I am just curious to know how come provision of 6.5cr help when the client defaults on receivables of 132 cr ? Can you throw more light on this. Suppose if the clients pay full, the provision reserve of 6.5 cr is maintained for future reserve (or) will be added to cashflows ?

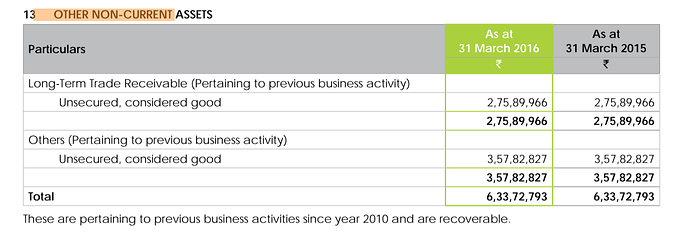

Long-term trade receivable are 6.5cr only.

@gautham1 Long term provision is 6.5 cr. What about trade receivables of 132 cr. There should be some provision pertaining to it right ? I am referring to your earlier post. Correct me if I misunderstood.

Trade receivable for FY17 = 132cr, 25% of revenue down from 29% in FY16.

Provisioning for trade receivable is done when management feels they are not recoverable. I agree that 25% trade receivable are on the higher side but

1. They are decreasing over the years.

2. Many-many companies have trade receivable of 25%. For a fast growing company, I think they are reasonable and no reason for worry.Thanks, Sreekanth. Receiving compensation from the US subsidiary may not be ideal in terms of disclosures to the Indian market, but there seems to be a logical reason for it. Without this reasoning I would be suspicious, but in light of that I would categorize this as an unknown, but not necessarily a negative.

I agree with the concern regarding not raising debt in US with the low cost of capital but again, that doesn’t seem like a massive issue. It may not make operational sense but I’m sure the management is aware of the low cost of capital and has their reasons. Either way, I wouldn’t count this as a major red flag from an investment perspective. At most a questionable decision by the management rather than evidence of corporate misgovernance.

I think the management has addressed the reverse merger in the Forbes interview alluded to above, and has accepted that it was a mistake on their part which they’re keen to move on from. I see no reason for it to be relevant to our investment decisions now.

Am I seeing everything above through 150% growth tinted glasses?

1 Like

shareholding at end of Q1 is out.

http://www.bseindia.com/corporates/shpSecurities.aspx?scripcd=512161&qtrid=94.00

promotors have sold around 10lac shares during q1

IIFL - backed by Prem watsa - has also picked 2 pc stake. How do you read it

Only CFO , Ramani has sold , Suresh Venkatachari the CEO and founder has not sold any shares.

If you give that kind of lucrative valuation why will promotors won’t sell … Only thing is what is that big cloud companies can’t do that these guys are doing ?

Forbes India

In Forbes i learned about MBL infra and then Nitin fire … both looked really promising and now down into dusts.

Forbes always talks of past performance and never about future. Inspite of anyone’s recommendation- must keep a track of actual performance every quarter.

MBL was also strongly recommended by Porinju. I bought it but later sold at shocking filings done by it on BSE.

Sharing a good white paper from KMPG on the next-Gen IT operating model: https://assets.kpmg.com/content/dam/kpmg/xx/pdf/2016/10/Next-Generation-IT-Delivery-Models.pdf.

The white paper talks about how the newer technologies and trends are now bringing varying levels of value to the business. These include cloud services, data and analytics, cognitive computing, mobile becoming more pervasive, consumerization of IT etc.

It is evident that, businesses across the world would not have any other option than migrating to Cloud. 8k Miles is an early-mover and leader in the above business, comparing to other IT service providers in India. They are coming up with outstanding results quarter after quarter due to the type of business they are in. This makes me very hard to ignore 8k Miles, in spite of any ambiguities in their financial statements or on the corporate governance.

Do you know who they are competing with ? Since when they become leader in this space ?

Its just nobody in india doing this doesn’t mean they are the leader.

Cloud is done and dusted already , you could have played this theme two years back now everybody has started doing that.

Name it Amazon , Microsoft , Oracle , Netsuits , Salesforce , IBM , SAP , Workday , list will go on.

They are into niche Pharmaceutical space but there too they are not the only one.

I think long term they going to trade between 10-15 times earning if they able to sustain their moat . Btw very heavy guys are attacking the moat i don’t wanna give soo much premium to it now.

I don’t see it has 30% CAGR stock anymore … may 10 % CAGR if things go well.

Not attractive from Risk reward point of view …

Its a known story , I don’t know why investor community discussing so much about it.

Dear Dhruva, It might be a known story, but I feel, it may also be prudent to review the situation periodically

Let me re-iterate their business model, otherwise I cannot do justice to my answer to your first question. 8k is not a cloud hosting service provider, unlike Amazon, Azure or Google. Instead, they help businesses to migrate to cloud (one-time business) and there upon provide the necessary on-going support (managed service offerings), which can be multi-year repeat business. In other words, 8k is just an implementation partner for product companies like Amazon. 8k also develops customized software for the customers on certain technologies (mainly recent hot technologies).Also, with Cornerstone acquisition, they are strengthening their Consulting service offerings even further.

Cloud market size is a large one, expected to be more than $200 Billion by 2020, and as I said earlier, for businesses around the world, moving to Cloud seems to be the only viable option. Even if product vendors like Amazon & Microsoft start offering implementation services tomorrow (Amazon has already started in a small way, I think), they cannot service the needs of the entire global market. Local players like 8k would always be important. Additionally, 8k can even be more experienced and effective in some of the areas (for example, pharma, healthcare verticals), as compared to those global biggies.

Why do you feel that, 8k’s skills and experience are not sufficient for them to compete with global players and be successful? Haven’t Indian IT services companies effectively competed with global giants and succeeded in the past? Indian companies have again and again proven to be leaders in IT services and we have seen the likes of Infosys grow from a capital of US$ 250 to US$ 10.4 billion revenue.

What is 8K’s MOAT? I would say, their experience on Cloud, skill, early-mover advantage to Cloud and tools/IP’s are primarily their MOAT. If you ask what was Usain Bolt’s MOAT to become 8-time Olympic Champion, I don’t think anyone can clearly explain that. There must be something similar here also, as is evident from their exceptional consistent growth rates YoY.

Among Indian providers, they are one of the early movers and specialists in Cloud offerings (whereas for other service providers, Cloud is just one among thier portfolio of service offerings) and they have marquee names in their list of customers, like Intel, BlueCross BlueShield, Cisco, Merck, Alfresco, ExonMobil, WB, Xerox etc. With their deep expertise, skills and automation tools/techniques, they are able to provide quicker quality services with efficiency and consistency, and the results are evident from their CAGR of more than 100% (revenue) for the past 5 years (Rs. 21 crore to 534 crore).

Coming to valuation, it trades at a P/E of 15.54 currently. It has increased its net profit from 3 crores in Mar’12 to 104 crores in Mar’17. Considering its past performance and the future prospects of cloud business, I feel that, it is perfectly reasonable to expect at least 60% growth in profit over each of the next couple of years. Even if no P/E expansion happens (but, isn’t a P/E of at least 30 reasonable?), I would be happy with that kind of returns.

10 Likes

Quite surprising that the company has neither declared results nor has announced dated for same. Majority of good companies have already declared results.

Anybody in know of reason for same?

The cloud story in the IT industry is not done but still unfolding. The large scale migration of enterprises is yet to happen. There is a lot of work and money to be made. The big enterprises will need help with deciding which cloud to move to (assessments), moving and then maintenance. As far as 8k miles what needs attention is their financials and governance.

http://www.businesswire.com/news/home/20170303005297/en/Global-Cloud-Migration-Services-Market-2016-2022--

Yes, the story is a known one and the same story keeps on repeating quarter after quarter . 8k Miles has yet again proven that, it can keep on growing its profit 100% year on year. I am not sure, if there is any other Indian company with market cap more than 1500 crores and growing at this rate year after year with consistency!

Those who are interested in this amazing growth story and willing to believe in it (may be, people with IT background will only believe it easily) may want to look at their Q1 results available at http://www.bseindia.com/xml-data/corpfiling/AttachLive/41930ce8-c5f6-48be-aec5-90311f036a42.pdf. It has doubled its profit of Rs. 19 crores in Q1’17 to Rs. 38 crores in Q1’18. Stock now quotes at an LTM P/E of just around 12.7.

One thing to be noted is that, the board has also proposed appointment of Deloitte Haskins & Sells LLP as their Statutory Auditors for the financial period from 1st April 2017 to 31st March 2022.

Disc: Invested and added more today in anticipation of the excellent results

The Q1FY18 result does look impressive and the detailed notes after that was quite useful as well.

Looks like a long term player for me.

Disc : Not invested, tracking.

In 2015 to 2016 sales jumped 100% while trade receivables jumped 300%. More than 40% sales growth stuck in trade receivables, looks like commodity company instead of niche software company.

Disc: Not invested and my personal views only.

Thank you