“Our company was born on the cloud with cloud expertise. We had a set of SMB customers who could not afford huge IT expenditures. We had to eradicate their capital expenditures and put them on an operating expenditure mode. For instance, a company’s expenditure of $200,000 on IT infrastructure can be halved if their software is set up on the cloud,” says Ramani, whose association with Suresh precedes 8K Miles

What this essentially means is there is an initial revenue from migration services along with a recurring revenue from post migration support services.

Though I am not 100% sure, but I think its because 8k miles issued more number of shares during that year. If you look at the balance sheets of the last two FYs, there is a small difference in share capital, implying that the number of shares outstanding changed during the last FY (could have been due to the company issuing more shares, say). The difference in the two EPS values is because of this, since EPS is calculated as Earnings/(no. of shares outstading)

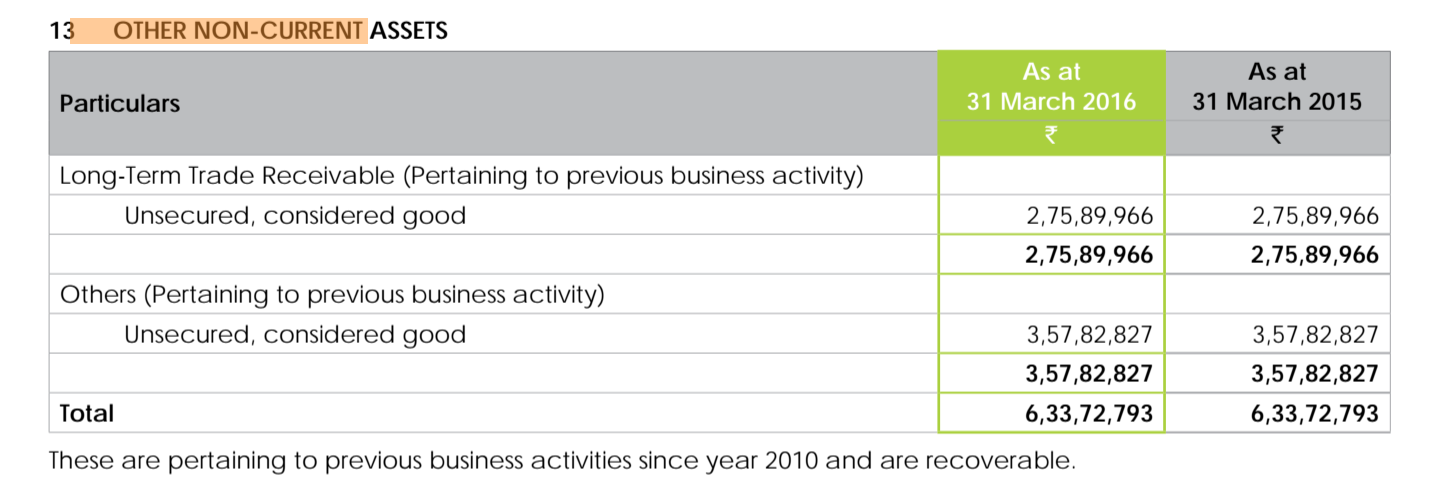

Carrying from 2010 receivables which they say is recoverable.

They had ~ 27 Cr worth of intangible assets generated and another 18 Cr under development. Looks too high for a services company.

Also, what does it mean for Reserves and Surplus to be in the cash flow from financing section? This is what is paying for the “investments” (the acquisitions and the intangible asset development), since there is hardly any operating cash flow.

Also, for what it is worth there are some negative reviews on glassdoor:

The summation of net profit between 2011 to 2016 is 74.21 cr at the same time cash flow from operating activity is 57.59cr. For a fast growing this seems reasonable.

Also trade receivable as percentage of revenues is 25% which is slightly on the higher side but is not alarming in any way.

Where did you get the figures of 27cr and 18cr from?

The intangible asset part is from the notes to the consolidated financial statements.

On the cash flow part: I am looking at their 2016 numbers where they have about 18 Cr from operations, they have spent 85 Cr on investing primarily in intangible assets. The money has to come from financing activity but there I only see a number with the heading “Reserves and surplus”. What does this mean? Did the get the cash to spend on investing from debt or raising equity? As I understand that should be only two ways they can get cash.

Also the 6 Cr they have receivable in long term assets from 2010 that they think is fully recoverable is quite suspect.

Also out of the FY 2016 revenue of 271 Cr; 80.2 is receivable + 27 Cr is a current asset of unbilled revenue (it is under the note for other current assets; which was not there in FY 2015); which makes it more like 39% of revenue.

Ok; was still looking at the old one since I think the new AR is not out. But briefly glanced at the results now.

Other current assets has jumped to 72 Cr; so its which again makes it about 38%. Don’t know what is in the other current assets until we have the AR; but last time it was mainly unbilled revenue.

I agree that the 6Cr is not material; but carrying this on the books as considered good (its there this year too) from 2010 just makes me question every number I see in their statements.

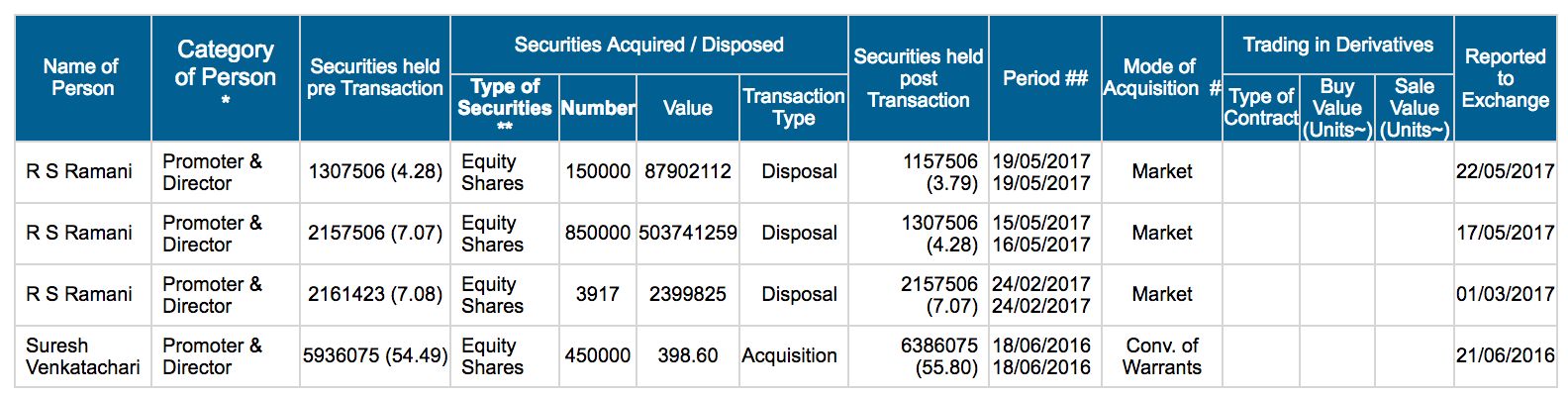

Also, another negative. Just noticed Ramani the CFO has sold about 59 Cr worth of shares on the market in the last 10 days. Not a vote of confidence one would expect looking at the headline numbers.

I could not understand, why you would like to add unbilled revenue to trade receivable. It will be thankful if you could explain it to me.

At the end of fy15 company had cash = 15cr

During fy15 company issued 5.5 lac shares @ 398.5 = 22cr

Also during the year company acquired NexAge & Cintel.

Intangibles have been broken up as

Internally generated = 27.35cr

Goodwill = 50.44cr

Does this data help answering your questions in relation to Cash Flow Statement?

If no, we need to break you question down and then work in each part to see if something is wrong with the company?

On unbilled revenue: It is also revenue that has been recognized but for which cash has not been received.

Several things not clear to me still, but given the selling from the CFO I don’t want to look into this further. To summarize my main issues:

Carrying 6 Cr as considered good for 6-7 years past when the money was to be recieved

Intangible asset generated internally during year of 27 Cr in FY 16 seems very high for what is primarily a services company with about 130 Cr of employee benefit expenses. For comparison Infy seems to have about 30 Cr of IP as intangible assets (goodwill of course is higher)

Inexplicable to me where they generated cash for investment of 80 odd Cr in FY 16.

Hi KV…Yes, the CFO selling is not good news…He had sold about half of

his holding. But he had held the stock for many years and saw it going up

more than 100 - 1000 times. So, what is wrong in taking some profits

out…So, it can be debated both ways…Even Eicher Motors management did

that last year…And even Microsoft do it regularly…

Does anyone have any insights on the Ambit report shared above? The long term receivables may not be a huge issue considering they’re ~25% of revenues which, as mentioned above can be expected from a company growing this fast. All the peers they have shown aren’t growing anywhere close to 8k Miles’ pace.

However, the accelerated depreciation and the opaqueness surrounding the management compensation could be serious concerns. I’m relatively new to investing in small caps, wondering if such discrepancies are par for the course? A few years back, I’d invested in Vakrangee where similar questions were raised. The company just kept on growing and once they reached a certain size, retained PWC and Deloitte as auditors.

Of course, the above isn’t necessarily going to happen, just wondering if it’s a necessity to expect lower thresholds of accounting standards in similarly sized companies?

Hi Siddarth,

On management compensation, standalone net profit is very small hence due to limits on managerial compensation linked to % of profits they might be getting paid by US subsidiary.

Having access to financials of US subsidiary will answer many questions. Companies like TAMO upload JLR financials as well as AR, big companies does that…

Frequent errors in financial statements like numbers don’t add up in cash flow and eps calculations mistakes etc show the incapability of CFO, They have major business in US subsidiary but they raise debt/equity from india to invest in US. Couldn’t they raise debt from US Subsidiary considering low cost of capital in US…

All IT companies have their base in india and bill revenues from Indian entity while it is not the case with 8K miles.

Revenues of standalone company are very small compared to consolidated so there can be some holding company discount applicable on valuations.

Why did they reverse merge with a shell company with bad reputation and under SEBI lens to raise QIP for acquisitions? CEO mentioned in FORBES article he went to reverse merger as he didnt like VC funding and give them control. He had prior experience in NASDAQ listing he could have waited and went for proper IPO…

I still dont understand why someone will list in india when they dont have much operations from Indian company.