business, I am wondering about its growth story.

Dear GSApte, Ambit Capital had pointed out certain discrepancies in 8k’s past financial statements in a report it came up with during Sep-16. If you read all the earlier messages from the vp members on this discussion thread, you can find about that. Apart from that, I am not aware of any investor reports. Suggest that you search in Google News for all the news about this company for the past couple of years and read those.

My doubt is that, the hangover created by the above Ambit report still exists in the minds of many of the investors and they still look at this company with a “suspicious” eye and tend to disbelieve such a massive growth story. To add fuel to the fire, very few investors understand the cloud technology and its potential. These are possibly the two main reasons about the undervaluation of this stock.

I am also a person from IT industry and have some good understanding of their business model. Based on my research, I do think that, their growth for the past 4-5 years is an achievable one. However, I am not knowledgeable and competent enough to challenge any of the discrepancies being pointed out by Ambit.

Thanks for quick update.

Being from IT industry, I also see potential in cloud business model (cloud implementation as service model) which they have.

I will study it further.

Thanks.

The reason for the fall

" The Board has decided

to revise the dividend to be proposed to shareholders at the ensuing Annual General Meeting and

accordingly, Board has presently decided revised recommendation of dividend of Re. 1/- per equity

share at the AGM for approval of shareholders. The revised AGM notice dated September 5, 2017

has been approved by Board.

Reason for Revision of Dividend:

The Board in its meeting held on May 10, 2017 recommended to the shareholders for their

approval a dividend of Rs. 7 per equity share. While proposing the dividend for shareholders

approval, the Board has taken into consideration of “Consolidated accounts” and recommended

the dividend to the extent of profit available in consolidated Financials."

I believe in the business model of 8k Miles, I work in the related industry and I see a lot of potential for growth. But at the same time, the way management is managing the company is making me doubtful about my investment thesis.

Invested 3% of my portfolio - average price higher than current price

So does this mean that the intent of the company is good, as they were planning to give higher dividend ? But because they could not pay that high dividend from the standalone profit, they have been forced to revise the dividend down to Rs.1 .

Also, is it not strange that the board was not aware of such rules before announcing the dividend ?

I have also invested on the ground that Dividend Rs 7 will be paid… Purchase price Rs 620 on 11th may 2017. Can I reverse my purchase? How suddenly company realized provision of sec 123 companies act.

I have been bearish on the stock all along … Thing is i work too in IT sector and i don’t see anything like moat for this company.

Plus bad management adds to the my bearishness even more.

So basically when dividend was recommended, deloitte wasnt in the frame. This dividend thing has been recommended by the new auditors. And mostly 6 rupees should be paid in the coming quarters.

I don’t understand that when its present and future growth and profits posted are so rosy then why no one is interested in buying? Why after spectacular profits QoQ it’s breaking new lows everyday? Why there is only 1 mutual fund holding it? Why they declared dividend only after 7 years and that too was a fiasco? Why no famous investors have it in their portfolio? Even if someone look at their website at the bottom you will see

Copyright @8KMiles 2007-2016. I mean for a public listed company and that too a internet company can’t even correct their website? Unfortunately I bought it in bulk amount at an average of 500 after such good results and now this dividend fiasco.

Only one suggestion, focus more on balance sheet n cash flow. P&L is many times tool of bulls. M not giving any verdict but only a way to build conviction to get over greed n fears of price movement n stagnation . Best of luck

stock down 9% at around 400/-…whats happening here…stock down day by day…despite strong results, very good growth…and future of sector also looks promising…Can any one solve this puzzle?